Predictive modeling in finance is defined as the use of statistical methods and machine learning algorithms to forecast future financial outcomes from historical and current data. The practice covers credit risk scoring, fraud detection, cash flow forecasting, and investment strategy. Algorithms such as logistic regression, decision trees, random forests, and neural networks each serve distinct forecasting roles. Finance teams that apply these models gain a measurable edge: firms using advanced predictive modeling report 10–20% revenue growth compared to those relying on manual forecasting. That gap reflects not just better predictions, but faster, more confident decisions at every level of the organization.

What is predictive modeling in finance?

Predictive modeling in finance is the formal discipline of building mathematical models that translate data patterns into probability-weighted forecasts of future financial events. The industry term most often used alongside it is predictive analytics in finance, which refers to the broader practice of applying those models to real business decisions. Both terms describe the same core activity: turning data into foresight.

Automate Regulatory Model Risk Governance

Examine models against 32 qualitative criteria and resolve risk Tiers with pre-deployment checklists per OCC 2011-12 guidelines.

The process starts with a clearly defined financial question. Will this borrower default? Will this transaction trigger fraud? What will cash flow look like in Q3? Each question shapes the type of model chosen and the data required to build it. Without a precise question, even technically sound models produce outputs that finance teams cannot act on.

The output of any predictive model is a score, probability, or forecast value. A credit risk model, for example, produces a probability of default rather than a binary yes or no. That probability then feeds into a lending decision, a pricing calculation, or a capital reserve requirement. The model informs the decision. It does not make it.

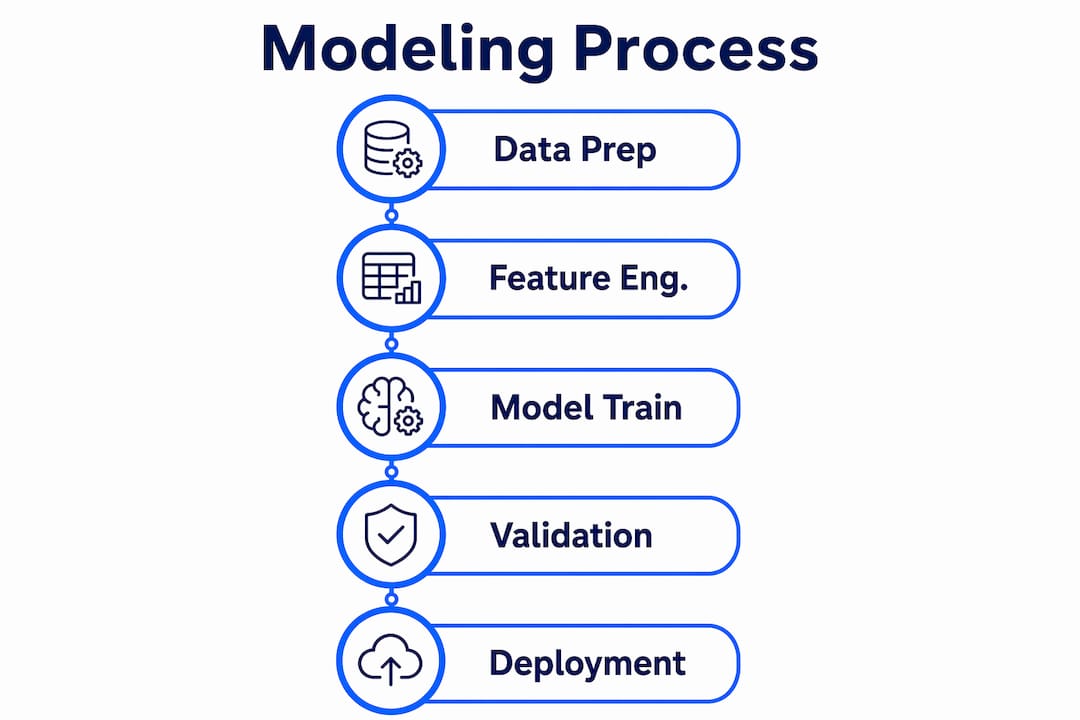

How does predictive modeling work in financial contexts?

Building a financial predictive model follows four distinct stages: data preparation, feature engineering, model training, and validation.

Stage 1: Data acquisition and preparation. Financial datasets arrive from multiple sources, including loan origination systems, market data feeds, transaction ledgers, and macroeconomic databases. Raw data contains gaps, inconsistencies, and outliers that distort model outputs. Cleaning and normalizing this data is not optional. It is the foundation everything else rests on.

Stage 2: Feature engineering. Raw variables rarely capture the financial dynamics a model needs. Feature engineering transforms raw inputs into meaningful signals: lagged variables that capture prior period behavior, volatility clusters that reflect market stress, debt-to-income ratios, and technical indicators like moving averages. Feature quality determines model accuracy far more than algorithm selection.

Stage 3: Model training. The prepared dataset trains the chosen algorithm. Classification models learn to assign borrowers to risk categories. Regression models learn to predict continuous values like revenue or loan loss reserves. Time-series models, particularly LSTM networks, learn sequential patterns in financial data over time.

Stage 4: Validation and backtesting. Validation via k-fold cross-validation and rigorous backtesting prevents overfitting and confirms that a model performs on unseen data, not just the training set. This step is frequently skipped under time pressure. Skipping it produces models that look accurate in development and fail in production.

Pro Tip: Run backtests on at least two distinct market cycles, not just the most recent period. A model trained only on low-volatility data will underperform the moment conditions shift.

After deployment, models require continuous monitoring. Market conditions, borrower behavior, and regulatory requirements all change. A model that was accurate in january may be miscalibrated by july without scheduled recalibration.

What are the benefits of predictive modeling for finance teams?

The benefits of predictive modeling are measurable in both revenue and cost terms. AI-driven predictive modeling architectures save 40–50 times operational costs compared to traditional data science teams. That is not a marginal efficiency gain. It represents a structural shift in how finance functions are resourced.

"Predictive modeling's value is best measured by incremental firm value impact rather than technical complexity." — Business LibreTexts

On the revenue side, better cash flow forecasting reduces unnecessary borrowing. A firm that forecasts a $250,000 reduction in short-term borrowing needs at an 8% rate saves $20,000 per year in interest alone. That saving justifies model investment and compounds across multiple forecasting use cases.

Predictive models also shift finance teams from reactive to proactive. Traditional finance relies on static historical data that reflects what already happened. AI-driven predictive models provide dynamic real-time updates, allowing finance teams to act fast in volatile markets. Capital budgeting, liquidity planning, and fraud prevention all improve when the underlying data is current rather than stale.

The most important nuance: model outputs only create value when integrated into financial management workflows. A fraud score sitting in a database does nothing. A fraud score embedded in a transaction approval workflow prevents losses in real time.

Which predictive modeling techniques do finance professionals use?

Common predictive models in finance include logistic regression, decision trees, random forests, neural networks, and Naïve Bayes. Each serves a different purpose depending on the financial question being answered.

| Model type | Best use case | Complexity | Key strength |

|---|---|---|---|

| Logistic regression | Credit default probability | Low | Interpretable, auditable output |

| Decision trees | Risk segmentation | Low to medium | Clear decision logic |

| Random forests | Fraud detection | Medium | Handles noisy, high-dimensional data |

| Neural networks | Market trend forecasting | High | Captures nonlinear relationships |

| LSTM networks | Time-series forecasting | High | Learns sequential financial patterns |

The table above reflects a core principle: model complexity should match the problem, not signal technical sophistication. Logistic regression remains the standard for credit scoring at regulated institutions because regulators require explainability. A neural network may outperform it on accuracy metrics but fail a model risk management review.

LSTM networks are particularly effective for financial time-series forecasting because they retain memory of prior time steps. Predicting next-quarter revenue or next-month delinquency rates requires understanding sequences, not just snapshots. LSTM architectures handle that requirement better than traditional regression approaches.

Key considerations when selecting a model:

- Regulatory explainability requirements often favor simpler models like logistic regression or decision trees.

- Random forests reduce overfitting risk compared to single decision trees by averaging across many trees.

- Neural networks require larger training datasets to avoid overfitting on limited financial history.

- Feature quality consistently outweighs algorithm choice in determining final model accuracy.

What are the practical applications of predictive modeling in finance?

The applications of predictive modeling span every major function in a financial institution. Each use case below reflects a real operational problem that models solve better than manual analysis.

-

Credit risk scoring. Logistic regression and random forest models assign probability-of-default scores to loan applicants. These scores replace or supplement manual underwriting, reducing both approval time and credit loss rates. Analysts working on predictive analytics for credit use these models to segment portfolios by risk tier and set appropriate pricing.

-

Cash flow and liquidity forecasting. Time-series models project future cash positions by learning from historical inflows, outflows, and seasonal patterns. Finance teams use these forecasts to plan short-term borrowing, manage working capital, and avoid liquidity shortfalls before they occur.

-

Fraud detection. Anomaly detection models flag transactions that deviate from established behavioral patterns. These models process thousands of transactions per second and surface suspicious activity that human reviewers would miss. The speed advantage alone justifies deployment in any institution processing high transaction volumes.

-

Portfolio risk management. Regression and simulation models estimate value-at-risk, stress-test portfolios under adverse scenarios, and identify concentration risk before it becomes a capital problem. Understanding financial risk assessment methods helps analysts apply the right model to each portfolio challenge.

-

Market trend forecasting. LSTM and other deep learning models analyze price sequences, macroeconomic indicators, and sentiment data to forecast asset price movements. Investment teams use these outputs to adjust position sizing and hedge exposure ahead of anticipated market shifts.

AI-driven dynamic models that update with real-time data represent the current frontier. Static models built on quarterly data snapshots cannot respond to intraday market moves or sudden credit deterioration. Real-time updating closes that gap and gives finance teams a genuine operational advantage.

Key Takeaways

Predictive modeling in finance delivers measurable value only when high-quality features, rigorous validation, and human judgment are combined with the right algorithm for each financial problem.

| Point | Details |

|---|---|

| Definition is precise | Predictive modeling uses statistical and ML methods to forecast financial outcomes from historical data. |

| Feature engineering drives accuracy | Lagged variables, volatility clusters, and financial ratios matter more than algorithm choice. |

| Validation prevents failure | K-fold cross-validation and backtesting across market cycles are non-negotiable before deployment. |

| Cost and revenue impact are real | AI-driven architectures save 40–50x operational costs; advanced modeling firms report 10–20% revenue gains. |

| Models support, not replace, judgment | Predictive models provide probabilities; final decisions require human expertise and business context. |

Predictive models are tools, not oracles

I have seen finance teams make two opposite mistakes with predictive models. The first is treating model output as a final answer. A credit score of 0.73 probability of default is not a decision. It is an input. The analyst still needs to weigh collateral quality, relationship history, and current market conditions before approving or declining. Models assist decisions; they do not make them.

The second mistake is dismissing models because they are not perfect. No model is. The relevant question is whether the model improves on the alternative, which is usually a slower, less consistent manual process. When you frame model value through an NPV lens, asking whether the incremental benefit exceeds implementation and maintenance costs, the answer is almost always yes for institutions processing meaningful loan or transaction volume.

The practical recommendation I give to every risk team: treat your predictive model as one voice in a structured credit committee, not as the committee chair. Build governance around it. Schedule recalibration. Document its assumptions. A model that runs unmonitored for 18 months is a liability, not an asset. The teams that get the most from machine learning in finance are the ones that treat model governance as seriously as model development.

— Raj

How Riskinmind puts predictive modeling to work

Riskinmind builds AI-powered predictive tools designed specifically for credit unions, community banks, and lenders that need production-grade risk analysis without building a data science team from scratch.

The CRE Loan Risk Predictor applies machine learning to commercial real estate loan data, scoring portfolio risk in real time with response times under half a second. The AI Credit Card Analyzer applies anomaly detection and spending pattern analysis to flag credit card risk before losses materialize. Both tools integrate with existing financial workflows and operate under SOC 2® certified security. Finance professionals who want to see these models in action can request a demo directly on the Riskinmind platform.

FAQ

What is predictive modeling in finance?

Predictive modeling in finance is the use of statistical and machine learning methods to forecast future financial outcomes, such as credit defaults, cash flows, and fraud, from historical and current data. The outputs are probability scores or forecast values that inform financial decisions.

How does predictive analytics differ from traditional financial analysis?

Traditional financial analysis relies on static historical data and manual interpretation. Predictive analytics uses algorithms that update dynamically, identify nonlinear patterns, and process far larger datasets than any manual process can handle.

What are the most common examples of predictive modeling in finance?

The most common examples include credit risk scoring, cash flow forecasting, fraud detection, portfolio stress testing, and market trend forecasting. Each application uses a different model type matched to the specific financial question.

Why does feature engineering matter more than algorithm choice?

Raw financial data rarely captures the temporal dynamics that drive outcomes. Engineered features like lagged variables, volatility clusters, and financial ratios give the model the signal it needs. A well-engineered dataset with a simple model consistently outperforms a poorly prepared dataset with a complex one.

How should finance teams validate predictive models before deployment?

Teams should use k-fold cross-validation to test model stability and rigorous backtesting across at least two distinct market cycles. Skipping validation produces models that overfit training data and underperform in live conditions.