Regulatory technology, commonly called RegTech, is defined as the application of AI, machine learning, and cloud computing to automate regulatory compliance and risk management inside financial institutions. RegTech is not a consumer product. It is an enterprise compliance tool serving legal, risk, and audit functions within banks, credit unions, and lenders. Compliance headcount growth has peaked across the industry, forcing institutions to rely on tech-enabled automation to meet rising regulatory demands. Frameworks like the EU's Digital Operational Resilience Act (DORA), the AI Act, and NIS2 have accelerated RegTech adoption, with global RegTech investments exceeding tens of billions annually by early 2026. For compliance officers, CROs, and operational leads, understanding what is regulatory technology is no longer optional. It is a prerequisite for managing modern financial risk.

What is regulatory technology and what does it actually do?

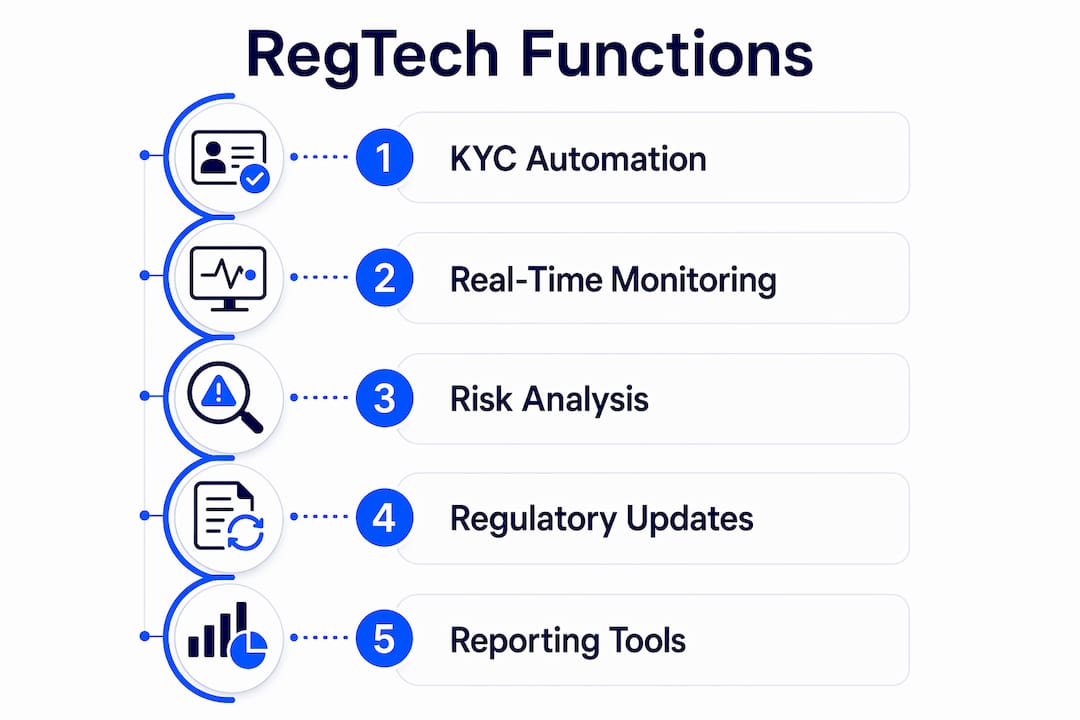

RegTech covers a defined set of compliance functions that financial institutions previously handled through manual labor. The core categories include automated Know Your Customer (KYC) verification, Anti-Money Laundering and Counter-Financing of Terrorism (AML/CFT) transaction monitoring, sanctions screening, and regulatory reporting automation. Each of these functions carries significant regulatory weight. Errors in any one of them can trigger enforcement actions, fines, or reputational damage.

Real-time monitoring is the feature that separates modern RegTech from legacy compliance software. Traditional systems ran batch checks overnight. RegTech platforms process transactions and flag anomalies as they occur, generating immutable audit trails that regulators can examine at any time. Regulatory horizon scanning adds another layer: platforms continuously ingest updates from regulatory bodies and automatically adjust compliance workflows when rules change. This prevents the compliance gaps that occur when teams miss a regulatory update buried in a 200-page consultation paper.

| RegTech Category | Core Function | Key Benefit |

|---|---|---|

| KYC Automation | Identity verification and customer due diligence | Faster onboarding, lower cost per customer |

| AML/CFT Monitoring | Real-time transaction surveillance | Reduced false positives, faster alert investigation |

| Sanctions Screening | Cross-referencing against global watchlists | Continuous coverage across 320+ data sources |

| Regulatory Reporting | Automated data aggregation and submission | Accurate, timely filings with full audit trail |

| Horizon Scanning | Tracking regulatory changes in real time | Proactive compliance updates before deadlines |

How does regulatory technology work under the hood?

The technical foundation of RegTech rests on three pillars: AI and machine learning, cloud computing, and structured data pipelines. AI models identify patterns in transaction data that human analysts would miss. Machine learning algorithms improve detection accuracy over time by learning from confirmed cases of fraud, money laundering, or policy violations. Cloud computing provides the processing power and storage capacity to run these models at the scale financial institutions require.

Data hygiene is the factor most institutions underestimate. Clean, structured internal data is the prerequisite for any AI-driven compliance tool to produce reliable outputs. If customer records are fragmented across legacy systems, or transaction data lacks consistent formatting, the AI model will generate unreliable results regardless of its sophistication. Institutions that invest in data preparation before deploying RegTech see significantly better outcomes than those that treat it as an afterthought.

Automation workflows replace manual compliance steps with rule-based and AI-driven processes. A compliance analyst who previously spent hours reviewing KYC documents now reviews only the flagged exceptions. The platform handles the routine verification. This shift does not eliminate compliance roles. It redirects human judgment toward higher-value decisions.

Key technical components driving RegTech effectiveness:

- Large language models (LLMs): Extract and interpret regulatory text from dense legal documents, translating requirements into workflow rules.

- Neural networks: Power transaction monitoring models that detect anomalous behavior with greater accuracy than rules-based systems alone.

- API integrations: Connect RegTech platforms to core banking systems, data vendors, and regulatory portals without requiring full system replacement.

- Cloud-native architecture: Enables real-time processing and rapid deployment of regulatory updates across the entire platform.

Pro Tip: When evaluating RegTech vendors, ask specifically how they push regulatory updates to your workflows. Vendors who require manual configuration updates after each regulatory change introduce the same compliance lag you are trying to eliminate.

What are the benefits of regulatory technology for financial institutions?

The primary benefit of RegTech is cost reduction at scale. Manual compliance costs are significantly higher per unit than automation-first models. The investment case for RegTech is built on reducing the cost per customer onboarded, the cost per alert investigated, and the cost per regulatory report filed. As transaction volumes grow, manual processes scale linearly with headcount. RegTech scales with compute, which is far cheaper.

Modern RegTech platforms employing generative AI can reduce compliance workloads by up to 80%, particularly in document validation and regulatory reporting. That figure represents a structural shift in how compliance functions are staffed and resourced. Institutions that achieve this level of automation redirect compliance staff toward exception management, regulatory strategy, and examiner relationships.

The benefits extend beyond cost:

- Auditability by design: RegTech systems generate tamper-proof, timestamped logs of every compliance decision. Regulators can examine not just what the system decided, but why. This is critical for AI-driven decisions that must be explainable under frameworks like the EU AI Act.

- Regulatory transparency: Automated reporting reduces the risk of human error in filings and creates a consistent record that survives staff turnover.

- Scalability: A RegTech platform handling 10,000 transactions per day can handle 10 million with infrastructure adjustments, not headcount additions.

- Accuracy: Machine learning models applied to AI-driven compliance reduce false positive rates in AML monitoring, freeing analysts from reviewing alerts that were never genuine risks.

The institutions gaining the most from RegTech are those that treat it as an operational infrastructure investment, not a point solution for a single compliance problem.

What regulatory drivers are accelerating RegTech adoption?

Three regulatory frameworks are reshaping compliance demands for financial institutions in 2026. DORA, the EU's Digital Operational Resilience Act, requires financial entities to demonstrate operational resilience across their entire technology supply chain, including third-party vendors. The EU AI Act introduces transparency and explainability requirements for AI systems used in high-risk decisions, which includes credit and compliance applications. NIS2 expands cybersecurity obligations across financial infrastructure. Together, these frameworks create compliance obligations that manual processes cannot satisfy at the required speed or documentation depth.

RegTech is distinct from two adjacent categories that compliance leaders often conflate. SupTech (supervisory technology) is used by regulators themselves to monitor the institutions they oversee. FinTech focuses on consumer-facing financial products and services. RegTech sits between them: it is the technology that regulated institutions use to meet the demands that SupTech-equipped regulators impose. Understanding this distinction matters when allocating budget and selecting vendors.

Regulatory complexity compounds annually. Each new framework adds reporting obligations, documentation requirements, and audit expectations. Institutions that rely on manual processes face a widening gap between what regulators expect and what their compliance teams can deliver. Regulatory complexity and enforcement pressure are the primary forces driving rapid RegTech adoption across community banks, credit unions, and larger financial institutions alike.

Pro Tip: Assign one compliance team member to monitor regulatory horizon changes on a monthly cadence. Pair this with a RegTech platform that embeds real-time regulatory updates directly into your workflows. The combination closes the gap between regulatory publication and operational response.

How to implement RegTech effectively in your institution

The most common implementation failure is deploying RegTech on top of dirty data. Legacy IT systems create integration challenges that require upfront data preparation before any AI tool can function reliably. Institutions that skip this step find that their RegTech platform produces unreliable outputs, which erodes trust in the system and often leads to abandonment. A data audit before vendor selection is not optional. It is the foundation of a successful deployment.

Vendor selection criteria matter as much as the technology itself. The right vendor provides real-time regulatory horizon scanning, not quarterly update packages. They offer API-based integration with your core banking system, not a rip-and-replace approach. They maintain SOC 2 certification and can demonstrate their security posture to your IT and audit teams. Vendors who cannot answer detailed questions about their update cadence and integration architecture introduce operational risk into your compliance program.

Common pitfalls to avoid during RegTech implementation:

- Skipping the data hygiene phase: Deploying AI tools on fragmented or inconsistent data produces unreliable compliance outputs.

- Selecting vendors without horizon scanning: Platforms that do not embed real-time regulatory updates require manual reconfiguration after every rule change.

- Ignoring auditability requirements: Systems that complete compliance tasks without logging decision rationale will fail regulatory examination.

- Underestimating integration complexity: API connections to core banking systems require dedicated technical resources and testing time.

- Treating RegTech as a one-time deployment: Continuous vendor management and periodic compliance reviews are necessary to maintain effectiveness.

A risk technology integration checklist helps institutions sequence these steps correctly and avoid the gaps that create compliance exposure during transition periods.

Key Takeaways

RegTech is the most direct path financial institutions have to meet rising regulatory demands without proportional increases in compliance headcount.

| Point | Details |

|---|---|

| RegTech is an enterprise tool | It serves legal, risk, and compliance functions inside financial firms, not consumer-facing products. |

| Data hygiene is the foundation | AI-driven compliance outputs are only as reliable as the structured data feeding the system. |

| Auditability by design is non-negotiable | Tamper-proof decision logs are required to satisfy regulatory examiners and AI Act transparency rules. |

| Workload reduction reaches up to 80% | Generative AI applied to document validation and reporting delivers the largest efficiency gains. |

| Vendor agility determines long-term value | Platforms with real-time regulatory horizon scanning prevent compliance gaps as rules evolve. |

RegTech is moving faster than most compliance teams realize

I have spent years watching financial institutions treat compliance technology as a back-office procurement decision. That framing is now a liability. The institutions I see falling behind are not the ones with smaller budgets. They are the ones where compliance leaders are not in the room when technology decisions get made.

The shift that surprises most CROs is how quickly RegTech changes the nature of compliance work itself. The question stops being "do we have enough people to handle this?" and becomes "do we have the right data architecture to support automation?" That is a fundamentally different problem, and it requires a different kind of leadership response.

What I find most underappreciated is the auditability dimension. Institutions focus on whether a RegTech platform can complete a task. Regulators care about whether the platform can explain why it made a decision. Those are not the same requirement. Platforms that automate without logging decision rationale create a new category of examination risk. The automation in financial compliance conversation needs to include explainability from the first vendor meeting, not as a feature request after deployment.

My strongest advice for compliance leaders evaluating RegTech in 2026: prioritize vendors who treat regulatory horizon scanning as a core product feature, not an add-on. The regulatory environment is not stabilizing. DORA, the AI Act, and NIS2 are the current wave. The next wave is already in consultation. The institutions that build their compliance infrastructure around real-time regulatory intelligence will absorb those changes without crisis. The ones that do not will spend the next three years in reactive mode.

— Raj

How Riskinmind supports financial institutions with AI-powered compliance

Financial institutions that need to close the gap between regulatory expectations and operational capacity have a direct path forward with Riskinmind.

Riskinmind's AI-powered platform is built specifically for credit unions, community banks, and lenders. It automates core compliance and risk processes, including regulatory reporting, credit risk assessment, and portfolio monitoring, with response times under half a second. The platform's AI agents, coordinated by a central director named Ava, cover regulatory compliance, credit risk, and market analysis simultaneously. SOC 2 certification and bank-grade security address the auditability and data protection requirements that regulators now demand. Explore Riskinmind's AI risk management platform to see how these capabilities apply to your institution's compliance program.

FAQ

What is regulatory technology in simple terms?

Regulatory technology, or RegTech, is the use of AI, machine learning, and cloud computing to automate compliance tasks inside financial institutions. It replaces manual processes like KYC verification, AML monitoring, and regulatory reporting with automated, auditable systems.

How does regulatory technology differ from FinTech?

FinTech focuses on consumer-facing financial products and services. RegTech is an enterprise tool used by financial institutions to meet compliance obligations imposed by regulators, not to serve end customers directly.

What are the main benefits of regulatory technology?

The primary benefits include cost reduction per compliance unit, workload reduction of up to 80% through AI automation, real-time audit trails, and the ability to scale compliance operations without proportional headcount increases.

What regulations are driving RegTech adoption in 2026?

DORA, the EU AI Act, and NIS2 are the three frameworks creating the most significant compliance demands. Each requires documentation depth, operational resilience, and AI explainability that manual compliance processes cannot deliver at scale.

What is the biggest risk in implementing RegTech?

The biggest implementation risk is deploying AI-driven compliance tools on top of unstructured or fragmented legacy data. Poor data hygiene produces unreliable outputs and erodes institutional confidence in the platform, often leading to underutilization or abandonment.