AI-powered loan underwriting is defined as the application of machine learning, large language models, and neural networks to automate credit data extraction, risk scoring, and decision packaging within the lending workflow. The case for adopting this technology is no longer theoretical. TD Bank's AI agent reduced mortgage processing from 15 hours to minutes, delivering packaged summaries directly to human underwriters for final adjudication. For risk management professionals and financial decision-makers, understanding why use AI for loan underwriting comes down to three measurable outcomes: faster decisions, more accurate credit risk assessment, and expanded borrower access, all within a compliant, human-supervised framework.

Why use AI for loan underwriting: efficiency and accuracy gains

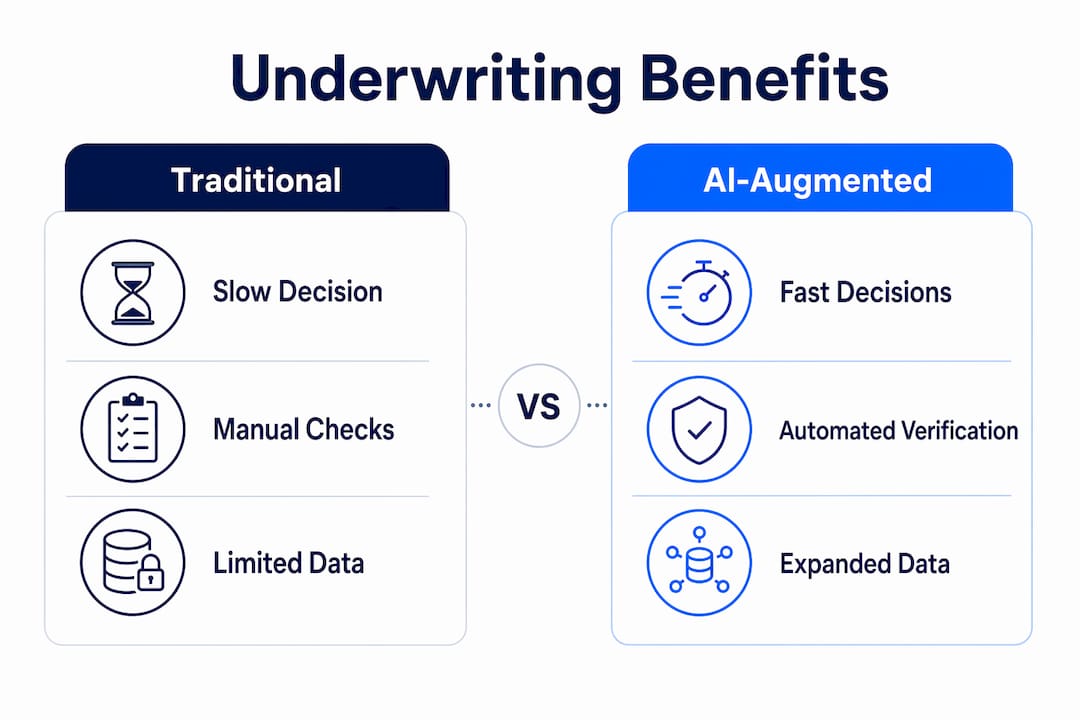

Traditional loan underwriting is a document-intensive, sequential process. An underwriter manually pulls income statements, verifies assets, cross-references credit bureau data, and applies rules-based criteria, a workflow that routinely takes three to five business days per file. AI collapses that timeline by automating document ingestion, optical character recognition, data extraction, and preliminary risk scoring in a single pass.

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

The speed gains are substantial and well-documented. AI underwriting systems can reduce loan decision time from multiple days to under three minutes by replacing static FICO-only models with dynamic, multi-variable assessments that process income volatility, cash flow patterns, and behavioral signals simultaneously. That compression in cycle time translates directly into competitive advantage: lenders who respond faster close more loans.

Accuracy improvements are equally significant, particularly when AI incorporates alternative data. Transaction-level bank data, rent payment histories, and utility records give models a far richer picture of a borrower's actual financial behavior than a tri-merge credit report alone. Transaction-level AI provides a continuous, explainable data stream that enhances underwriting precision beyond what historical credit files can offer. This matters most for thin-file borrowers, including freelancers, gig workers, and young adults, whose creditworthiness is systematically underestimated by legacy scoring models.

| Underwriting step | Traditional workflow | AI-augmented workflow |

|---|---|---|

| Document collection | Manual upload and sorting | Automated ingestion and classification |

| Income verification | Underwriter reviews pay stubs manually | AI extracts and annualizes income in seconds |

| Credit risk scoring | Single FICO score, rules-based thresholds | Multi-variable model using transaction and alternative data |

| Decision turnaround | 3 to 5 business days | Under 3 minutes for standard files |

| Human review | Full file review by underwriter | Underwriter reviews AI-packaged summary and exceptions |

Pro Tip: Start your AI underwriting pilot with the document extraction and income verification steps. These are the most standardized, highest-volume tasks in your workflow, and they produce measurable ROI within the first 90 days without requiring changes to your credit policy.

Does AI replace human underwriters or complement them?

The most persistent misconception in this conversation is that AI underwriting is a binary choice between full automation and the status quo. It is neither. Human-in-the-loop models combine AI strengths with human judgment to meet regulatory and quality demands, and that hybrid structure is where the real value lives.

AI excels at standardized, high-volume tasks: parsing W-2s, extracting bank statement data, flagging missing documents, and generating preliminary risk scores. Where it struggles is with the nuanced judgment calls that define complex files. Annualizing income for a self-employed borrower with irregular draws, interpreting a blurry or partially completed document, or weighing a borrower's explanation for a prior delinquency, these are situations where human expertise remains irreplaceable.

Regulatory accountability reinforces this point. Adverse action notices, fair lending compliance, and Community Reinvestment Act obligations all require explainable, auditable decision rationale. An AI model that cannot articulate why it denied a loan creates legal and regulatory exposure that no lender can afford. The practical answer is a workflow where AI handles data assembly and preliminary scoring, and a credentialed underwriter retains authority over the final credit decision.

Consider how this plays out operationally:

- AI agents process incoming loan files, extract structured data, and flag anomalies or missing items within seconds of submission.

- The system generates a risk summary with supporting data points, organized for rapid human review.

- The underwriter focuses on exception handling, borrower-specific nuances, and compliance sign-off rather than data entry.

- Complex files, such as those involving multiple income sources or non-standard collateral, are escalated automatically for deeper human analysis.

Pro Tip: When designing your AI underwriting workflow, define explicit handoff criteria before deployment. Specify which file types go straight through AI processing, which trigger human review, and which require senior underwriter adjudication. Ambiguous handoffs are where errors and compliance gaps emerge.

What are the measurable benefits for portfolio performance?

The business case for AI in lending extends well beyond speed. The portfolio-level outcomes are where risk management professionals should focus their attention, because the numbers reframe the ROI conversation entirely.

Transaction-level AI underwriting increases approval rates by 10 to 35%, accelerates decisions up to five times faster, and reduces portfolio losses by 15 to 40% without taking on additional risk. That loss reduction figure deserves emphasis: it means AI is not simply approving more loans and accepting more defaults. It is identifying creditworthy borrowers that legacy models misclassify as risky, while simultaneously detecting risk signals that static credit scores miss entirely.

Approval rate improvements are particularly pronounced for underserved segments. Thin-file borrowers see approval rate increases of up to 27% when lenders incorporate alternative data into their models. For community banks and credit unions competing against fintech lenders for younger and immigrant borrowers, this is a direct growth lever.

"AI doesn't just score borrowers faster. It scores them more completely, using data that reflects how they actually manage money rather than how they managed debt years ago."

Risk-based pricing also becomes more precise under AI-driven models. Where traditional underwriting groups borrowers into broad risk buckets, AI enables micro-tiered loan pricing based on cash flow volatility, income stability, and behavioral patterns. Two borrowers with identical FICO scores may receive materially different rates because their transaction histories reveal fundamentally different risk profiles. That granularity protects net interest margin while keeping pricing competitive.

| Outcome metric | Traditional underwriting | AI-augmented underwriting |

|---|---|---|

| Decision turnaround | 3 to 5 days | Under 3 minutes |

| Approval rate lift | Baseline | 10 to 35% increase |

| Thin-file approval improvement | Baseline | Up to 27% increase |

| Portfolio loss reduction | Baseline | 15 to 40% reduction |

| Pricing tiers | Broad risk buckets | Dozens of micro-tiers |

How to implement AI in loan underwriting without common pitfalls

The most common implementation failure is scope. Institutions that launch with a vision of end-to-end AI automation across all loan products simultaneously tend to produce systems that are difficult to audit, hard to explain to regulators, and slow to deliver measurable results. The evidence-backed approach is the opposite: start with narrowly defined, document-heavy workflows that have clear inputs, outputs, and control points.

Explainability and auditability are non-negotiable, not optional features to add later. Bias mitigation and explainability frameworks are essential to maintain fairness and regulator trust, and they must be built into the model architecture from the start. This means your AI system needs to generate decision rationale that a compliance officer can read, a regulator can audit, and a borrower can receive as an adverse action explanation.

Fairness testing deserves its own workstream. AI models trained on historical lending data can encode and amplify existing disparities in credit access. Before deployment, run your model against demographic proxies to identify whether approval rates diverge in ways that cannot be explained by legitimate credit factors. This is not just a regulatory requirement. It is a reputational and legal risk management imperative.

Three additional practices that separate successful implementations from stalled ones:

- Measure ROI at the workflow level, not the enterprise level. Track cycle time reduction, underwriter capacity freed, and error rates for each specific use case before expanding scope.

- Maintain a clear human adjudication protocol for exceptions. Every AI system will encounter files it cannot process confidently. The escalation path must be defined, tested, and documented before go-live.

- Invest in model monitoring post-deployment. Credit conditions change, and a model trained on 2023 data may perform differently in a 2026 rate environment. Scheduled revalidation is a governance requirement, not a nice-to-have.

Pro Tip: Before selecting an AI underwriting vendor, ask for a sample adverse action explanation generated by their system. If the explanation is not clear enough to satisfy a CFPB examiner, it is not ready for production.

Key takeaways

AI-powered loan underwriting delivers measurable gains in speed, accuracy, and portfolio performance only when implemented within a structured human-in-the-loop framework that prioritizes explainability, fairness, and bounded workflow design.

| Point | Details |

|---|---|

| Speed is the entry-level benefit | AI reduces loan decisions from days to under three minutes, freeing underwriters for complex files. |

| Portfolio losses drop significantly | Transaction-level AI reduces portfolio losses 15 to 40% without requiring additional risk appetite. |

| Thin-file borrowers gain access | Alternative data models increase approval rates for underserved borrowers by up to 27%. |

| Human oversight is non-negotiable | Regulatory compliance and adverse action requirements demand explainable, human-supervised final decisions. |

| Start narrow, then scale | Bounded, document-heavy workflows with clear control points deliver faster ROI and lower implementation risk. |

The underwriting transformation I think most institutions are getting wrong

My honest assessment, after watching dozens of financial institutions approach AI adoption, is that the conversation is still too focused on the technology and not focused enough on the workflow design. Institutions spend months evaluating AI vendors and almost no time mapping exactly where human judgment adds irreplaceable value versus where it is simply adding latency to a process a machine can handle better.

The institutions getting this right are not the ones with the most sophisticated models. They are the ones that defined their human-in-the-loop criteria before they wrote a single line of configuration. They know which file types go straight through, which ones get flagged, and which ones land on a senior underwriter's desk. That clarity is what makes the system auditable, scalable, and defensible to regulators.

There is also a customer experience dimension that risk managers tend to underweight. A borrower who receives a decision in three minutes and a clear explanation of that decision, whether approved or declined, has a fundamentally different relationship with your institution than one who waits five days and receives a form letter. AI done well is not just an operational efficiency play. It is a trust-building mechanism, and in a market where community banks and credit unions compete against fintech lenders on experience as much as rate, that matters.

The practical path forward is to deploy AI risk management in stages, measure outcomes at each stage, and resist the pressure to automate everything before you have validated that your model performs fairly and accurately across all borrower segments. The institutions that scale thoughtfully will outperform those that move fast and fix problems later.

— Raj

How RiskInMind supports smarter loan underwriting

RiskInMind builds AI-powered tools specifically for the credit risk workflows that community banks, credit unions, and lenders run every day. The David AI Loan Assessor analyzes loan files, detects risk signals, and generates underwriting conditions, giving your team a structured, auditable summary rather than a raw data dump. For commercial real estate portfolios, the CRE Loan Risk Predictor applies transaction-level analysis to assess property and borrower risk with the granularity that broad credit scoring cannot provide. Both tools are built on SOC 2 certified infrastructure with response times under half a second, so your underwriters get AI-grade speed without sacrificing the security and compliance standards your institution requires.

FAQ

What is AI loan underwriting?

AI loan underwriting is the use of machine learning and large language models to automate credit data extraction, risk scoring, and decision packaging within the lending process. Human underwriters retain final decision authority, particularly for complex files and regulatory compliance.

How much faster are AI underwriting decisions?

AI systems can reduce loan decision time from three to five business days to under three minutes for standard files. TD Bank's implementation cut mortgage processing from 15 hours to minutes using an agentic AI workflow.

Does AI underwriting increase approval rates?

Transaction-level AI underwriting increases approval rates by 10 to 35% overall, with thin-file borrowers seeing gains of up to 27% when alternative data such as rent and utility payments is incorporated into the credit model.

What are the main compliance risks of AI underwriting?

The primary compliance risks are model bias, lack of explainability in adverse action notices, and insufficient human oversight. Responsible AI underwriting requires bias testing, explainability frameworks, and documented human adjudication protocols before deployment.

Where should lenders start with AI underwriting implementation?

Start with narrowly defined, document-heavy workflows such as income verification and document extraction, where inputs and outputs are standardized and control points are clear. This approach delivers measurable ROI faster and reduces regulatory and operational risk during the initial deployment phase.