Accuracy in risk management is defined as correctly identifying and quantifying the threats that genuinely affect your institution's objectives, not simply generating numbers that look authoritative. For risk professionals at credit unions, community banks, and lenders, the question of why prioritize accuracy in risk management has a direct answer: inaccurate risk data produces wrong decisions, misallocated capital, and regulatory exposure. Failing to prioritize data accuracy in risk workflows causes fines, missed market opportunities, and regulator scrutiny that reflects poorly on governance. The 2026 risk environment demands that institutions distinguish between data that is precise and data that is actually correct. Those two qualities are not the same thing, and confusing them is one of the most costly mistakes in financial risk management.

Why does accuracy improve risk prioritization and decision-making?

Accurate risk data is the foundation of sound risk prioritization. Without it, your institution allocates capital and attention to the wrong threats while real exposures accumulate undetected. Quantitative precision — many decimal places in a model output — does not guarantee accuracy. A model can be directionally wrong because its underlying assumptions are flawed, even when it produces results that look authoritative.

The distinction between precision and accuracy matters enormously in practice. Precision describes how finely a measurement is expressed. Accuracy describes whether that measurement reflects reality. A credit risk model that outputs a probability of default to four decimal places is precise. If the model was calibrated on pre-pandemic loan data and applied to a post-rate-shock portfolio, it is not accurate. The fine-grained output masks a structural error.

Models that perform accurately in 95% of standard scenarios can fail catastrophically in the remaining 5%, where assumptions break down. That 5% is precisely where crises originate. False precision hides the warning signals that would otherwise prompt human review.

Risk professionals who understand this treat model outputs as inputs for human judgment, not as final answers. The model narrows the range of possibilities. The risk officer, drawing on institutional knowledge and current conditions, makes the call.

Key indicators that your risk data may be misleading include:

- Model outputs that never change significantly across reporting cycles

- Risk ratings that cluster tightly around the middle of the scale

- Assumptions that have not been updated since the model was built

- Inputs sourced from parties with a financial interest in the outcome

Pro Tip: Before presenting any model output to senior leadership, ask one question: what assumption, if wrong, would reverse this conclusion? If you cannot answer that quickly, the model needs more scrutiny before it drives a decision.

What are the best practices for maintaining accuracy in risk frameworks?

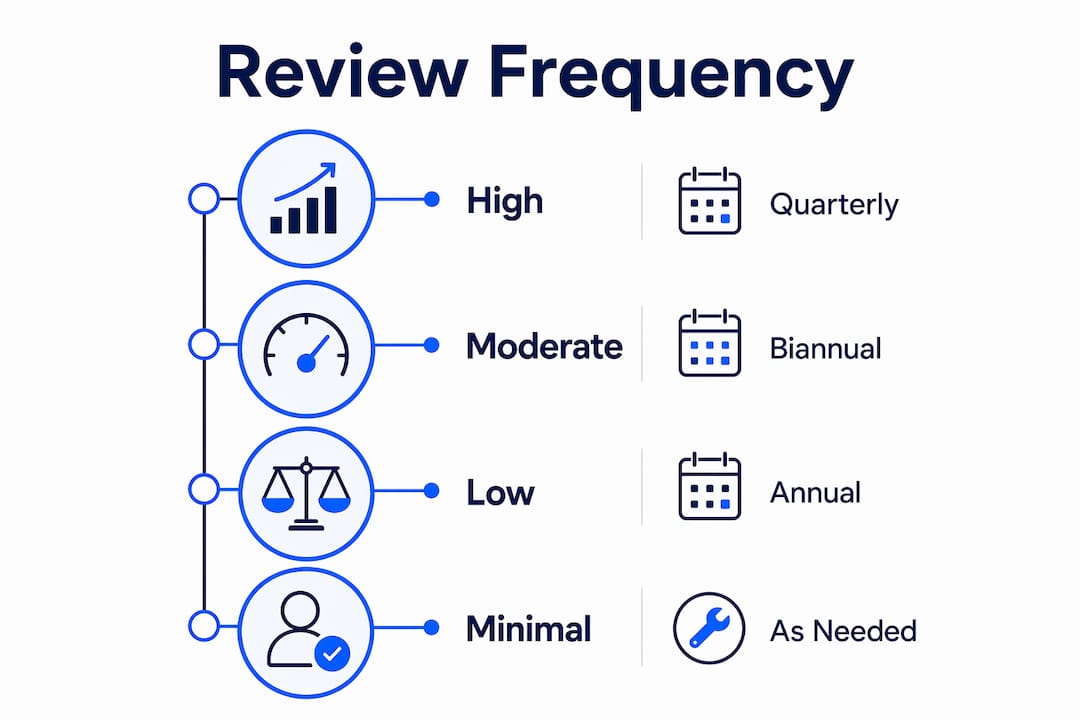

Review frequency is the first structural control for maintaining accuracy. High-risk areas require quarterly reviews for controls, while lower-priority risks allow annual assessments. That cadence is not arbitrary. It reflects the rate at which conditions change and the cost of acting on stale data in each risk category.

The table below summarizes how review frequency and validation intensity should align with risk priority level.

| Risk priority | Review frequency | Validation approach |

|---|---|---|

| High | Quarterly | Full model validation, stress testing, assumption review |

| Medium | Semi-annual | Control effectiveness testing, data source verification |

| Low | Annual | Sanity checks, trend comparison, exception flagging |

Beyond scheduled reviews, fast manual checks catch errors that formal audits miss. Fast manual data sanity checks under one minute catch most common inaccuracies, especially from parties with conflicting incentives. These checks require no specialized statistical tools. They work because structural inaccuracies tend to produce visible anomalies: numbers that refuse to reconcile, distributions that look too clean, or counterparties who will not share raw data.

Effective data ingestion policies are equally critical. Every data source feeding your risk models should have a documented owner, a defined update frequency, and a clear audit trail. Accurate data ingestion forms the foundation for all downstream risk monitoring and modeling. A model built on well-validated inputs will outperform a more sophisticated model built on questionable data.

Core validation steps before relying on any risk dataset include:

- Confirm the data source has no undisclosed conflicts of interest

- Check that the time period covered matches current conditions

- Look for patterns that are statistically too regular to be real

- Verify that the data owner can produce raw records on request

Pro Tip: Build a one-page data provenance log for each major risk input. Record the source, the date last updated, who validated it, and any known limitations. This single habit prevents most downstream model failures.

For a deeper look at how review cycles align with compliance requirements in 2026, the Riskinmind resource library covers current framework standards in detail.

How do organizational culture and systemic biases impact risk accuracy?

Culture is the most underestimated threat to risk accuracy. Technical controls and review cycles only work if the people operating them are willing to report what they actually find. Organizational cultures often penalize those reporting inconvenient accurate risk results, producing systemic truth degradation across the institution.

Truth degradation is not a dramatic event. It happens gradually. A risk officer softens a finding to avoid conflict with a business line head. A model assumption goes unchallenged because questioning it would delay a deal. A portfolio review flags a concentration risk, but the language in the final report is hedged until the signal disappears. Each individual act seems minor. The cumulative effect is a risk function that no longer reflects reality.

"Alignment is prioritized over accuracy, weakening escalation and masking exposures beneath false control." — Enterprise Risk Magazine, 2026

The organizational consequences are severe. Hidden exposure accumulates in portfolios that appear well-managed on paper. When conditions shift, the institution discovers it is holding concentrations or credit deterioration that its own risk reports never surfaced. Regulators examining those reports after the fact find a governance failure, not just a modeling error.

Addressing cultural bias requires structural changes, not motivational messaging. Anonymous escalation channels, separation between risk reporting and business line performance reviews, and board-level review of risk findings all reduce the pressure to filter uncomfortable data. The goal is to make accurate reporting the path of least resistance, not the path most likely to generate pushback.

What practical steps can financial institutions take to prioritize risk accuracy?

Embedding accuracy into risk workflows requires changes at the data, model, and cultural levels simultaneously. No single intervention is sufficient on its own. The following sequence reflects the order in which changes produce the most durable results.

- Establish data quality controls at ingestion. Define acceptable data sources, document their limitations, and assign ownership before any modeling begins. Reject inputs that cannot be traced to a verifiable origin.

- Run fast sanity checks on every new dataset. Simple validation tests, like refusal to share raw data or unusual patterns, reveal structural inaccuracies before formal audits. Apply these checks as a standard gate, not an occasional exercise.

- Validate models against current conditions. Stress test assumptions using scenarios that reflect the current rate environment, credit cycle, and regulatory expectations. A model validated in 2022 is not validated for 2026.

- Define acceptable uncertainty explicitly. Accuracy in measurement is about defining acceptable uncertainty levels according to potential costs of error, not eliminating all uncertainty. Document the tolerance for each risk category and communicate it to decision-makers.

- Separate risk reporting from business line incentives. Risk officers who report to the same executive as the business lines they assess face structural pressure to soften findings. Organizational independence is a prerequisite for accurate reporting.

- Align review cycles with 2026 framework standards. High-risk areas need quarterly control reviews. Lower-priority risks can follow annual cycles. Misaligning review frequency with risk priority wastes resources and creates blind spots simultaneously.

- Treat model outputs as starting points. Train risk teams to interrogate model conclusions rather than present them as facts. The risk analytics process works best when human judgment validates what the model produces.

Key Takeaways

Accuracy in risk management is the single most important determinant of whether your institution's risk function produces decisions that protect the balance sheet or decisions that create a false sense of control.

| Point | Details |

|---|---|

| Precision is not accuracy | A model can produce fine-grained outputs that are directionally wrong due to flawed assumptions. |

| Review cycles must match risk priority | High-risk areas require quarterly reviews; lower-priority risks allow annual assessments under 2026 standards. |

| Fast sanity checks prevent model failures | Sub-minute manual checks catch structural data inaccuracies before they enter formal models. |

| Culture degrades accuracy silently | Organizations that penalize uncomfortable findings accumulate hidden exposure over time. |

| Data ingestion quality drives all downstream results | Poor data at intake produces unreliable monitoring, modeling, and regulatory reporting. |

The uncomfortable truth about risk accuracy

The most persistent problem I see in financial risk management is not technical. It is the institutional habit of treating a precise number as a correct one. Risk officers present model outputs with four decimal places, and senior leaders accept them as facts. Nobody asks what assumption would reverse the conclusion. Nobody checks when the model was last validated against current conditions.

The 2008 financial crisis produced extensive post-mortems on model failure. The core finding was consistent: the models were not wrong because the math was bad. They were wrong because the assumptions were wrong, and nobody with authority was asking hard questions about those assumptions. That lesson has not been fully absorbed. Institutions still conflate the sophistication of a model with its reliability.

The cultural problem is harder to fix than the technical one. I have seen risk teams produce accurate, uncomfortable findings that were quietly revised before reaching the board. The revision was not fraudulent. It was the product of a hundred small decisions to soften language, hedge conclusions, and avoid conflict. The result was a risk report that looked professional and was substantively misleading.

The fix starts with leadership. When a CRO or board risk committee visibly rewards a risk officer for delivering bad news accurately, the culture shifts. When the same leaders penalize softened findings after the fact, the shift accelerates. Accuracy is not a technical standard. It is an organizational commitment. You either build structures that support it, or you build structures that erode it. There is no neutral position.

— Raj

How Riskinmind supports accurate risk assessment

Risk professionals who want to embed accuracy into their workflows need tools that validate data at intake, flag model anomalies in real time, and maintain audit trails that satisfy regulatory scrutiny. Riskinmind builds those capabilities directly into its platform for credit unions, community banks, and lenders.

The Riskinmind loan application product integrates data quality controls at the point of intake, reducing the risk of flawed inputs reaching downstream models. The CRE Loan Risk Predictor applies AI-driven analysis to commercial real estate portfolios, with outputs designed to support human judgment rather than replace it. Both products operate under SOC 2® certification with real-time processing, giving risk teams the data integrity and speed that 2026 compliance standards demand. For institutions ready to move from manual validation to systematic accuracy controls, Riskinmind provides the infrastructure to do it at scale.

FAQ

What is the difference between accuracy and precision in risk management?

Accuracy means a risk measurement reflects reality. Precision means it is expressed in fine detail. A model can be highly precise and still be wrong if its underlying assumptions are flawed.

Why does inaccurate risk data cause regulatory problems?

Regulators treat data quality as a governance indicator. Poor data ingestion causes fines, missed market opportunities, and scrutiny that signals weak internal controls to examiners.

How often should risk controls be reviewed to maintain accuracy?

High-risk areas require quarterly control reviews under 2026 risk framework standards. Lower-priority risks can be assessed annually without compromising accuracy.

What is truth degradation in risk management?

Truth degradation occurs when organizational culture penalizes accurate but uncomfortable risk findings, causing risk signals to be softened or filtered before reaching decision-makers.

How can financial institutions improve risk data accuracy quickly?

Fast manual sanity checks under one minute catch most common data inaccuracies before they enter models. These checks require no statistical tools and work by identifying anomalies like refusal to share raw data or patterns that look too regular to be real.