Risk process automation is defined as the use of specialized software, AI, machine learning, and robotic process automation (RPA) to identify, assess, monitor, and mitigate risks with minimal manual intervention. For credit unions, community banks, and lenders operating under intensifying regulatory scrutiny, this shift from spreadsheet-driven workflows to automated risk management is no longer optional. Platforms like Riskinmind now deploy AI agents that handle credit risk assessment, compliance monitoring, and portfolio analysis in real time, compressing tasks that once took weeks into processes measured in minutes. The result is continuous risk visibility, fewer human errors, and a compliance posture that keeps pace with regulatory change rather than chasing it.

What is risk process automation and how does it work?

Risk process automation applies AI, machine learning, and RPA to create centralized, real-time risk registers that trigger workflows automatically when risk thresholds are crossed. Rather than relying on periodic manual reviews, the system continuously ingests data from multiple sources, scores risks against predefined criteria, and dispatches alerts or remediation tasks without human prompting. This architecture transforms risk management from a reactive, calendar-driven exercise into a continuous, data-driven discipline.

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

The core components of an automated risk management system each serve a distinct function. Automated risk identification scans internal and external data feeds to surface emerging threats. Scoring engines apply consistent, rule-based or ML-driven criteria to rank risks by severity and likelihood. Real-time dashboards centralize findings for executive visibility, while automated alerting notifies responsible owners the moment a threshold is breached. Auto task assignment and remediation tracking close the loop by ensuring that identified risks move through resolution workflows without manual handoffs.

Integration with existing enterprise systems is what makes this architecture practical for financial institutions. Automated platforms connect to ERP systems, CRM platforms, loan origination systems, and regulatory compliance tools, pulling data from each to build a unified risk picture. This eliminates the data silos that make manual risk management so fragmented and slow.

| Component | Primary benefit |

|---|---|

| Real-time risk register | Continuous visibility across all risk categories |

| Automated scoring engine | Consistent, objective risk prioritization |

| Threshold-triggered alerts | Immediate notification before risks escalate |

| Auto task assignment | Faster remediation with clear accountability |

| Executive dashboards | Proactive decision support for leadership |

Pro Tip: When evaluating automation platforms, confirm that the system supports bidirectional integration with your core banking or loan origination system. One-way data pulls create blind spots that undermine the continuous monitoring value you are paying for.

How does automation compare to traditional manual risk management?

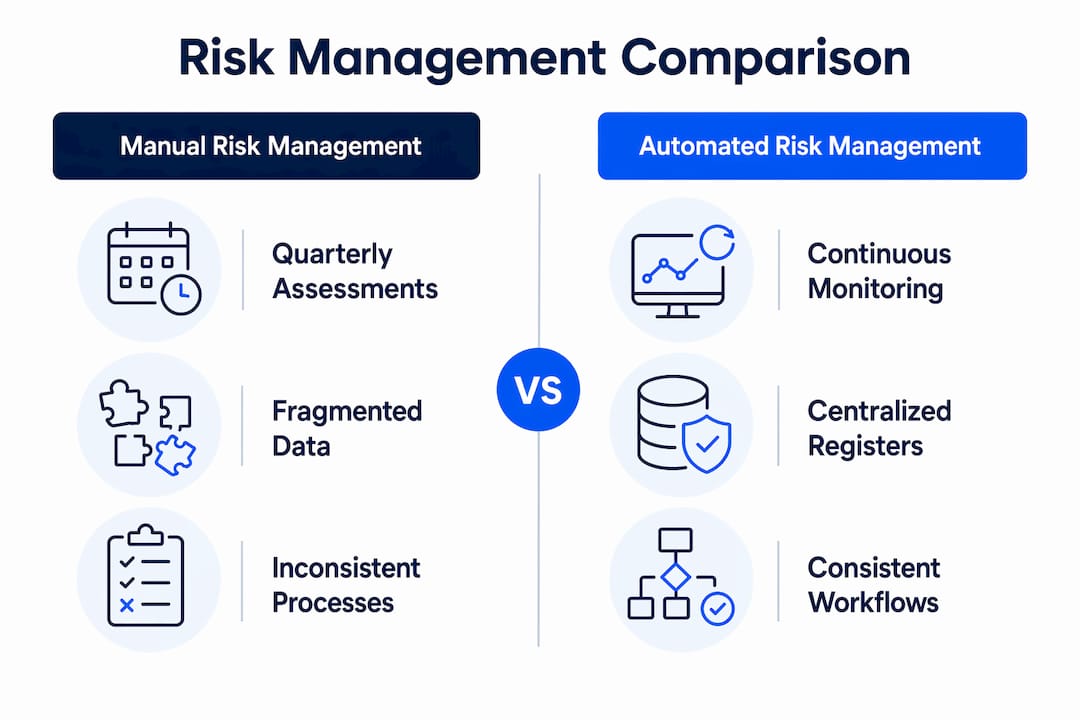

Manual risk management in financial institutions typically means fragmented spreadsheets, quarterly assessments, and risk data scattered across departments that rarely communicate in real time. Automated risk assessment workflows reduce financial processing errors by up to 75% compared to these manual methods, and they compress complex multi-framework assessments from weeks to under one hour. That compression is not just a time saving. It means your institution can respond to a credit risk signal or a compliance gap before it becomes a regulatory finding or a loss event.

Consistency is the second major advantage. Human analysts apply judgment differently depending on workload, experience, and fatigue. Automated scoring engines apply the same criteria to every assessment, every time, which produces defensible, auditable outputs. Automated dashboards and reporting enable executive visibility and proactive risk management, replacing the static monthly report with a live picture that updates as conditions change.

Audit readiness is a direct byproduct of this consistency. When every risk assessment follows the same documented workflow and every decision is logged with a timestamp and a data citation, your institution enters an examination with a complete, organized record rather than a collection of manually assembled files.

| Feature | Traditional manual methods | Automated risk management |

|---|---|---|

| Assessment frequency | Quarterly or annual | Continuous, real-time |

| Error rate | High, human-dependent | Up to 75% reduction |

| Audit trail | Manually assembled | Automatically generated |

| Response time | Days to weeks | Minutes to hours |

| Consistency | Variable by analyst | Uniform across all assessments |

| Executive visibility | Periodic reports | Live dashboards |

Pro Tip: The most common transition pitfall is running automated and manual processes in parallel for too long. Set a firm cutover date for each risk domain, because parallel processes create conflicting records and confuse audit trails during examinations.

What challenges should financial institutions consider when implementing risk automation?

The most consequential risk in adopting automation is the assumption that it replaces human judgment entirely. Final risk acceptance and strategic decisions must remain with qualified human professionals, even when automation handles the analysis. Regulators at the OCC, FDIC, and Federal Reserve have made clear that accountability for risk decisions cannot be delegated to an algorithm. Automation handles the data; your risk officers own the conclusions.

Aligning the platform with your institution's specific risk appetite and regulatory obligations is equally critical. A community bank operating under CAMELS ratings has different threshold requirements than a credit union managing member concentration risk. Effective automation success depends on aligning tools with organizational objectives and maintaining continuous expert oversight. Deploying a generic platform without this calibration produces alerts that are either too frequent to act on or too infrequent to catch real problems.

Governance and security requirements add another layer of complexity. Automation platforms must maintain immutable logs with complete citation trails for AI findings, supporting defensible compliance and mitigating the risk of algorithmic errors or disputes. Role-based access controls, data encryption at rest and in transit, and audit trail integrity aligned to standards like SOC 2 and ISO 27001 are non-negotiable for regulated institutions.

Common implementation challenges and their mitigations include:

- Data quality gaps. Automation amplifies whatever data quality exists in your source systems. Conduct a data governance audit before deployment, not after.

- Change resistance from risk staff. Frame automation as a tool that removes low-value data entry, freeing analysts for judgment-intensive work. Staff who understand this transition adapt faster.

- Scope creep during rollout. Start with one risk domain, such as credit risk or vendor risk, and prove value before expanding. Attempting full automation across all domains simultaneously creates integration failures and delays.

- Inadequate testing of threshold logic. Threshold settings that are too sensitive generate alert fatigue. Calibrate scoring rules against at least 12 months of historical data before going live.

- Governance gaps post-deployment. Assign a named owner for each automated workflow and schedule quarterly reviews of threshold logic to reflect changing risk conditions.

Pro Tip: Treat your automation platform as a regulated system, not just a productivity tool. Document the rationale for every threshold setting and scoring weight, because examiners will ask.

What are the practical benefits of risk automation in financial institutions today?

Automation in operational risk management can save up to 30% in operational losses within five years through efficiency gains and error reduction. AI and ML models detect complex fraud patterns and threat signals that exceed human analytical capacity, particularly in high-volume transaction environments where manual review is simply not scalable. For community banks and credit unions managing lean risk teams, this capability represents a structural improvement in resilience.

Vendor risk management is one of the most immediate use cases. Continuous automated monitoring pulls fresh security and financial health information on third-party vendors, surfacing risks early rather than waiting for delayed quarterly assessments. When a vendor's cybersecurity posture deteriorates or a financial stress signal appears, the system generates an alert and assigns a review task automatically, giving your institution time to act before a third-party incident becomes your institution's problem.

Agentic AI systems now manage the full compliance lifecycle in financial services, handling real-time data ingestion, model management, alert triage, and investigations. This represents a meaningful evolution beyond simple workflow automation. Rather than executing predefined rules, agentic systems reason across data sources and adapt their responses to novel situations, which is particularly valuable for institutions managing BSA/AML compliance, fair lending analysis, and CRA documentation simultaneously.

Automation also supports continuous documentation for frameworks like SOC 2, ISO 27001, and GDPR. Instead of assembling compliance evidence manually before an audit, automated platforms generate and store documentation as a byproduct of normal operations. The audit package is always current.

| Application area | Benefit realized |

|---|---|

| Vendor risk management | Continuous monitoring replaces delayed quarterly reviews |

| Compliance lifecycle | Real-time documentation and alert triage |

| Credit risk assessment | Faster, consistent scoring across the full portfolio |

| Operational risk | Up to 30% reduction in operational losses over five years |

| Fraud detection | AI/ML pattern recognition beyond manual analytical capacity |

For institutions exploring automated risk assessment implementation, the practical starting point is identifying the risk domain with the highest manual workload and the clearest data inputs. That combination produces the fastest, most measurable return.

Key takeaways

Risk process automation delivers measurable efficiency, compliance, and resilience gains only when AI-driven workflows are paired with disciplined human oversight and governance structures calibrated to the institution's specific risk appetite.

| Point | Details |

|---|---|

| Core definition | Automation uses AI, ML, and RPA to continuously identify, score, and remediate risks without manual intervention. |

| Efficiency gains | Automated workflows reduce processing errors by up to 75% and compress multi-framework assessments from weeks to under one hour. |

| Human oversight is non-negotiable | Final risk acceptance and regulatory accountability must remain with qualified human professionals, not algorithms. |

| Governance requirements | Platforms must maintain immutable audit logs, role-based access, and encryption aligned to SOC 2 and ISO 27001 standards. |

| Operational savings | Automation in operational risk management can reduce operational losses by up to 30% within five years. |

Why automation without governance is the real risk

I have spent years watching financial institutions approach risk automation as a technology procurement decision rather than a governance transformation. The institutions that get the most from automation are not the ones with the most sophisticated platforms. They are the ones that spent time before deployment defining who owns each automated workflow, what the escalation path looks like when an alert fires, and how threshold logic will be reviewed as conditions change.

The institutions that struggle are the ones that treated deployment as the finish line. They automated data collection and alert generation, then discovered that no one had clear authority to act on the outputs. Automation without governance does not reduce risk. It relocates it.

The deeper insight I would offer to CROs and risk committee chairs is this: automation is not a cost-cutting measure dressed up as a resilience strategy. It is a genuine resilience strategy that happens to reduce costs. The distinction matters because it changes how you resource the implementation. Governance, training, and threshold calibration are not overhead. They are the mechanism by which automation actually works. Institutions that treat those elements as secondary will find that their automated platform produces noise rather than signal.

For leaders in community banks and credit unions, the practical advice is to start with AI risk management best practices before selecting a platform. Clarity on your risk appetite, your regulatory obligations, and your team's capacity to act on automated outputs will determine which platform fits, not the other way around.

— Raj

See how Riskinmind automates risk management for financial institutions

Riskinmind is built specifically for credit unions, community banks, and lenders that need enterprise-grade risk automation without the complexity of a generic enterprise platform. The platform's AI agents, coordinated by a central AI director named Ava, handle credit risk assessment, regulatory compliance monitoring, and portfolio analysis in real time, with response times under half a second and SOC 2 certification backing every workflow.

If your institution is ready to move from quarterly manual reviews to continuous, automated risk visibility, Riskinmind provides the AI-powered risk management infrastructure to make that transition with confidence. The platform integrates with existing core banking systems and delivers live dashboards, automated regulatory reporting, and audit-ready documentation from day one.

FAQ

What is risk process automation in simple terms?

Risk process automation is the use of AI, machine learning, and RPA software to continuously identify, score, monitor, and remediate risks without manual data entry or periodic manual reviews. It replaces fragmented spreadsheet-based workflows with centralized, real-time systems that trigger actions automatically when risk thresholds are crossed.

How does risk automation reduce compliance gaps?

Automated platforms generate compliance documentation as a byproduct of normal operations, maintaining continuous audit trails and real-time dashboards that keep institutions examination-ready at all times. This eliminates the manual evidence-assembly process that typically precedes regulatory audits.

Can automation replace human risk judgment entirely?

No. Final risk acceptance and strategic decisions must remain with qualified human professionals, as regulators at the OCC, FDIC, and Federal Reserve hold institutions accountable for risk outcomes regardless of the tools used. Automation handles analysis and workflow execution; humans own the decisions.

What is the typical ROI of automating risk processes?

Automation in operational risk management can reduce operational losses by up to 30% within five years, while also compressing multi-framework risk assessments from weeks to under one hour and cutting processing errors by up to 75%.

Where should a financial institution start with risk automation?

Start with the risk domain that carries the highest manual workload and the clearest, most structured data inputs, such as vendor risk management or credit risk scoring. Proving measurable value in one domain before expanding reduces integration risk and builds internal confidence in the technology.