Automating credit memo creation, data extraction, and risk detection for loan underwriting without increasing audit risk or burdening teams with complex workflows remains a persistent challenge for banks and lenders. Many loan risk management software platforms fail to offer true in-house model control, require heavy manual integration, or restrict transparent audit trails to top-tier plans and custom implementations. This comparison covers speed, automation coverage, policy configuration, and evidence traceability so credit and risk teams can pick the platform that cuts manual tasks without sacrificing compliance demands.

Table of Contents

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

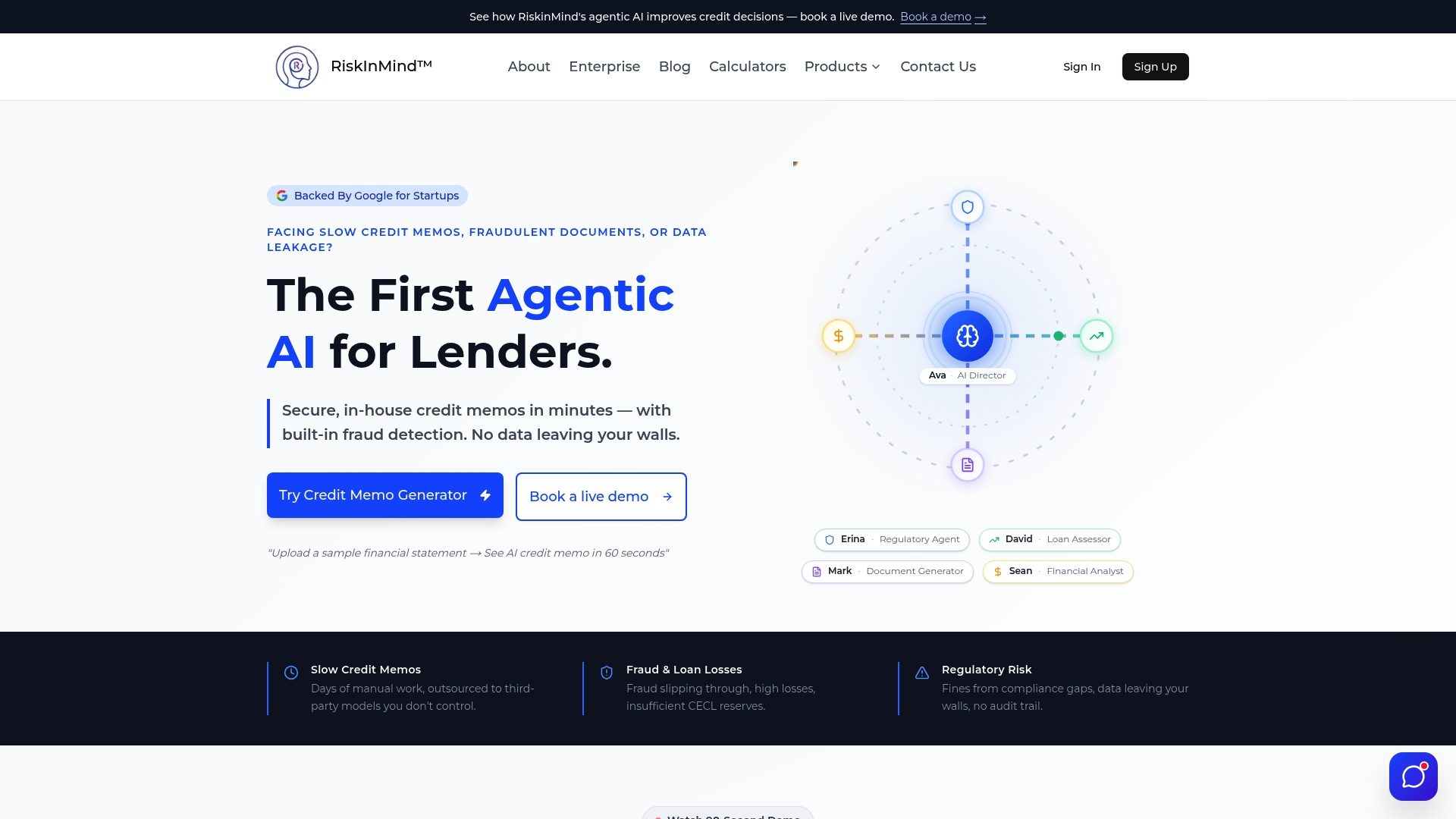

RiskinMind

At a Glance

RiskinMind's marketing materials claim 99.7% risk detection accuracy and a 0.3 second processing time for core analyses, and the vendor states SOC 2 compliance for its security posture. The platform bundles credit memo automation, fraud detection, CECL modeling, and regulatory alerts into a single workflow.

Core Features

Automates credit memos from financial statements in minutes, turning raw numbers into draft narrative and credit conclusions ready for review.

Built-in fraud and anomaly detection that triggers at the point of analysis, plus AI-driven CECL loan loss reserve modeling and management.

Real-time monitoring of regulatory changes with alerting, portfolio management insights, member visibility tools for retention work, and mobile access to dashboards and reports.

The platform uses large language models, neural networks, and machine learning to power those features and advertises sub-half-second response times for many queries.

Key Differentiator

RiskinMind centralizes credit workflow automation with in-house model control and integrated regulatory monitoring. That combination reduces handoffs between underwriting, compliance, and portfolio teams by keeping model inference and data control inside the same environment.

Pros

- Automates credit memos from statements, which shrinks manual writeup time and lets credit officers focus on judgment rather than transcription.

- The vendor emphasizes in-house control over models and data, reducing reliance on third-party model hosting and lowering some data governance risks.

- Integrated fraud and anomaly detection at analysis time reduces downstream investigation load and speeds decisioning when an alert is valid.

- Supports CECL reserve modeling alongside underwriting, so accounting and credit functions use the same modeled inputs rather than reconciling different spreadsheets.

- Scalable cloud-native infrastructure designed to handle high transaction volumes while the company highlights SOC 2 compliance and enterprise-grade security.

Cons

- Dependence on AI models means ongoing tuning and validation will be necessary for institution-specific credit types and local underwriting policies.

Who It's For

Risk managers, credit officers, and compliance officers at small to mid-sized banks and credit unions that want a single system to automate underwriting tasks, maintain audit trails, and surface regulatory change alerts without stitching multiple point tools together.

Unique Value Proposition

Automated credit memo creation in minutes powers a measurable change in workflow. With AI models running inside the platform and a single audit trail for underwriting and compliance, RiskinMind turns repetitive analyst work into review time and shortens time to decision.

Real World Use Case

A regional credit union used RiskinMind to auto-generate draft credit memos for standard consumer and small business loans, run CECL scenarios, and receive regulatory-change alerts. The institution reported faster turnarounds for routine approvals while audit logs captured decisions for examiners.

Pricing

Pricing is not publicly disclosed and appears to be tailored. The vendor typically structures commercial arrangements as enterprise or subscription contracts with integration and deployment sizing dictated by institution scale.

Website: https://riskinmind.ai

Oscilar

At a Glance

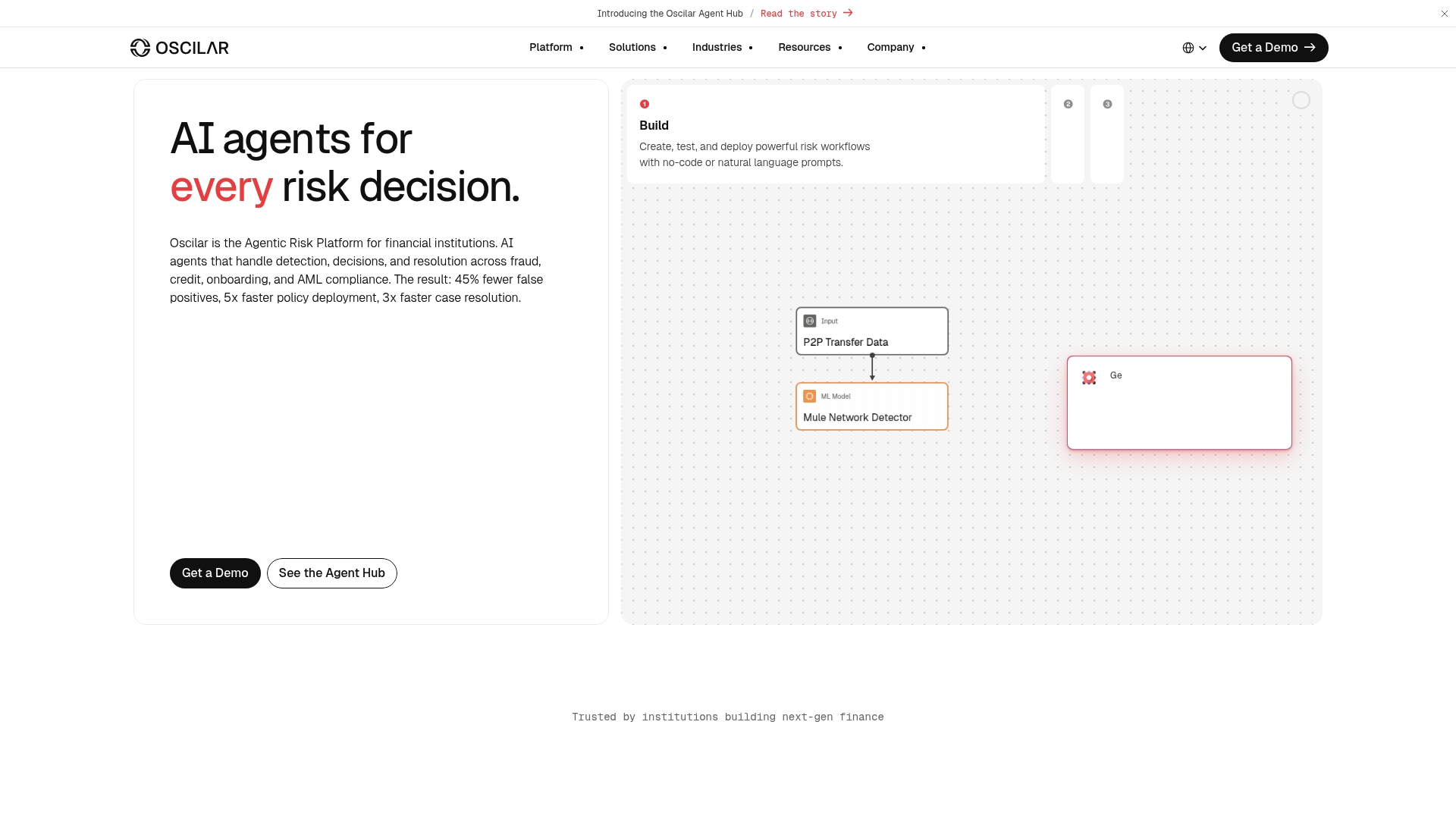

Oscilar's marketing materials position it as the first AI Risk Decisioning™ Platform that consolidates fraud detection, AML compliance, and credit underwriting into a single no-code system. It targets banks, credit unions, sponsor banks, fintechs, payments companies, and digital asset platforms.

Core Features

The platform combines no-code workflow creation, specialized AI agents, and explainable decision scoring to run onboarding, fraud, credit, and compliance flows from one interface.

The vendor advertises data enrichment via 100+ integrations, and the product includes real-time case investigation, behavioral and device biometrics, automated case prioritization, and continuous model retraining.

Key Differentiator

Oscilar centers on unified, no-code AI decisioning driven by specialized risk agents trained on client standard operating procedures. That design lets risk teams encode plain language policies and let the agents apply context-aware scoring across fraud, AML, and credit.

Adaptive machine learning is applied continuously so decision rules evolve with live feedback and new fraud patterns rather than relying solely on static rule engines.

Pros

-

Highly adaptable platform that lets compliance and risk teams build or edit workflows without deep engineering support. Deploy changes faster than reworking legacy rule engines.

-

Low-code and natural language policy editing reduces friction between legal, compliance, and operations while keeping audit trails for reviewers.

-

Real-time case investigation surfaces context rich signals and behavioral biometrics so analysts see device fingerprints and stepwise histories in one view.

-

Continuous retraining and live feedback loops mean the model learns from investigator decisions and flagged incidents over time.

-

Integrations with major identity, credit, and data providers shorten time to value and reduce manual enrichment work.

Cons

-

Steep learning curve during initial setup. Operational teams will need time and expert support to tune policies and agent behavior.

-

The vendor expects a nontrivial initial investment in training and onboarding to maximize the platform's potential for complex book structures.

-

Pricing is not publicly disclosed and appears to be bespoke per client, which complicates vendor comparisons for procurement teams.

When It May Not Fit

If you need a turnkey system that requires zero configuration, this product is likely a poor match. Oscilar assumes an initial training period to map SOPs and tune agents.

If transparent, self-serve pricing is a procurement requirement, expect friction. Smaller institutions with minimal risk engineering resources may find the implementation cost and learning curve prohibitive.

Notable Integrations

Oscilar connects to common identity, verification, and credit vendors including Plaid, Persona, Socure, LexisNexis, Experian, Equifax, TransUnion, and Jumio. Those partners support device signals, KYC checks, and credit enrichments used inside decisioning flows.

Who It's For

Risk and compliance teams at mid market to large financial institutions, sponsor banks, fintechs, and digital asset platforms that have the resources to onboard a configurable AI system and want a single platform for onboarding, fraud, credit, and AML.

Real World Use Case

A major fintech deployed Oscilar to automate onboarding and reduce false positives. Analysts reported faster case resolution as behavioral biometrics and real-time scoring removed noisy signals and routed high risk cases to specialized queues.

Pricing

Pricing is not publicly disclosed and is likely tailored per client based on scale and features. Procurement teams should request a demo and a scoped quote that maps expected decision volume and integration needs.

Website: https://oscilar.com

LenderBox

At a Glance

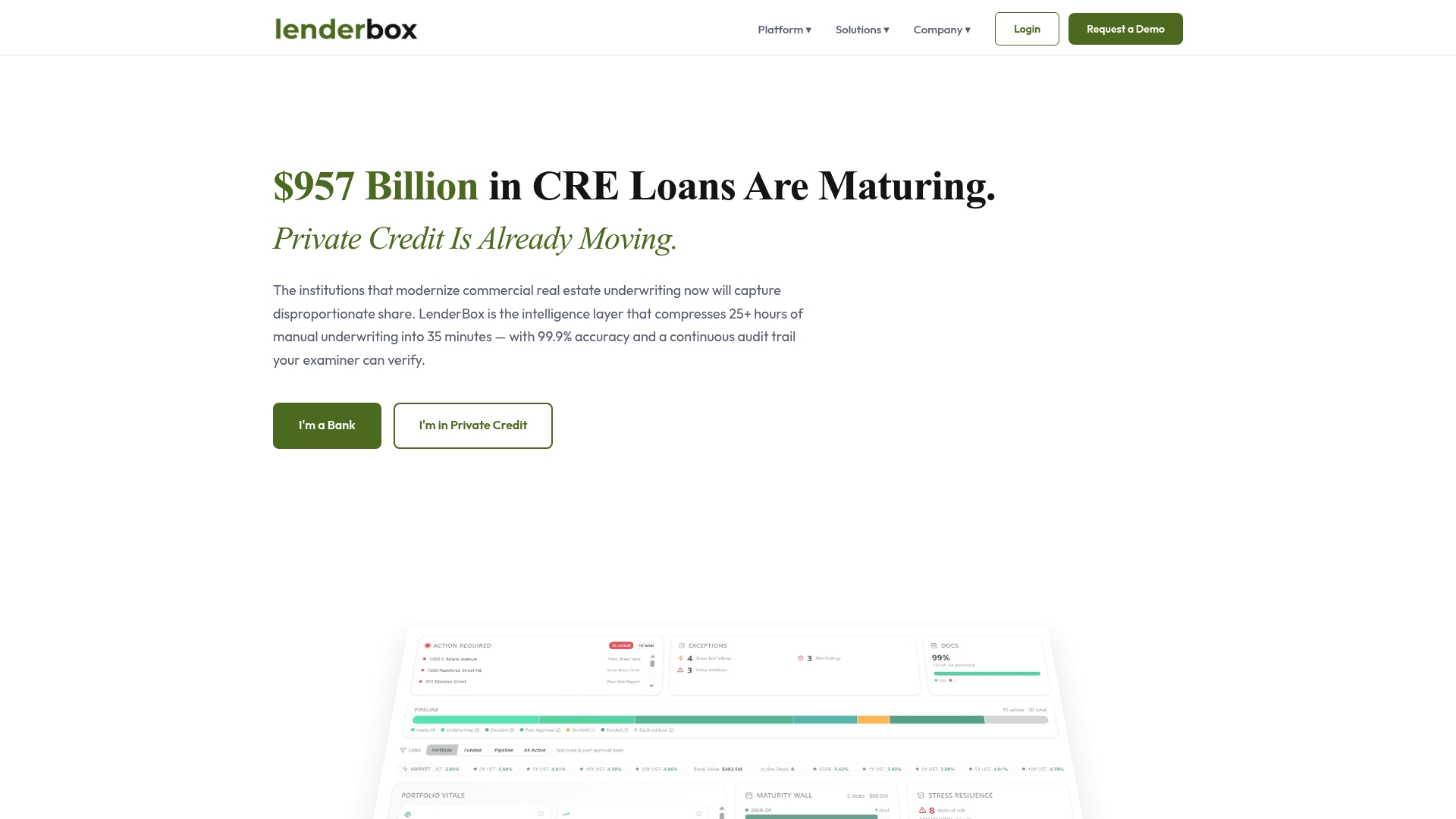

LenderBox's marketing materials claim it can generate credit memos in about 35 minutes with 99.9% accuracy. The vendor advertises SOC 2 Type II certification and bank grade encryption, positioning the product for regulated lenders that need audit trails and tight controls.

Core Features

Purpose built AI engines handle document extraction, policy enforcement, market research, risk scoring, conversational queries, and deal structuring. The extraction layer pulls over 6,000+ data points from 70 plus CRE document types and links findings to source pages for auditability.

Automatic policy checks add dual citations so compliance exceptions come with evidence. Real time market research returns cap rates, rent comps, and local property trends while portfolio monitoring tracks maturities, concentration risk, and covenant breaches.

Key Differentiator

LenderBox uses purpose-specific AI engines to automate the full CRE underwriting chain from extraction to policy enforcement and structuring. That architectural choice aims to remove handoffs between teams and produce committee ready materials faster than manual workflows.

Pros

- Accelerates underwriting dramatically when compared with manual processes; the figure above gives an explicit speed target teams can evaluate against their current cycle times.

- Automated compliance checks with dual citations reduce the work required to prepare an audit packet and create a traceable decision trail for credit committees.

- Transparent risk scores that cite source data help lending officers defend recommendations during internal review.

- Integrates with existing loan origination and CRM systems, letting teams keep legacy workflows while adding automation to specific steps.

- Built to meet regulated industry expectations and the vendor advertises SOC 2 Type II certification, which will matter to security and audit teams.

Cons

- Public user feedback is mixed; some reviews report inaccuracies in credit reporting and delays or gaps in customer support, which raises operational risk for high stakes loans.

- There is limited independent verification of the positive performance claims, so buyers will want a pilot and careful validation before wide rollout.

- A few users have flagged data security concerns and difficulty reaching responsive support during critical issue windows.

When It May Not Fit

If your team requires fully independent, third party validation of model accuracy before production use, LenderBox may be a poor match until you complete your own audits. Large banks with complex in house models and strict vendor governance will need a detailed due diligence process before adoption.

Who It's For

Small to mid sized banks and private credit teams focused on commercial real estate who want to cut manual underwriting load and produce consistent credit memos faster. Best for teams willing to run pilots and validate accuracy against known deals.

Real World Use Case

A regional bank used LenderBox to ingest CRE loan packages, run automatic policy checks, and produce committee ready files. The bank reported faster throughput and fewer manual data pulls after validating outputs on a sample of recent deals.

Pricing

Not applicable — informational only. Prospective buyers should contact LenderBox for pilot and licensing details.

Website: https://lenderbox.ai

Aloan

At a Glance

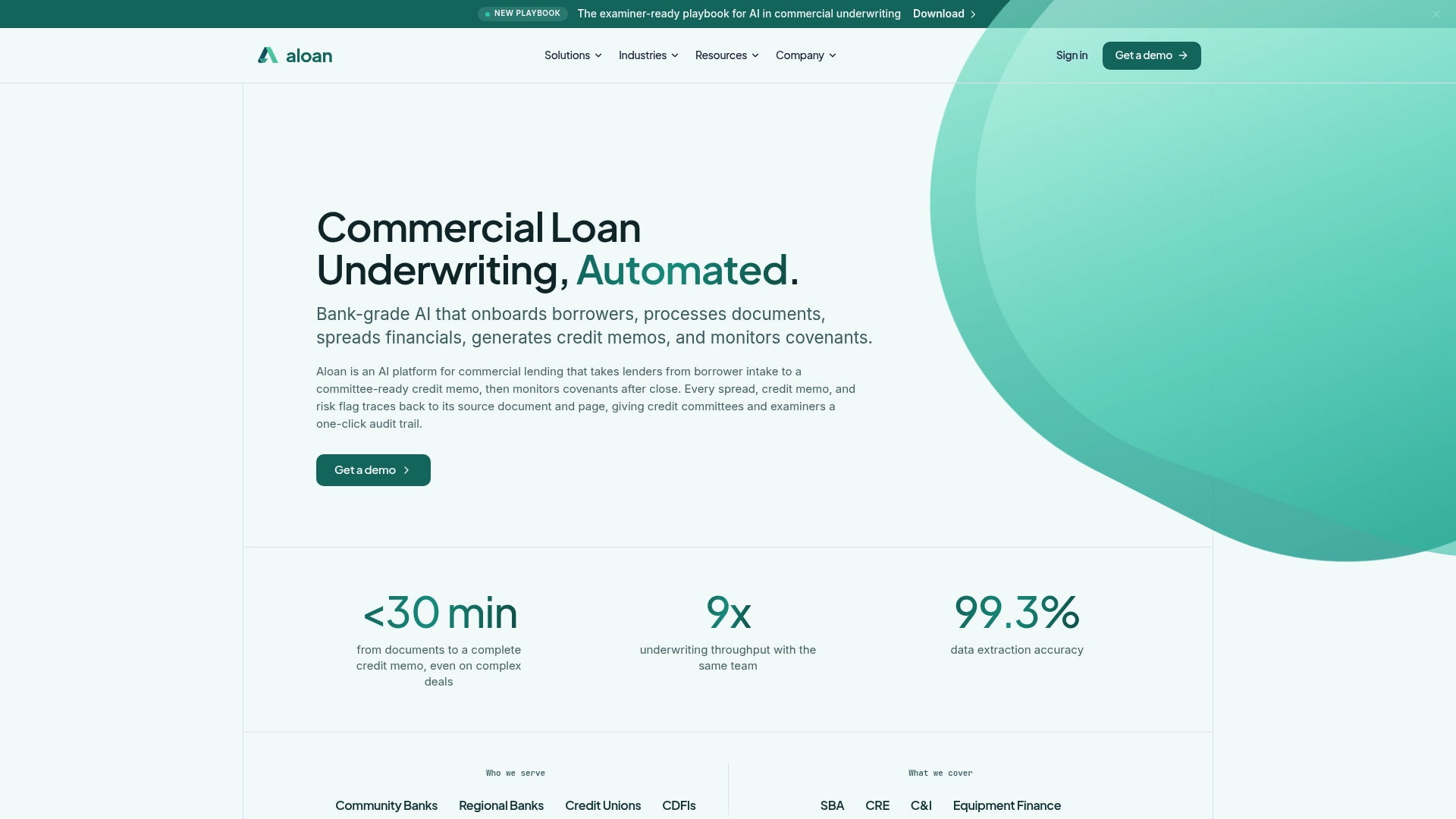

Aloan's marketing materials report 99.3% data extraction accuracy and claim up to 90% reduction in manual work, with typical deployment in 2–4 weeks. These vendor-reported figures position Aloan as an underwriting layer focused on speed, auditability, and source-traced outputs.

Core Features

Automated intake and document collection that reduces friction for loan officers.

- AI-driven financial spreading with line-item, source-cited values for every financial figure.

- Proactive risk flags and exception handling tied to policy rules.

- Automatic credit memo generation and continuous covenant monitoring.

- Customizable policies and workflows that map to an institution's credit rules.

Key Differentiator

Aloan emphasizes source-level citations for every financial figure and risk flag, so every number in a credit memo links back to an origin document. That traceability is built for examiner reviews and audit trails rather than replacing human judgment on final credit decisions.

Pros

- Speeds typical underwriting steps by combining intake, spreading, and memo drafting, which reduces repetitive task time for analysts.

- The accuracy claim above gives compliance teams a quantifiable starting point when documenting data quality in audit packets.

- Integrates as an overlay to existing loan origination systems, so IT teams do not have to migrate core LOS data to test the product.

- Built-in covenant alerts and examiner-friendly reports reduce manual reconciliation during reviews and periodic audits.

- Deployment is oriented toward institutions that want policy mapping; that approach limits disruption to existing origination workflows.

Cons

- There is a lack of publicly available independent user reviews, which makes third-party validation of long term satisfaction hard to find.

- Integration complexity will vary; some legacy LOS environments require engineering effort to connect via APIs or webhooks.

- For very bespoke or highly complex deals, the platform may need customization and policy tuning before it matches bank procedures.

When It May Not Fit

If you expect Aloan to replace your loan origination system, this is the wrong match. It functions solely as an underwriting layer and requires initial policy configuration to mirror your credit rules. Institutions without resources for mapping policies may find setup burdensome.

Notable Integrations

Aloan exposes REST APIs and supports webhooks for LOS integration, enabling automated handoffs and event-driven updates without prescriptive connector lists.

Who It's For

Community banks, regional banks, credit unions, CDFIs, and non-bank commercial lenders that need faster, regulator-friendly underwriting support and prefer an overlay model to full LOS migration. Best for teams that value source traceability and examiner-ready deliverables.

Real World Use Case

According to the vendor, a regional bank deployed Aloan to automate commercial loan underwriting and reduced turnaround from several weeks to under 30 minutes while keeping full source documentation for audits. That reported outcome illustrates the platform's focus on speed plus traceability.

Pricing

The product listing is informational only and does not publish standard pricing. Institutions should contact Aloan for licensing, implementation, and ongoing support cost estimates tied to deal volume and customization needs.

Website: https://aloan.ai

Comparative Analysis: Loan Risk Management Software Options

Choosing the right loan risk management software depends on your organization’s size, priorities, and operational complexities. Four standout options—RiskinMind, Oscilar, LenderBox, and Aloan—each cater to different needs within the financial services landscape.

Usability and Implementation

RiskinMind simplifies workflows by integrating credit memo creation, regulatory monitoring, and CECL modeling into one platform, which minimizes manual interventions commonly experienced in other tools. Meanwhile, Oscilar's no-code interface enables rapid configuration of workflows but requires significant upfront effort to adapt the platform to specific use cases. LenderBox focuses on parameterized automation, allowing CRE-focused institutions to create committee-ready reports efficiently. Lastly, Aloan also streamlines integration with existing systems for mid-market adopters but may require bespoke configurations to manage specific policy mappings effectively.

AI Customization and Scalability

When it comes to scalability, Oscilar excels by continuously retraining its AI models using live feedback. This adaptability makes it particularly well-suited to dynamic, high-volume scenarios. Conversely, RiskinMind reduces complexity by hosting internally controlled models more appropriate for mid-range banks prioritizing data sovereignty over live adaptability. LenderBox's application of specialized AI engines ensures accuracy and speed in real estate lending, but its modularity may not resonate with organizations seeking all-encompassing capabilities.

Best Fit Scenarios

- RiskinMind is recommended for financial institutions that need a unified solution to manage credit, fraud, and regulatory operations efficiently while maintaining a high data governance standard.

- Oscilar shines for larger, adaptable operations with engineering support and evolving SOPs, benefiting from its customizable, no-code approach.

- LenderBox suits CRE-focused institutions that require precise, audit-friendly outputs and integrated market assessments.

- Aloan fits regional banks favoring low-disruption overlays and source-cited financials highly tailored for examiner reviews.

Our Pick: RiskinMind

RiskinMind’s unique offering lies in its integration of credit memo automation, fraud detection, and regulatory updates through AI technologies while maintaining in-house model control. This configuration ensures operational depth, offering utility for mid-sized institutions prioritizing cross-departmental efficiencies. While it may not cater to organizations requiring frequent policy updates on a granular level, its all-in-one approach solidifies RiskinMind as an ideal choice for streamlined risk management workflows.

Loan Risk Management Software Comparison

When selecting a loan risk management software, consider platforms offering comprehensive feature sets, streamlined workflows, and robust audit compliance tools.

| Product | Core Feature | Key Differentiator | Best For | Notable Limitation |

|---|---|---|---|---|

| RiskinMind | Credit memo creation, fraud detection, CECL | Integrated AI models with in-house controls | Small to mid-sized banks prioritizing unified workflows | Requires model tuning for specific credit policies |

| Oscilar | AI-based fraud detection and compliance | No-code platform with trainable agents | Medium to large institutions managing diverse risk needs | Steep learning curve and initial setup investment |

| LenderBox | Underwriting for commercial real estate (CRE) | Purpose-specific AI engines for CRE tasks | CRE-focused banks emphasizing compliance and accuracy | Mixed reviews on service and accuracy reporting |

| Aloan | Automated underwriting and policy mapping | Source-cited financial data for audit trails | Institutions requiring audit-friendly credit processes | Requires policy configuration to align with usage |

Discover Better Loan Risk Management with RiskinMind

Finding the right solution among the thedailyworkflow.com alternatives can be challenging when your financial institution needs faster, more accurate, and fully auditable credit risk workflows. RiskinMind addresses the core pain points highlighted in the article—from automating credit memos to integrating real-time regulatory alerts—helping credit officers and compliance teams reduce manual tasks while maintaining complete control over data and AI models.

Key benefits include:

- 99.7% risk detection accuracy with sub-second processing times

- Unified workflows combining underwriting, fraud detection, and compliance

- SOC 2 certified security for peace of mind

See how RiskinMind can transform your underwriting process and produce committee-ready reports faster. Visit RiskinMind now to explore demos and client stories. Take control of your loan risk management and automate credit memo creation in minutes.

Frequently Asked Questions

How does Riskinmind’s fraud detection feature work?

Riskinmind automatically detects fraud and anomalies at the point of analysis. This built-in feature minimizes the investigation load downstream and results in faster decision-making when alerts are valid, enhancing overall efficiency in loan risk management.

What is the difference between Riskinmind and Oscilar?

Oscilar emphasizes a no-code AI Risk Decisioning™ platform that allows users to configure workflows easily. In contrast, Riskinmind is designed for users who prioritize centralized credit workflow automation, integrating model control and regulatory monitoring within a single environment, suited for small to mid-sized banks and credit unions.

Which platform automates credit memo creation more quickly, Riskinmind or LenderBox?

Riskinmind automates credit memo generation in minutes, with an accuracy claim of 99.7%. This rapid processing time allows credit officers to focus more on review rather than transcription, making it a suitable choice for institutions looking to enhance their underwriting efficiency.

Can I use Aloan if my institution requires tight audit trails and source citations?

Aloan provides source-level citations for every financial figure, ensuring traceability essential for auditor reviews. This focus on auditability makes Aloan a strong candidate if your institution prioritizes meticulous documentation and regulatory compliance in underwriting.

How does Riskinmind support compliance with regulatory alerts?

Riskinmind offers real-time monitoring of regulatory changes, accompanied by alert features, which helps institutions stay informed and compliant without needing to stitch multiple tools together. This all-in-one capability simplifies oversight and enhances operational efficiency in loan risk management.

What should I consider when using Riskinmind for specific credit types?

While Riskinmind offers impressive automation and control, its dependence on AI models may require ongoing tuning and validation specific to your institution’s credit types. Taking this into account ensures that your use aligns effectively with local underwriting policies.