Risk management professionals at financial institutions know the difference between tracking risk and truly managing it. Yet when evaluating software, many teams conflate basic risk assessment software with what is enterprise-grade risk platform technology built for regulatory scrutiny, multi-entity complexity, and board-level accountability. The gap between the two is not marginal. It affects compliance posture, capital allocation decisions, and your institution's ability to act on risk signals before they become losses. This article breaks down what separates enterprise-grade from everything else.

Table of Contents

- Key takeaways

- What defines an enterprise-grade risk platform

- Frameworks that shape enterprise risk platforms

- Cloud-native delivery and 2026 platform innovations

- Practical applications in financial institutions

- ERM vs. GRC vs. IRM: getting the terminology right

- My perspective on adopting enterprise-grade risk platforms

- How Riskinmind delivers enterprise-grade risk capabilities

- FAQ

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

Key takeaways

| Point | Details |

|---|---|

| Enterprise-grade means integration | True platforms span operational, credit, cyber, and compliance risks in a single aggregated view. |

| Frameworks drive platform design | COSO ERM 2017 and ISO 31000 shape how enterprise platforms handle risk appetite, taxonomy, and board reporting. |

| Cloud-native delivery changes the game | CI/CD architecture means risk models stay current without disruptive patch windows or downtime. |

| Automation reduces manual burden | Automated workflows can cut time spent on risk assessments by up to 80% annually. |

| ERM and GRC are not the same | Enterprise risk platforms support strategic judgment; GRC tools handle compliance execution. |

What defines an enterprise-grade risk platform

At its core, an enterprise-grade risk platform is a technology system designed to aggregate, assess, monitor, and report risk across an entire financial institution, not just one department or risk type. The word "enterprise" is doing real work here. It signals architecture built for scale, governance requirements, and multi-dimensional risk visibility that a spreadsheet-based process or a standalone compliance tool simply cannot provide.

The defining capabilities tend to cluster around six dimensions:

- Integrated risk coverage. A genuine enterprise risk management platform addresses operational, strategic, compliance, financial, and cyber risks within a single data environment. Siloed tools that handle only credit risk or only regulatory reporting do not qualify.

- Continuous and automated risk assessment. Automated risk assessment workflows reduce manual touchpoints throughout the risk cycle. Platforms like Resilience Arc, launched in May 2026, demonstrate that portfolio-level cyber risk visibility with multi-entity aggregation can reduce manual assessment time by 80% annually.

- Portfolio-level aggregation. For institutions managing multiple business lines, subsidiaries, or loan portfolios, the platform must roll up individual risk exposures into an institution-wide view that supports strategic decisions.

- Cloud-native architecture with CI/CD delivery. FIS launched its Enterprise Risk Suite on AWS in May 2026, enabling financial institutions to always run the latest platform version without operational downtime. That model represents where enterprise-grade risk technology is heading.

- Scalability for peak workloads. Microservice-based cloud architecture allows institutions to scale risk calculations linearly and deploy burst computing during stress testing or regulatory reporting cycles, without degrading system performance.

- Role-based access and cross-organizational collaboration. Enterprise platforms support operational staff, risk teams, compliance officers, and board risk committees using the same system with access appropriately scoped to each role.

Pro Tip: When evaluating platforms, ask vendors specifically how risk data flows from the operational level to the board reporting layer. Platforms that require manual export and reformatting at each step are not truly enterprise-grade.

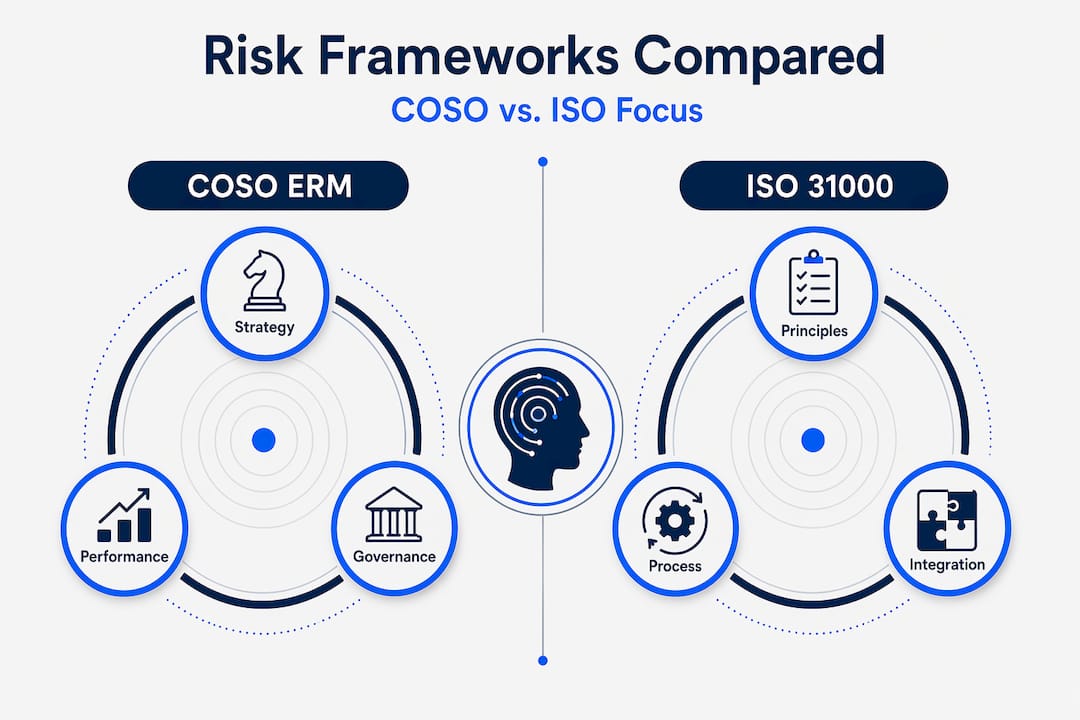

Frameworks that shape enterprise risk platforms

Understanding what is enterprise-grade risk software requires understanding the frameworks it must operationalize. Two standards dominate: COSO ERM 2017 and ISO 31000:2018.

The COSO ERM framework updated in 2017 directs organizations to connect risk management explicitly with strategy and performance, placing board oversight and management accountability at the center. It emphasizes identifying potential events, managing risks within defined appetite, and providing reasonable assurance around objective achievement. ISO 31000 takes a principles-based approach that is broader in scope and applicable across industries, but both frameworks converge on one point: risk management must be embedded in strategic decision-making processes, not bolted on as a compliance afterthought.

Enterprise-grade platforms are designed to operationalize these requirements directly. They provide structured support for risk appetite statements, risk taxonomy management, scenario-based modeling, and board-ready reporting. A platform that cannot translate your institution's risk appetite into monitored thresholds tied to real portfolio data is not enterprise-grade, regardless of what the marketing materials claim.

| Framework | Primary focus | Best suited for |

|---|---|---|

| COSO ERM 2017 | Strategy integration, performance alignment, board oversight | U.S.-based financial institutions with SEC/regulatory obligations |

| ISO 31000:2018 | Principles-based, adaptable risk management processes | Institutions seeking a universal, flexible framework |

| GRC platforms | Compliance control execution, audit evidence management | Regulatory reporting, policy management, audit readiness |

Pro Tip: Your platform selection should map directly to the framework your institution's board has adopted. Misalignment between the software's taxonomy and your governance structure creates reporting gaps that examiners will find.

Cloud-native delivery and 2026 platform innovations

The shift from on-premise installations to cloud-native, continuously delivered platforms represents the most consequential change in enterprise-grade risk technology in the past decade. The operational implications for financial institutions are significant.

Traditional risk platforms required scheduled upgrade windows that interrupted operations, froze reporting cycles, and frequently introduced compatibility issues. CI/CD-managed upgrades eliminate that pattern entirely. Risk calculations remain current, model updates deploy without patch windows, and institutions maintain continuous alignment with the latest regulatory guidance and market conditions. For institutions under ongoing examiner scrutiny, that continuity matters.

The architectural advantages extend beyond uptime. Consider these concrete benefits for financial institution risk teams:

- Burst computing for stress testing. Regulatory stress tests and CECL calculations require processing volumes that spike dramatically above baseline. Cloud-native microservices scale to absorb those peaks without requiring dedicated on-premise hardware investments.

- Governance and audit readiness. Every configuration change, model update, and access event in a cloud-native platform generates a traceable log, which strengthens your audit trail and supports examiner inquiries without manual reconstruction.

- Reduced infrastructure risk. On-premise hardware failures during critical reporting periods create operational risk. Cloud-native platforms shift that infrastructure responsibility to the vendor's SLA, which for institutions without large IT teams is a material operational risk reduction.

- Accelerated feature adoption. When regulators revise capital rules or stress testing methodologies, cloud-native vendors deploy updated models institution-wide without requiring each client to manage their own upgrade cycle.

The FIS Enterprise Risk Suite deployment on AWS demonstrates that cloud-native risk infrastructure agility is no longer theoretical. It is a production reality for financial institutions that choose platforms built on this architecture.

Practical applications in financial institutions

Understanding the features of risk platforms matters less than understanding what they enable your institution to actually do differently. The practical benefits of enterprise-grade risk tools manifest across four areas of financial institution operations.

-

Automated risk assessment workflows. When a community bank or credit union moves loan underwriting, concentration risk tracking, and compliance monitoring onto a unified platform, the manual handoffs between spreadsheets and email chains disappear. Risk professionals spend time on judgment, not data wrangling. The time savings are not trivial. Institutions that have deployed automated portfolio risk platforms report reductions in assessment time approaching 80%, which translates directly into faster credit decisions and more frequent risk reviews.

-

Portfolio-level cyber risk quantification. One of the most valuable and underutilized capabilities of enterprise-grade platforms is translating cyber risk into financial exposure estimates that executives and board members can act on. Continuous monitoring across your digital asset portfolio, combined with financial quantification models, closes the communication gap between your information security team and your CFO.

-

Cross-organizational alignment. Enterprise platforms give your credit team, compliance officers, finance function, and senior leadership a shared view of risk. When everyone is working from the same risk taxonomy and the same data, the institution stops having three different answers to the question "what is our current credit risk exposure?" That alignment is foundational to sound governance. For deeper context on how risk technology supports financial institutions, the structural reasons behind that alignment are worth examining.

-

Board reporting efficiency. Preparing a risk report for the board risk committee is a significant time investment for most risk teams. Enterprise platforms that connect live portfolio data to templated board reporting formats reduce that cycle from days to hours, while improving the accuracy and currency of the information directors receive.

ERM vs. GRC vs. IRM: getting the terminology right

Risk professionals evaluating platforms frequently encounter three overlapping categories: ERM software, GRC platforms, and IRM tools. The distinctions matter when choosing a solution, and conflating them leads to procurement decisions that leave critical gaps.

GRC platforms integrate governance, risk, and compliance activities, with particular strength in policy management, control testing, audit evidence collection, and regulatory reporting. They are built for compliance execution. ERM platforms, by contrast, are built for strategic risk judgment. They support risk appetite setting aligned to strategy, risk aggregation across the enterprise, and board-level portfolio reporting. The distinction matters because GRC tools can produce compliance artifacts without providing the strategic risk intelligence that senior leaders and examiners increasingly expect.

IRM, or Integrated Risk Management, is a more recent framing that attempts to bridge both functions within a single platform. For many financial institutions, an IRM-oriented enterprise platform that supports both compliance workflows and strategic risk aggregation represents the most practical architecture.

A few markers help identify which category a solution actually falls into:

- Does the platform support a formal risk appetite statement with monitored thresholds tied to portfolio data, or does it only track policy exceptions?

- Can it produce an aggregated, enterprise-wide risk profile, or does it report risk by function in isolation?

- Does it support scenario-based stress modeling, or only control status tracking?

Effective enterprise risk management software uses a shared risk taxonomy aligned with COSO or ISO frameworks to integrate ERM with GRC and audit disciplines while preserving distinct roles and artifacts. The taxonomy is the connective tissue. Without it, your GRC data and your ERM judgments live in separate worlds, and your board receives an incomplete picture.

My perspective on adopting enterprise-grade risk platforms

I've worked closely enough with financial institutions going through platform evaluations to recognize a pattern that consistently undermines the investment. The institution selects technically sound enterprise-grade risk software, deploys it competently, and then discovers six months later that the platform is being used primarily as a document repository. The features are there. The data is not flowing through them.

In my experience, the failure is almost never the technology. It is the absence of governance infrastructure around it. Before your institution selects a platform, your risk appetite statement needs to be specific enough to generate measurable thresholds. Your risk taxonomy needs executive sign-off, not just a draft in a working group folder. Without those inputs, even the most capable platform produces outputs that no one trusts or acts on.

What I've also seen is that cloud-native delivery changes the political dynamics of platform adoption in ways institutions do not anticipate. When the vendor pushes updates continuously, your risk team is always working with current models. But that also means your governance processes, your training, and your board reporting templates need to evolve continuously as well. The institutions that succeed are the ones that build that adaptability into their operating model from day one.

My core advice: choose a platform that matches your institution's strategic ambition and operational maturity, not just its current compliance requirements. The enterprise risk management frameworks you adopt should drive the platform requirements, not the other way around.

— Raj

How Riskinmind delivers enterprise-grade risk capabilities

For credit unions, community banks, and lenders looking to put the capabilities described here into practice, Riskinmind offers an AI-powered platform built specifically for financial institutions at this scale. The platform's suite of specialized AI agents handles credit risk assessment, regulatory compliance, and portfolio monitoring under the coordination of Ava, its central AI director, delivering real-time risk intelligence with response times under half a second.

Riskinmind's product suite includes the CRE Loan Risk Predictor for commercial real estate analysis, peer benchmarking tools for comparative risk positioning, and David, an AI-driven loan assessor that supports intelligent underwriting decisions. With SOC 2® certification and bank-grade security, the platform meets the compliance and data governance requirements that financial institution examiners expect. Explore the full Riskinmind platform to see how AI-powered automation transforms your institution's risk management operations.

FAQ

What is an enterprise-grade risk platform?

An enterprise-grade risk platform is a technology system that aggregates and monitors risk across an entire financial institution, supporting strategic decision-making, regulatory compliance, and board reporting from a unified data environment.

How does an enterprise risk platform differ from GRC software?

GRC software focuses on compliance control execution and audit evidence management, while an enterprise risk management platform supports strategic risk judgment, risk appetite monitoring, and portfolio-level risk aggregation aligned with frameworks like COSO ERM 2017.

What are the key features of enterprise risk platforms?

Core features of risk platforms include integrated risk coverage across multiple risk types, automated assessment workflows, cloud-native scalability, role-based access, and board-ready reporting connected to live portfolio data.

Why do financial institutions need cloud-native risk platforms?

Cloud-native delivery through CI/CD architecture keeps risk models current without disruptive upgrade cycles, supports burst computing for stress testing, and reduces infrastructure operational risk, all of which are material concerns for regulated institutions.

How do I choose the right risk platform for my institution?

To choose a risk platform, align your selection with your institution's adopted framework (COSO or ISO 31000), verify the platform supports your risk appetite statement with monitored thresholds, and confirm it scales to your portfolio complexity and regulatory reporting requirements.