The cost of overlooking a single risk signal can be catastrophic. Recent bank failures in 2026 have reinforced a hard truth: institutions that rely on fragmented oversight and static checklists are the most vulnerable when market conditions shift. For risk management professionals at credit unions, community banks, and lenders, the answer is not just more data but a structured, repeatable analytics process powered by AI. This guide walks you through that process step by step, from building your risk taxonomy to continuous monitoring, so you can strengthen oversight, satisfy regulators, and protect your portfolio before problems escalate.

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

Table of Contents

- What you need: Tools, frameworks, and requirements

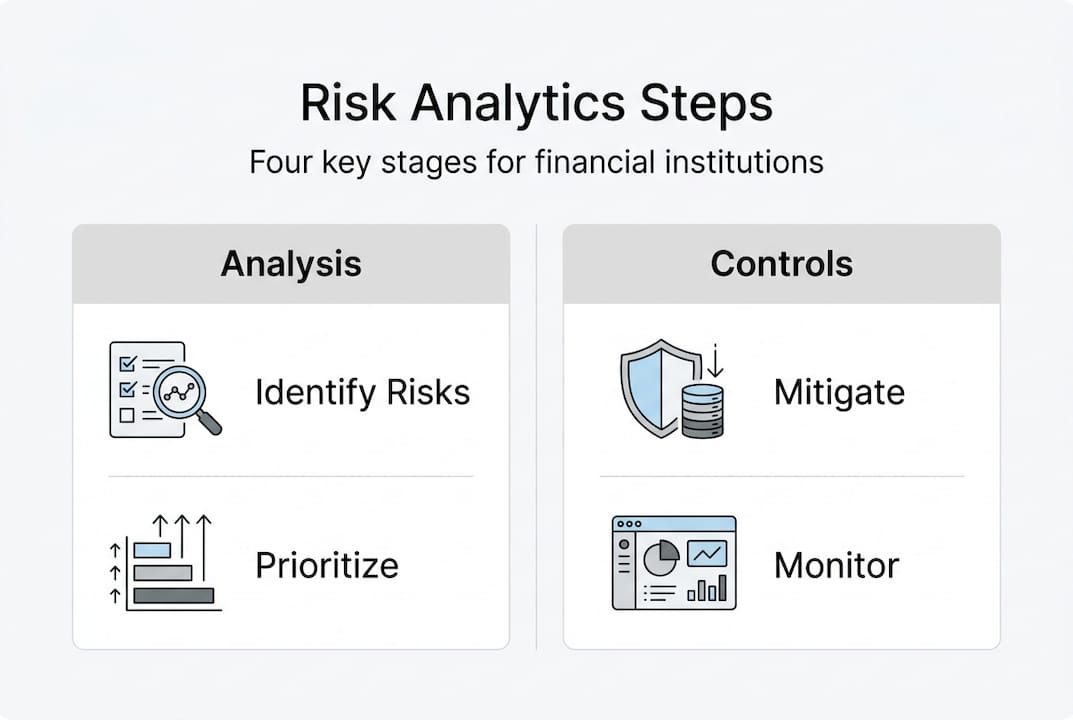

- Step 1: Identify and classify key risks

- Step 2: Assess, analyze, and prioritize risks

- Step 3: Develop mitigation strategies and embed controls

- Step 4: Monitor, review, and report risks continuously

- What most experts miss about step-by-step risk analytics

- Supercharge your risk analytics with RiskInMind's AI solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Comprehensive risk mapping | Start with a well-defined taxonomy that integrates both traditional and AI-driven risks. |

| Quantitative assessment first | Use scoring models and stress tests to prioritize risks before taking action. |

| Mitigation plus monitoring | Pair mitigation strategies with ongoing monitoring using AI tools and board oversight. |

| Human oversight critical | Never rely on AI alone—embed human review and governance at each step. |

What you need: Tools, frameworks, and requirements

Now that you know why proactive risk analytics is business-critical, let's look at the core tools and frameworks you'll need to operate effectively. Two pillars anchor any serious risk analytics program: Basel III and ISO 31000, which establish capital adequacy, liquidity standards, and a universal risk management vocabulary. Layered on top of these, the NIST AI Risk Management Framework and EBA benchmarks provide the guardrails specifically needed when AI-powered tools enter your analytics stack.

| Framework | What it adds | Core tools |

|---|---|---|

| Basel III | Capital and liquidity minimums | LCR, NSFR, stress testing |

| ISO 31000 | Universal risk process structure | Risk registers, heat maps |

| NIST AI RMF | AI governance and accountability | Model cards, bias audits |

| EBA Methodological Guide | Supervisory benchmarks for EU/global banks | Asset quality ratios, solvency indicators |

Beyond frameworks, your quantitative toolkit should include probability-impact matrices, value-at-risk models, scenario analysis engines, and machine learning-based anomaly detectors. These tools let you move from gut-feel assessments to evidence-based decisions, which is exactly what regulators expect when reviewing your risk assessment models.

The five main financial risk categories you must cover are:

- Market risk: Exposure to interest rate shifts, equity price changes, and foreign exchange volatility

- Credit risk: Probability of borrower default across your loan portfolio

- Liquidity risk: Ability to meet short-term obligations without fire-sale asset disposals

- Operational risk: Losses from process failures, fraud, cyber incidents, and operational risk management with AI

- Solvency risk: Long-term capital adequacy relative to total risk exposure

Aligning your institution to risk governance standards from the outset prevents costly retrofits later.

Pro Tip: Before building anything new, run a current-state inventory of your existing risks using a structured taxonomy like the ORX Reference Taxonomy for operational risk. This baseline reveals gaps and prevents duplication across business lines.

Step 1: Identify and classify key risks

With tools and frameworks ready, the first actionable step is building your institution's risk map. Risk analytics starts by identifying market, credit, liquidity, and operational exposures, then mapping each one to specific business lines, products, and geographies. This mapping exercise transforms a vague sense of exposure into a structured inventory that every stakeholder, from the board to the front line, can act on.

When integrating AI tools into your identification process, SR 11-7 model risk guidance becomes essential. Key requirements include:

- Documenting the purpose, assumptions, and limitations of every model before deployment

- Conducting independent validation separate from the model development team

- Establishing ongoing performance monitoring with defined thresholds for escalation

- Maintaining version control and an audit trail for all model changes

- Ensuring explainability so examiners can understand how outputs are generated

For a practical look at how risk analytics methodologies apply in real institutional settings, community bank and credit union case studies offer compelling evidence of what early detection can prevent. Reviewing examples of institutional risks across asset classes also sharpens your classification criteria.

Pro Tip: At this stage, document AI-specific risks alongside classic financial risks. Model drift, training data bias, and adversarial input vulnerabilities belong in your risk register just as much as interest rate exposure does. Treating them as afterthoughts creates blind spots that examiners will find before you do.

Step 2: Assess, analyze, and prioritize risks

Once risks are cataloged, it's time to measure and rank them so you can focus where it matters most. Common tools include probability-impact matrices, scoring models, and stress tests, each of which assigns a quantitative weight to the likelihood and severity of each identified risk. AI-driven approaches extend this by processing thousands of data points in real time, surfacing non-linear relationships that traditional models miss.

| Dimension | Traditional approach | AI-driven approach |

|---|---|---|

| Data volume | Periodic batch samples | Real-time continuous feeds |

| Pattern detection | Linear regression, rule sets | Neural networks, anomaly detection |

| Speed | Days to weeks | Sub-second response |

| Explainability | High (formula-based) | Requires additional XAI layer |

| Regulatory alignment | Well-established | Evolving, requires documentation |

A structured quantitative assessment follows these steps:

- Score each risk on a 1-5 probability scale and a 1-5 impact scale

- Multiply scores to generate a risk priority number for ranking

- Apply expected loss models to credit exposures using CECL-compliant methodologies

- Run scenario-based stress tests against EBA indicators such as LCR, NSFR, asset quality ratios, and solvency buffers

- Benchmark your outputs against peer institutions using publicly available supervisory data

For institutions already using machine learning, AI-powered risk intelligence platforms can automate steps 1 through 4, dramatically reducing the time from data ingestion to actionable priority rankings.

Pro Tip: Before finalizing your risk priority list, run an explainability check on every AI model output. If your team cannot articulate why a specific loan or counterparty ranked as high-risk, regulators will not accept it either. Explainability is not optional; it is a regulatory expectation.

Step 3: Develop mitigation strategies and embed controls

With rankings in place, the logical next step is translating priorities into actionable mitigation strategies. Effective mitigation goes well beyond policy updates. Risk mitigation includes contingency plans, AI-specific controls for adversarial attacks, and governance structures that address black-box model risks. For financial institutions deploying agentic AI, the stakes are especially high because automated decisions can cascade faster than any human review cycle.

Core mitigation controls to implement include:

- KRI dashboards: Real-time key risk indicator tracking tied to pre-approved escalation thresholds

- AI model validation: Scheduled independent reviews of every model in production, including edge case testing

- Contingency drills: Tabletop exercises simulating liquidity stress, cyber incidents, and model failures

- Policy guardrails: Documented limits on AI decision authority, particularly for high-value loan approvals

Building and reviewing mitigations follows a clear sequence:

- Assign a risk owner for each high-priority exposure

- Draft a mitigation plan with specific controls, timelines, and success metrics

- Review the plan against AI risk management best practices and regulatory guidance

- Obtain board or senior management sign-off before implementation

- Schedule a formal review cycle, at minimum quarterly, to assess control effectiveness

For risk intelligence strategies that integrate human oversight with AI automation, the guiding principle is straightforward:

High-impact decisions driven by AI must always include a human checkpoint. Automation accelerates analysis, but accountability cannot be delegated to an algorithm.

Step 4: Monitor, review, and report risks continuously

With mitigations in place, success depends on ongoing monitoring, adaptation, and transparent reporting. Static risk assessments decay quickly in dynamic markets, and a control that worked last quarter may be inadequate today. Continuous monitoring with dashboards, periodic reviews, and board reporting is what separates institutions that catch emerging risks early from those that discover them in an examiner's report.

Your monitoring infrastructure should include:

- Real-time KRI dashboards that alert risk officers when thresholds are breached, not after the fact

- Board-level reporting packages delivered on a monthly or quarterly cadence with clear trend analysis

- Periodic internal audits that independently verify whether controls are operating as designed

- Regulatory reporting automation that maps your risk data directly to supervisory templates, reducing manual error

- Emerging risk horizon scanning using AI to flag new threat patterns before they reach material exposure levels

For context on how AI-driven risk governance can prevent catastrophic oversight gaps, the lessons from recent institutional failures are instructive. Robust risk monitoring strategies across asset classes also illustrate how dynamic surveillance outperforms periodic snapshots.

Pro Tip: Schedule quarterly stress tests specifically for your AI models, not just your loan portfolio. Model drift and data distribution shifts are silent risks that compound over time. A model performing well in 2025 market conditions may produce materially different outputs in a 2026 rate environment without triggering any obvious alert.

What most experts miss about step-by-step risk analytics

All the steps above help you build a robust process, yet most institutions still miss key ingredients. The most common failure is treating risk analytics as a project with a finish line rather than a continuous operating discipline. Frameworks get implemented, checklists get completed, and then the process quietly stagnates while the risk environment keeps moving.

AI tools amplify this problem when they are deployed without ongoing governance. AI risks should be woven into traditional risk frameworks, monitored dynamically, and never left on autopilot. A model that was validated 18 months ago and has not been reviewed since is not a risk management asset; it is a liability waiting to surface.

The institutions that perform best on regulatory examinations share three characteristics: their risk frameworks evolve with the threat landscape, their technology and human oversight are genuinely integrated rather than siloed, and their boards are actively engaged rather than passively informed. Embedding dynamic risk analytics strategies into your governance culture is what separates resilient institutions from reactive ones.

Supercharge your risk analytics with RiskInMind's AI solutions

If you're ready to implement these best practices with minimal friction, here's how RiskInMind can help. The step-by-step process outlined above can be accelerated significantly with purpose-built AI tools designed for financial institutions.

RiskInMind risk solutions bring together specialized AI agents that cover the full risk lifecycle. The Erina regulatory risk agent continuously monitors your compliance posture against evolving regulatory requirements, flagging gaps before examiners do. The CRE Loan Risk Predictor delivers real-time portfolio health scoring for commercial real estate exposures, giving your team the forward-looking visibility that manual reviews simply cannot match. Both tools operate with SOC 2 certified security and sub-second response times. Contact RiskInMind today to schedule a tailored demo and see how AI-powered risk analytics fits your institution's specific needs.

Frequently asked questions

What are the five main risk categories financial institutions must address?

The five core categories are market, credit, liquidity, operational, and solvency risk, each requiring distinct measurement tools and mitigation controls.

How does AI improve risk analytics in banks?

AI amplifies risk identification by processing real-time data streams to predict future exposures and enable continuous monitoring that periodic manual reviews cannot replicate.

What is SR 11-7 and why is it important for AI models in finance?

SR 11-7 is model risk management guidance that governs AI model validation requirements, ensuring that every model in production is independently reviewed, documented, and explainable to regulators.

How often should risk analytics be updated?

Continuous monitoring and periodic updates are the standard, with formal reviews conducted at least quarterly and immediate reassessments triggered by significant market or regulatory changes.

Recommended

- Stopping the Next 1st Choice: How RiskinMind.ai Helps Credit Unions Catch Trouble Before Failure | RiskInMind

- Blog - RiskInMind | Financial Insights & News

- Before Regulators Step In: Stopping Yonkers‑Style Failures with RiskInMind | RiskInMind

- Transforming Credit Union Growth with AI-Powered Risk Intelligence | RiskInMind

- How to secure corporate banking: a step-by-step guide