A credit score is a three-digit number that predicts how likely you are to repay borrowed money on time. Lenders use this number, which ranges from 300 to 850, to decide whether to approve your loan and at what interest rate. The score specifically estimates the probability of missing a payment by 90 or more days within the next 24 months. Three major credit bureaus, Equifax, Experian, and TransUnion, compile the underlying credit report data. The FICO scoring model, the most widely used standard in American lending, translates that data into the number lenders see.

What is credit scoring and how does it work?

Credit scoring is the process of converting your borrowing and repayment history into a single numerical risk indicator. The model does not measure your wealth or your income. It measures your behavior with credit over time. Lenders report your credit activity to Equifax, Experian, and TransUnion, and those bureaus feed that data into scoring formulas.

The FICO model is the dominant standard, though VantageScore is also widely accepted. Both models read the same underlying credit report data but weight the factors slightly differently. The output is a score that lets a lender rank you against millions of other borrowers in seconds. Credit scoring models rank borrower risk statistically rather than predict a specific default event. That distinction matters: a score of 750 does not guarantee you will repay, but it signals you are statistically far less likely to miss payments than a borrower at 580.

Understanding the mechanics of credit scoring gives you real control over your financial profile. When you know what drives the number, you can make deliberate choices that move it in the right direction.

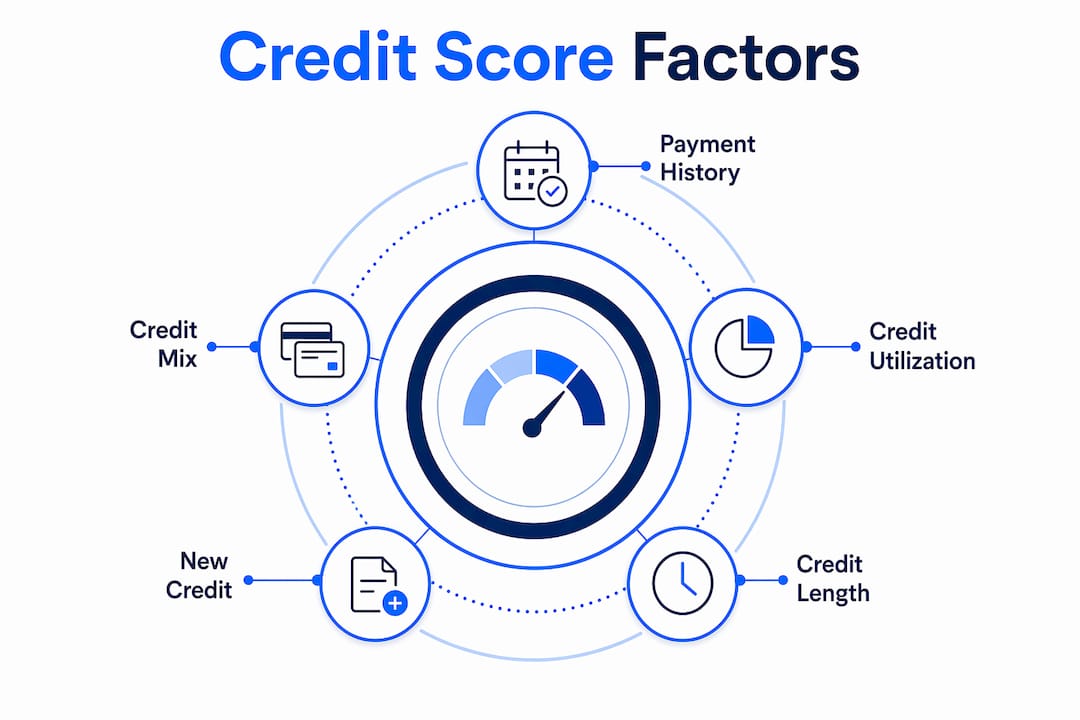

What factors influence your credit score?

Five categories determine your credit score, and each carries a different weight in the FICO model.

- Payment history (35%): This is the single largest factor. One missed payment, especially one that goes 30 or more days past due, can drop your score significantly.

- Amounts owed (30%): This measures your credit utilization ratio, which is the percentage of your available revolving credit you are currently using. Payment history and amounts owed together account for 65% of your FICO score, making them the two factors worth protecting most aggressively.

- Length of credit history (15%): Older accounts raise your average account age and signal stability to lenders.

- Credit mix (10%): A combination of installment loans (auto, mortgage) and revolving credit (credit cards) shows you can manage different debt types.

- New credit (10%): Each hard inquiry from a new credit application creates a small, temporary dip in your score.

Your credit utilization ratio deserves special attention. Financial experts recommend keeping utilization below 30%, and borrowers with the highest scores typically stay under 10%. If your total credit limit across all cards is $10,000 and your balance is $3,500, your utilization sits at 35%, which is above the recommended threshold.

Pro Tip: Pay your credit card balance down before the statement closing date, not just the due date. Issuers report your balance to the bureaus on the closing date, so a lower balance at that moment directly reduces your reported utilization.

Late payments create damage that compounds over time. A single 90-day late payment can stay on your credit report for seven years. The impact fades gradually, but the record remains. Consistent on-time payments are the most reliable path to a strong score.

How does your credit score affect loans and interest rates?

Your credit score is the primary input lenders use to price risk. Higher credit scores yield better loan terms and lower interest rates because lenders see less risk in lending to you. This practice is called risk-based pricing, and it means two borrowers taking out the same mortgage can pay dramatically different rates based solely on their scores.

The financial impact of a score difference is not trivial. On a 30-year mortgage, a borrower with a score in the 760–850 range can receive an interest rate that is a full percentage point or more lower than a borrower in the 620–639 range. Over the life of the loan, that gap translates to tens of thousands of dollars in additional interest paid.

Credit scores affect more than just mortgage and auto loans. They shape your financial life in several practical ways:

- Credit card offers: Higher scores unlock cards with lower APRs, better rewards, and higher credit limits.

- Rental applications: Many landlords run credit checks. A low score can result in a higher security deposit or outright denial.

- Personal loan rates: Unsecured personal loans carry higher rates by default, and a low score pushes those rates even higher.

- Auto loans: Dealership financing and bank auto loans both use your score to set the rate. A score below 600 often means subprime rates.

The importance of credit scores extends to insurance premiums in many states, where insurers use credit-based insurance scores to set rates. Your score is not just a borrowing tool. It is a financial reputation that follows you across multiple life decisions.

Pro Tip: Before applying for a major loan, check your credit report at AnnualCreditReport.com for errors. A single reporting mistake can suppress your score by 20 or more points and cost you a better rate.

What are common misconceptions about credit scores?

Several persistent myths cause people to make decisions that hurt their scores. Getting these facts straight protects your financial standing.

The most common misconception is that income affects your credit score. Credit scores do not consider income, employment, race, religion, or gender. The formula relies exclusively on credit behavior data. A high-earning professional with a history of missed payments will score lower than a modest-income borrower who pays on time every month.

A second misconception is that checking your own score hurts it. Checking your own credit generates a soft inquiry, which has no impact on your score. Only hard inquiries from lenders, triggered when you apply for new credit, create a temporary dip. You can check your score as often as you like without any penalty.

A third misconception involves closing old accounts. Closing old credit card accounts can harm your score by shortening your average credit history length and reducing your total available credit. Both changes push your utilization ratio up and your average account age down. If you want to stop using a card, consider leaving the account open with a zero balance instead.

Finally, many people believe they need to pay for their credit score. Free credit scores are widely available through banks, credit unions, and credit card issuers. Paying for a score rarely provides information you cannot access at no cost.

How can you improve and maintain a healthy credit score?

Improving your credit score is a process of building consistent habits over time. There are no shortcuts, but the steps are straightforward.

- Pay every bill on time. Set up autopay for at least the minimum payment on every account. One missed payment can undo months of progress. Payment history carries more weight than any other factor.

- Reduce your credit card balances. Target a utilization rate below 30% on each individual card and across all cards combined. Paying down balances is the fastest lever most borrowers can pull to raise their score.

- Avoid opening new accounts unnecessarily. Each application triggers a hard inquiry and lowers your average account age. Apply for new credit only when you have a clear need.

- Keep old accounts open. The length of your credit history accounts for 15% of your FICO score. An old card with no annual fee is worth keeping active with a small recurring charge.

- Build a diverse credit mix responsibly. If you only have credit cards, a small installment loan (such as a credit-builder loan from a credit union) adds a new credit type to your profile. Do not take on debt purely for the mix benefit unless the terms make financial sense.

- Monitor your credit reports regularly. You are entitled to free reports from all three bureaus. Review them at least once a year for errors, fraudulent accounts, or outdated negative items that should have aged off.

For borrowers exploring how risk scoring works in lending, the same principles that govern individual credit scores also underpin the models financial institutions use to evaluate entire loan portfolios.

Key Takeaways

A credit score is a statistical risk indicator, and the behaviors that build it, on-time payments, low utilization, and long account history, are the same behaviors that produce long-term financial stability.

| Point | Details |

|---|---|

| Score range and purpose | Credit scores run from 300 to 850 and predict the likelihood of missing a payment within 24 months. |

| Top two factors | Payment history (35%) and amounts owed (30%) together drive 65% of your FICO score. |

| Utilization threshold | Keep credit utilization below 30%, and aim under 10% for the best scores. |

| Score affects more than loans | Credit scores influence rental approvals, insurance premiums, and credit card terms, not just loan rates. |

| Free access to scores | Free credit scores are available through most banks and credit unions, making paid score services unnecessary. |

Credit scores are more than a number

I have spent years watching people treat their credit score as a report card they check once and forget. That framing is the wrong one. A credit score is a living signal. It changes every month based on what you do or do not do with your credit accounts.

The detail that most people miss is the gap between understanding the rules and actually acting on them. Knowing that utilization matters is not the same as checking your balance before the statement closes. The borrowers who consistently land in the 750-plus range are not necessarily the wealthiest. They are the most deliberate. They pay early, keep balances low, and leave old accounts open even when the card sits unused in a drawer.

The FICO model has real limitations, which is worth acknowledging. The FICO Resilience Index was developed specifically because traditional scores do not fully capture how a borrower holds up during economic stress. That supplemental tool, along with modern credit risk modeling approaches, reflects a broader shift in how lenders are thinking about risk beyond a single three-digit number.

My honest advice: treat your credit score as a habit tracker, not a grade. The number is just the output. The inputs are your daily financial behaviors, and those are entirely within your control.

— Raj

Riskinmind's AI-powered approach to credit risk

Credit scoring gives lenders a starting point, but modern lending decisions require more depth than a single score provides.

Riskinmind's AI-powered platform is built for financial institutions that need to go further. Its specialized AI agents analyze credit risk, regulatory compliance, and portfolio behavior in real time, with processing speeds under half a second. For lenders who want to move beyond traditional scoring models, the loan application platform integrates AI-driven risk assessment directly into the underwriting workflow. Institutions looking for a broader view of their risk exposure can explore the full suite of tools at Riskinmind. The platform carries SOC 2® certification and bank-grade security, making it a credible choice for credit unions, community banks, and commercial lenders.

FAQ

What is a good credit score range?

A score of 670 or above is generally considered good by most lenders, while scores above 740 qualify for the best loan rates. The full scale runs from 300 to 850.

How does credit scoring work for first-time borrowers?

First-time borrowers have a thin credit file, which means limited data for scoring models to evaluate. Starting with a secured credit card or a credit-builder loan establishes the payment history needed to generate a score.

Does checking your credit score lower it?

Checking your own credit score generates a soft inquiry and does not affect your score at all. Only hard inquiries from lender applications create a temporary, small decrease.

How long does it take to improve a credit score?

Meaningful improvement typically takes three to six months of consistent on-time payments and reduced utilization. Recovering from serious negative items like collections or late payments takes longer, often one to two years.

What is the difference between FICO and VantageScore?

Both FICO and VantageScore use the same 300–850 scale and similar factor categories, but they weight those factors differently and use different minimum scoring criteria. FICO requires at least six months of credit history, while VantageScore can generate a score with as little as one month of data.