Risk scoring is defined as the systematic process of assigning numeric or categorical values to risks so they can be compared, prioritized, and tracked over time. At its core, risk scoring combines two primary inputs: the likelihood that a risk event will occur and the severity of its impact if it does. For credit unions, community banks, and lenders, this process is not a compliance formality. It is the analytical foundation that determines where capital, controls, and attention flow. Frameworks like NIST IR 8286, Oracle's risk methodology, and ISO 31000 each formalize risk scoring within enterprise risk management, and understanding how they differ is the starting point for applying them well.

What is risk scoring and how does it work?

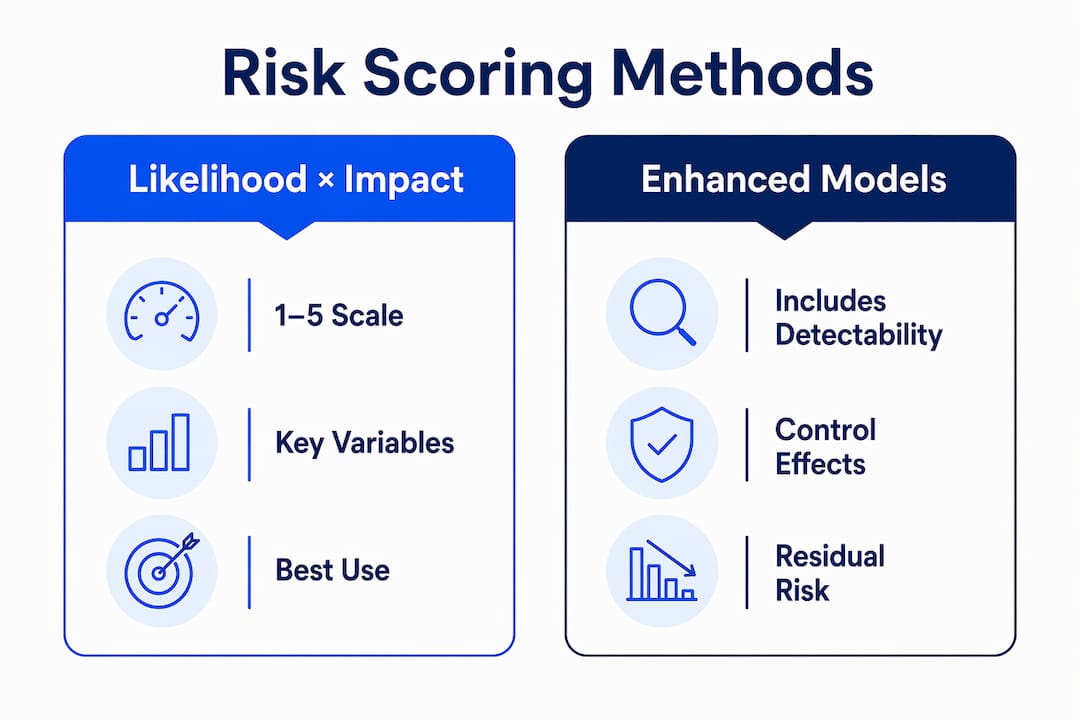

Risk scoring translates qualitative judgment into a structured, repeatable number. The standard formula is straightforward: Risk Score = Likelihood × Impact, where each variable is rated on an ordinal scale. A 1–5 scale is the most common choice in financial institutions, producing a composite score range of 1–25. That range is then divided into categorical bands: low (1–4), moderate (5–9), high (10–19), and critical (20–25).

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

The bands matter more than the raw number. A score of 18 is not twice as dangerous as a score of 9 in any mathematical sense. The bands communicate priority tiers, not precise magnitudes. This distinction keeps scoring practical and prevents false precision from distorting decisions.

Beyond the basic formula, some institutions incorporate a third variable: detectability or control effectiveness. A risk that is highly likely and highly impactful but also highly detectable may warrant a different response than one that is equally severe but nearly invisible. This three-factor approach appears in frameworks like FMEA (Failure Mode and Effects Analysis), which is used in operational risk programs at larger financial institutions.

The concept of inherent versus residual risk scoring adds another layer of analytical depth. Inherent risk is scored before any controls are applied. Residual risk reflects what remains after controls are in place. Tracking both scores side by side reveals how much work your control environment is actually doing. If a risk carries an inherent score of 20 and a residual score of 18, the controls are not performing. That gap is where accountability lives.

Comparing common risk scoring methods

| Method | Scale | Key Variables | Best Use Case |

|---|---|---|---|

| Likelihood × Impact Matrix | 1–5 or 1–10 | Probability, severity | General enterprise risk registers |

| FMEA Scoring | 1–10 per factor | Severity, occurrence, detection | Operational and process risk |

| NIST Cybersecurity Framework | Qualitative tiers | Likelihood, impact, BIA values | Cybersecurity and IT risk programs |

| ISO 31000 Blended Approach | Context-dependent | Qualitative + quantitative inputs | Mature, multi-domain risk programs |

Pro Tip: Start with a 1–5 scale rather than 1–10. Finer scales create the illusion of precision but increase assessor disagreement. Expand the scale only when your program has enough historical data to calibrate the additional gradations.

What are the practical challenges in applying risk scoring?

The mechanics of risk scoring are straightforward. The governance required to make scores reliable is not. The most common failure point is inconsistent scale definitions. Undefined likelihood scales cause different assessors to assign different scores to identical risks, which undermines the entire purpose of quantification. A "likely" event means something different to a credit officer in a rural community bank than it does to a compliance analyst at a regional lender.

The following challenges appear consistently across financial institutions that rely on risk scoring:

- Scale definition gaps. Likelihood should be tied to a specific timeframe, such as "probability of occurrence within 12 months," not a vague descriptor like "possible."

- Impact definitions without measurable anchors. Impact ratings must connect to real loss categories: financial loss thresholds, regulatory penalty ranges, or reputational exposure metrics.

- Treating scores as absolute truth. Risk scores are model outputs dependent on chosen scales and thresholds. Changing those inputs without version control produces misleading trend data.

- Misalignment with risk appetite. Scores that are not calibrated against the institution's stated risk tolerance produce priorities that do not reflect what leadership is actually willing to accept.

- Assessor training gaps. Without structured calibration sessions, scoring becomes a compliance exercise rather than a decision-making tool.

Residual risk scores are particularly vulnerable to these issues. If control effectiveness is assumed rather than tested, residual scores will overstate how much protection the institution actually has. This is a common audit finding in community bank examinations.

Pro Tip: Run a calibration exercise annually. Present three to five identical risk scenarios to your assessors independently, then compare scores. Gaps greater than two points on a 1–5 scale signal a definition problem, not a judgment problem.

How is risk scoring integrated into risk management workflows?

Risk scoring does not operate in isolation. It sits inside a broader workflow that begins with risk identification and ends with monitored, residual risk. Understanding where scoring fits in that chain is what separates institutions that use scores to drive decisions from those that file them in a register and move on.

Oracle's risk methodology provides a clear workflow model. The process assigns probability and impact values, applies the matrix to generate a score, records the planned response action, and then captures a post-response score to estimate residual risk. That post-response score becomes the basis for ongoing monitoring and escalation triggers. Oracle's scoring approach treats scoring as a governance tool, not just a measurement.

NIST IR 8286 integrates risk scoring with business impact analysis (BIA). BIA outputs define asset criticality and acceptable impact thresholds, which then inform the impact dimension of every risk score. This means BIA-informed scoring produces priorities that are grounded in what the institution has determined it cannot afford to lose. For cybersecurity risk programs in particular, this connection between BIA and scoring is now considered a baseline expectation by federal examiners.

ISO 31000 takes a broader view. The standard expects organizations to select and sequence risk assessment techniques based on data maturity and context, blending qualitative and quantitative methods as appropriate. This means a community bank with limited loss history might rely primarily on expert judgment and qualitative banding, while a larger institution with actuarial data can apply quantitative models with statistical confidence.

Risk scoring workflow: from identification to monitoring

| Workflow Step | Activity | Output |

|---|---|---|

| Risk Identification | Catalog risk events by category | Risk register entries |

| Inherent Scoring | Apply Likelihood × Impact before controls | Inherent risk score |

| Control Assessment | Evaluate existing control effectiveness | Control gap analysis |

| Residual Scoring | Recalculate score after control credit | Residual risk score |

| Response Planning | Assign treatment actions to high/critical risks | Treatment plan |

| Ongoing Monitoring | Track score changes and trigger thresholds | Updated risk profile |

Automation is increasingly central to this workflow. Platforms that integrate with core banking systems can pull transaction data, delinquency rates, and concentration metrics directly into scoring models, replacing manual spreadsheet inputs with real-time data feeds. For institutions managing large loan portfolios, this shift from periodic to continuous scoring changes the speed at which emerging risks become visible. You can explore how automated risk assessment works in practice for banks and credit unions.

What are best practices for reliable risk scoring?

Reliable risk scoring requires deliberate design choices before the first score is ever assigned. The following practices reflect what well-governed financial institutions do differently from those that treat scoring as a checkbox.

-

Define scales with measurable anchors. Likelihood ratings should reference specific time horizons and frequency estimates. Impact ratings should map to dollar loss ranges, regulatory consequence categories, or customer harm metrics that your institution has already quantified.

-

Maintain inherent and residual scores side by side. Tracking both scores clarifies what your control environment is achieving and directs treatment planning toward the risks where controls are weakest.

-

Align scoring thresholds with risk appetite. Scores tied to risk appetite produce priorities that reflect what leadership has formally decided the institution can tolerate. Without this alignment, high scores may not trigger escalation, and low scores may mask exposures that exceed appetite.

-

Version your scoring methodology. Every time you change a scale definition, matrix threshold, or impact category, document the change and recalibrate historical scores. Without version control, trend comparisons become unreliable and audit trails break down.

-

Use scores to drive resource allocation. A risk register full of scores that never influences staffing, budget, or control investment is a documentation exercise. The output of scoring should directly inform which risks receive treatment resources in the next planning cycle.

A step-by-step risk assessment framework helps institutions build these practices into repeatable processes rather than relying on individual expertise.

Key takeaways

Risk scoring is only as reliable as the methodology, governance, and calibration behind it. Institutions that treat it as a structured decision tool rather than a measurement exercise extract the most value from it.

| Point | Details |

|---|---|

| Core formula | Risk Score = Likelihood × Impact, typically on a 1–5 scale producing a 1–25 range. |

| Inherent vs. residual | Track both scores side by side to measure control effectiveness and direct treatment planning. |

| Scale governance | Define likelihood and impact with measurable anchors to prevent assessor inconsistency. |

| Workflow integration | Embed scoring into risk registers, BIA outputs, and response planning for decision-driven results. |

| Version control | Document every methodology change to preserve reliable trend analysis over time. |

Risk scoring informs decisions. it does not make them.

After working with risk programs across financial institutions of varying sizes, the pattern I see most often is this: institutions invest in building a scoring model and then treat the output as the answer. It is not. A score of 18 tells you a risk deserves attention. It does not tell you whether to accept, transfer, mitigate, or escalate it. That judgment requires context the model cannot hold.

The most effective risk programs I have observed use scoring as a filter, not a verdict. They run scores through a governance layer where experienced risk officers apply institutional knowledge, regulatory context, and strategic priorities before any response decision is made. The score gets you to the right conversation faster. It does not replace the conversation.

The other trap worth naming is the residual score illusion. Institutions frequently assign residual scores based on the existence of controls rather than the tested effectiveness of those controls. A policy document is not a control. A control that has not been tested in the past 12 months is an assumption. When residual scores are built on untested assumptions, the entire prioritization framework is built on the same foundation.

Track both inherent and residual scores. Test your controls on a schedule that matches the velocity of the risks they are meant to address. And when your scoring methodology changes, version it. The ability to compare scores across time is one of the most undervalued outputs of a mature risk program.

— Raj

How Riskinmind supports consistent risk scoring at scale

Financial institutions that want to move beyond spreadsheet-based scoring need tools built for the complexity of credit risk, regulatory compliance, and portfolio monitoring simultaneously. Riskinmind's AI-powered platform applies structured risk scoring models directly to loan applications and commercial real estate portfolios, replacing manual inputs with real-time data analysis and standardized scoring criteria.

The platform's loan application risk scoring tool applies predictive analytics to each application, producing consistent scores that reflect current portfolio risk and regulatory thresholds. For CRE exposure, the CRE Loan Risk Predictor delivers scenario-based scoring that accounts for market conditions, concentration risk, and borrower financials. Both tools operate within Riskinmind's SOC 2® certified environment, with response times under half a second. Request a demo to see how automated, governance-quality scoring works in practice.

FAQ

What is the risk scoring definition in financial institutions?

Risk scoring is the process of assigning numeric or categorical ratings to risks based on likelihood and impact, enabling comparison, prioritization, and tracking over time. In financial institutions, it is applied to credit risk, operational risk, cybersecurity risk, and regulatory compliance.

How do you calculate a basic risk score?

The standard formula is Risk Score = Likelihood × Impact, with each variable rated on an ordinal scale such as 1–5. The resulting score is then mapped to a categorical band: low, moderate, high, or critical.

What is the difference between inherent and residual risk scores?

Inherent risk is scored before any controls are applied. Residual risk reflects what remains after controls are in place. Tracking both scores side by side shows how much risk reduction your control environment is actually delivering.

Why does risk scoring sometimes produce unreliable results?

Inconsistent scale definitions are the primary cause. When likelihood and impact are not defined with measurable anchors and specific timeframes, different assessors assign different scores to identical risks, which undermines prioritization accuracy.

How does NIST integrate risk scoring into enterprise risk management?

NIST IR 8286 connects risk scoring to business impact analysis outputs, using BIA-derived asset criticality and impact thresholds to calibrate the impact dimension of each risk score. This ensures that scoring priorities reflect what the institution has formally determined it cannot afford to lose.