A risk assessment methodology is a structured, repeatable framework that organizations use to identify, evaluate, and prioritize risks by measuring their likelihood and potential impact on business objectives. For credit unions, community banks, and lenders, selecting the right methodology is not a theoretical exercise. It directly determines whether your institution can defend its risk decisions to regulators, allocate capital rationally, and avoid the kind of portfolio surprises that erode trust and capital buffers. This guide breaks down the core risk assessment approaches available in 2026, from qualitative judgment-based techniques to quantitative statistical models, and explains how frameworks like PMBOK and NIST AI RMF structure these methods into governance-ready processes.

What is risk assessment methodology and why does it matter?

Risk assessment methodology refers to the systematic process by which an organization identifies potential threats, analyzes their probability and consequence, and ranks them to support risk management decisions. The term encompasses a spectrum of approaches: qualitative methods that rely on expert judgment, quantitative methods that use statistical models, and semi-quantitative hybrids that combine both. Each approach produces different outputs, from narrative risk registers to numerical expected loss figures, and each serves a distinct organizational purpose.

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

The importance of risk assessment in financial institutions cannot be overstated. Regulatory bodies including the OCC, FDIC, and NCUA expect institutions to demonstrate that their risk decisions are systematic, documented, and defensible. A methodology provides that documentation trail. Without one, risk scores across business units become inconsistent, audit findings multiply, and board-level risk reporting loses credibility. The methodology is the architecture that makes risk management repeatable rather than reactive.

Financial risk scenarios that demand structured assessment include credit concentration in commercial real estate portfolios, interest rate sensitivity under stress scenarios, third-party vendor failures, and increasingly, AI model risk. Each of these requires a different analytical lens, which is precisely why understanding the full range of methodologies gives risk officers and CROs a genuine strategic advantage.

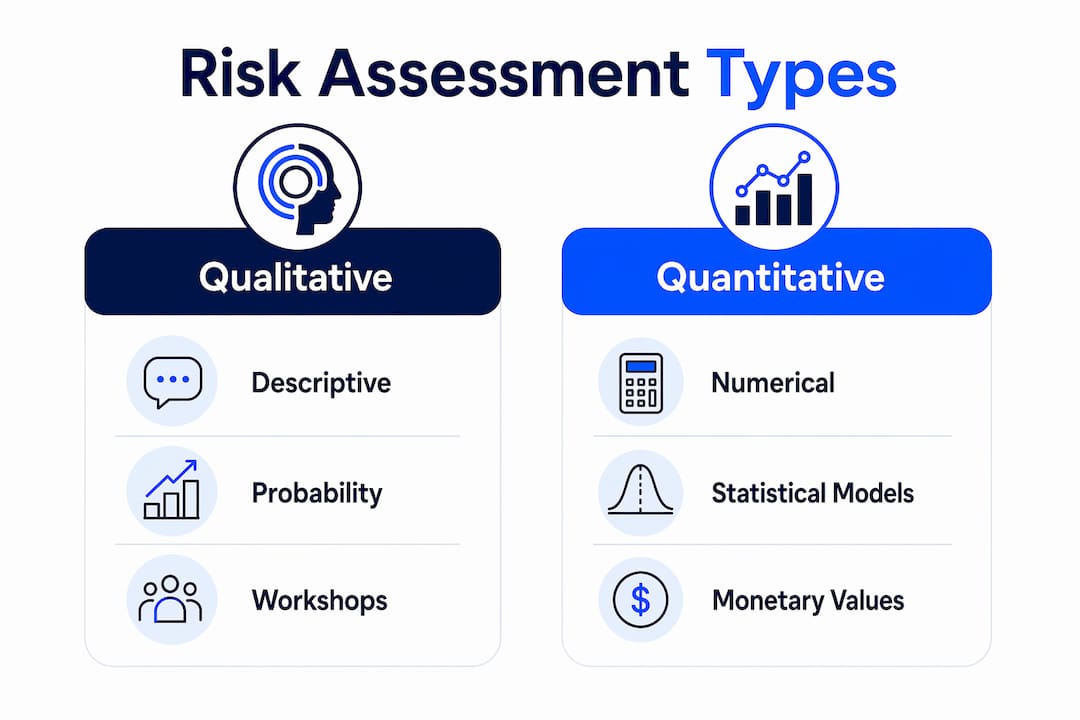

What are the main types of risk assessment methodologies?

The three primary categories of risk assessment techniques are qualitative, quantitative, and semi-quantitative. Understanding their differences in data requirements, precision, and complexity is the foundation of sound methodology selection.

Qualitative methods use descriptive scales, probability-impact matrices, and structured workshops to rank risks without numerical precision. Cross-functional team input reduces the bias that emerges when a single department rates its own risks. This matters because siloed qualitative scoring routinely underestimates cross-functional exposures. Common tools include one-dimensional rating scales (low, medium, high), two-dimensional probability-impact grids, and facilitated risk workshops with subject matter experts. These methods are fast, low-cost, and accessible to organizations without mature data infrastructure.

Quantitative methods use numerical data and statistical models, including Monte Carlo simulation and expected monetary value calculations, to produce numeric risk prioritization. This approach is used when institutions need to express risk in dollar terms, such as expected credit loss under CECL, or when comparing risk-adjusted returns across loan portfolios. The precision is real, but so is the cost. Quantitative assessments require accurate, complete data and strong data lineage standards comparable to financial model risk practices.

Semi-quantitative methods assign numerical scores to qualitative categories, for example, scoring "high probability" as a 4 on a 1-to-5 scale, then multiplying by an impact score to produce a composite risk rating. This approach offers more comparability than pure qualitative assessment while avoiding the full data burden of quantitative modeling. Many community banks use semi-quantitative scoring in their enterprise risk management programs as a practical middle ground.

| Methodology | Data requirements | Precision | Complexity | Typical application |

|---|---|---|---|---|

| Qualitative | Low (expert judgment) | Descriptive | Low to medium | Early-stage risk identification, operational risk |

| Semi-quantitative | Moderate (scored scales) | Ordinal ranking | Medium | ERM programs, compliance risk scoring |

| Quantitative | High (historical data, models) | Numeric (dollar, probability) | High | Credit risk, market risk, CECL modeling |

Pro Tip: If your institution is building its first formal risk assessment program, start qualitative to establish a risk register and governance structure, then introduce semi-quantitative scoring once you have consistent data collection across business units. Reserve full quantitative modeling for your highest-criticality risk domains where the data infrastructure already exists.

How do PMBOK and NIST AI RMF structure the risk assessment process?

Established frameworks translate methodology choices into repeatable governance processes. Two frameworks are especially relevant for financial institutions in 2026: PMBOK 8 and the NIST AI Risk Management Framework.

PMBOK 8 consolidates qualitative and quantitative risk analysis into a single iterative risk analysis process rather than treating them as sequential phases. The key structural elements include:

- Developing a risk management plan that defines scoring criteria, roles, and reporting cadence before any assessment begins.

- Identifying risks through structured interviews, checklists, and assumption analysis across all project or portfolio dimensions.

- Performing qualitative analysis using a probability-impact matrix to prioritize risks for further attention.

- Performing quantitative analysis on high-priority risks where data supports numerical modeling.

- Communicating results to stakeholders through visual matrices and risk registers that support decision-making at the board and management levels.

The PMBOK model requires risk owners and subject matter experts to validate scores, which directly addresses the consistency problem. Standardizing scoring rubrics and requiring justification for each risk rating improves comparability across business units and makes the assessment defensible under audit. Without this discipline, two loan officers rating the same credit concentration risk may produce scores that differ by two full categories.

The NIST AI Risk Management Framework structures AI risk management into four functions: Govern, Map, Measure, and Manage. The Measure function explicitly incorporates both qualitative and quantitative approaches, supported by selection of appropriate metrics and tools. For financial institutions deploying AI in underwriting or fraud detection, this framework provides a lifecycle model that embeds risk assessment within an ongoing governance and improvement cycle rather than treating it as a one-time compliance exercise. The NIST AI RMF's continuous iteration model is particularly valuable as AI systems evolve and their risk profiles shift over time.

Together, PMBOK and NIST AI RMF demonstrate that the most effective risk evaluation frameworks share three structural features: defined scoring criteria, cross-functional stakeholder involvement, and iterative reassessment tied to governance cycles.

What are practical applications and challenges in financial organizations?

Applying risk assessment methodologies in financial institutions produces specific outputs that feed directly into credit decisions, compliance reporting, and capital allocation. The most common outputs are risk registers, heat maps, and treatment plans. Risk registers and heat maps score threats and vulnerabilities by likelihood and impact, producing a visual prioritization that board members and examiners can interpret quickly.

The practical challenges are significant and often underestimated:

- Data completeness: Quantitative assessments require evidence standards comparable to financial model risk practices. Probabilities and loss distributions need strong supporting data, and many community banks lack the historical depth required for statistically valid quantitative models across all risk categories.

- Qualitative bias: Individual raters systematically over- or underestimate risks based on their functional perspective. A loan officer may downgrade credit concentration risk in a sector where they have strong relationships. Larger, cross-departmental teams reduce this bias by introducing multiple perspectives into the scoring process.

- Matrix misuse: Risk matrix scores are frequently treated as objective truth rather than as decision inputs. Risk matrix outputs should be cross-validated with confidence levels, existing controls, and qualitative context to avoid misleading management decisions. A risk rated "medium" on a matrix may still be a board-level concern if existing controls are weak or untested.

- Cross-unit inconsistency: Without standardized scoring criteria, different business units rate identical risks differently, making portfolio-level aggregation meaningless.

Best practices that address these challenges include forming cross-functional assessment teams that include credit, compliance, operations, and technology representatives; requiring written justification for every risk score above a defined threshold; and linking risk assessment outputs directly to the institution's compliance reporting calendar so that assessments remain current rather than becoming annual snapshots that age poorly.

Pro Tip: Never present a risk matrix score to your board without also disclosing the confidence level behind it and the status of existing controls. A heat map without that context is a false precision instrument that can produce worse decisions than no matrix at all.

How to choose the right risk assessment methodology

Selecting a methodology requires honest evaluation of four organizational variables: risk maturity, data infrastructure, regulatory requirements, and the criticality of the risk domain being assessed.

- Assess your data infrastructure first. If your institution cannot produce clean, consistent historical loss data for a given risk category, a quantitative model will produce unreliable outputs. Start with qualitative or semi-quantitative methods and build data collection discipline in parallel.

- Match methodology rigor to risk criticality. Credit risk in a concentrated CRE portfolio warrants quantitative modeling. Operational risk in a back-office process may be adequately addressed by a well-facilitated qualitative workshop. Not every risk domain requires the same level of analytical investment.

- Consider regulatory expectations. Institutions subject to CECL, BSA/AML, or model risk management guidance (SR 11-7) face specific documentation and validation requirements that favor semi-quantitative or quantitative approaches with auditable outputs.

- Plan for evolution. Most institutions benefit from a step-by-step risk assessment approach that begins qualitatively and introduces quantitative rigor as data maturity improves. A hybrid methodology that uses qualitative scoring for emerging risks and quantitative modeling for established risk categories is both practical and defensible.

| Selection criterion | Recommended methodology |

|---|---|

| Limited data, early-stage program | Qualitative |

| Moderate data, ERM program in place | Semi-quantitative |

| Rich historical data, model risk governance | Quantitative |

| AI or technology risk with lifecycle exposure | NIST AI RMF with mixed methods |

| Regulatory audit or compliance reporting | Semi-quantitative with documented justification |

My honest assessment of where risk methodology is heading

The conversation about risk assessment methodology in financial services has shifted considerably over the past several years, and not always in the direction practitioners expect. The dominant trend is toward quantitative precision, driven by AI tooling, better data pipelines, and regulatory pressure for numeric defensibility. That trend is largely correct. But the institutions I see struggling most are not the ones that lack quantitative models. They are the ones that adopted quantitative outputs without maintaining the qualitative governance layer underneath.

A Monte Carlo simulation is only as credible as the assumptions feeding it. When those assumptions are set by a single analyst without cross-functional review, the quantitative output carries the same bias risk as a poorly facilitated qualitative workshop. The NIST AI RMF's emphasis on continuous evidence collection and iterative reassessment reflects a mature understanding of this problem. Risk assessment is not a model you run once. It is a governance discipline you maintain continuously.

For CROs and risk officers at community banks and credit unions, the practical implication is this: invest in your qualitative infrastructure before you invest in quantitative models. Build cross-functional scoring teams, standardize your rubrics, and require written justification for every material risk rating. That foundation makes every quantitative layer you add later more credible, more auditable, and more useful to the people making decisions with it. The AI risk management practices that produce the best outcomes combine algorithmic precision with human governance, not one at the expense of the other.

— Raj

How Riskinmind automates risk assessment for financial institutions

Riskinmind's AI-powered platform translates the methodologies described in this article into automated, real-time risk workflows purpose-built for credit unions, community banks, and lenders. The CRE Loan Risk Predictor applies quantitative risk analysis to commercial real estate portfolios, producing defensible risk scores in under half a second without manual model runs. The Loan Application AI tool automates borrower risk evaluation using the same structured probability-impact logic that underpins sound semi-quantitative methodology. For institutions seeking portfolio-level context, the peer benchmarking solution provides comparative risk analytics that situate your institution's risk profile against relevant peers. Each tool is SOC 2® certified and designed to meet the documentation and auditability standards that examiners expect.

FAQ

What is a risk assessment methodology in simple terms?

A risk assessment methodology is a structured process for identifying, analyzing, and prioritizing risks based on their likelihood and potential impact. It provides the rules and tools an organization uses to make risk decisions consistently and defensibly.

What are the three main types of risk assessment?

The three main types are qualitative, quantitative, and semi-quantitative. Qualitative methods use descriptive scales and expert judgment; quantitative methods use statistical models and numerical data; semi-quantitative methods assign scores to qualitative categories to produce comparable rankings.

How does PMBOK structure the risk assessment process?

PMBOK 8 combines qualitative and quantitative risk analysis into an iterative process that uses probability-impact matrices for prioritization and requires risk owner validation at each stage to produce auditable, stakeholder-ready outputs.

When should a financial institution use quantitative risk assessment?

Quantitative risk assessment is appropriate when an institution has sufficient historical data, established data governance, and a specific need to express risk in numeric terms, such as expected credit loss modeling under CECL or market risk stress testing.

What is the biggest mistake organizations make with risk matrices?

The most common error is treating risk matrix scores as objective conclusions rather than decision inputs. Risk matrix outputs must be cross-validated with confidence levels and existing control effectiveness to avoid misleading board and management decisions.

Key takeaways

A risk assessment methodology is only as effective as the governance structure, data quality, and cross-functional discipline supporting it.

| Point | Details |

|---|---|

| Methodology selection drives outcomes | Match qualitative, semi-quantitative, or quantitative methods to your data maturity and risk criticality. |

| Frameworks provide governance structure | PMBOK 8 and NIST AI RMF embed risk assessment into iterative, auditable governance cycles. |

| Bias is a qualitative risk | Cross-functional teams and standardized scoring rubrics are the primary defenses against inconsistent ratings. |

| Quantitative precision requires data governance | Statistical models need evidence standards equivalent to financial model risk practices to produce defensible outputs. |

| Evolution beats perfection | Start qualitative, build data discipline, and introduce quantitative rigor incrementally as infrastructure matures. |