The portfolio monitoring process is the systematic, ongoing practice of tracking, analyzing, and evaluating investment portfolios to maintain alignment with risk tolerance, compliance requirements, and investment objectives. For financial professionals at credit unions, community banks, and lending institutions, this process is not a periodic report. It is an active risk management and suitability function that must respond to both market shifts and changes in client circumstances. Standards from CIRO and frameworks like the Investment Policy Statement (IPS) define the boundaries within which effective monitoring operates. Riskinmind supports this function with AI-powered tools built specifically for institutional professionals.

What are the essential components of a portfolio monitoring process?

A well-structured portfolio monitoring process tracks both performance metrics and risk structure simultaneously. Focusing only on returns is the most common and costly mistake financial professionals make.

Performance metrics include total portfolio valuation, revenue generation, cash flow patterns, and absolute returns across time periods. Risk metrics go deeper: volatility, maximum drawdown, sector exposure, geographic concentration, and currency risk all belong in every monitoring framework. Risk-adjusted measures like the Sharpe ratio separate genuine manager skill from favorable market conditions. A portfolio generating strong absolute returns during a bull market may carry hidden concentration risk that only the Sharpe ratio and drawdown analysis will reveal.

Allocation drift is another core component. Portfolios naturally drift from their target weights as asset classes perform differently over time. Monitoring drift against the IPS target allocation is not optional. It is a suitability requirement.

- Valuation and returns: Total portfolio value, time-weighted returns, and benchmark comparisons

- Risk metrics: Volatility, maximum drawdown, Value at Risk (VaR), and beta

- Exposure monitoring: Sector, geographic, and currency concentration

- Risk-adjusted performance: Sharpe ratio, Sortino ratio, and information ratio

- Allocation drift: Deviation from IPS target weights across all asset classes

Pro Tip: Practitioners distinguish money-weighted returns from time-weighted returns to avoid misleading performance assessments influenced by cash flow timing. Use time-weighted returns for manager evaluation and money-weighted returns only when assessing client-specific outcomes.

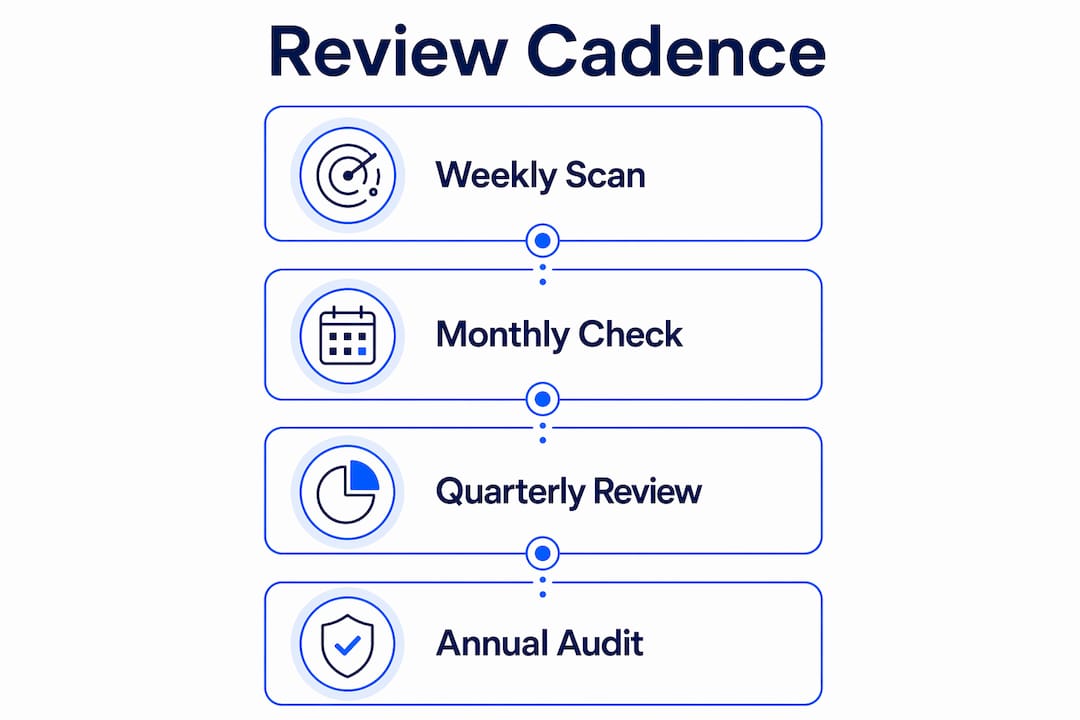

How to establish an effective portfolio review cadence

A tiered review cadence is the structural backbone of disciplined portfolio monitoring. Without defined intervals and time budgets, reviews become reactive and inconsistent.

The most effective cadence follows four tiers:

- Weekly scans (5 minutes): Check total portfolio value, flag any positions with unusual price moves, and confirm no automated alerts have been triggered. This is a quick exception check, not a full review.

- Monthly reviews (30 minutes): Analyze return trends, detect early allocation drift, and assess whether any positions have crossed concentration thresholds. Monthly reviews catch problems before they compound.

- Quarterly deep dives (60–120 minutes): Conduct a full asset allocation review, recalculate risk metrics, assess rebalancing needs, and compare performance against benchmarks. This is the primary decision-making interval for most institutional portfolios.

- Annual comprehensive evaluations (half day): Review the full portfolio against the IPS, conduct tax planning analysis, audit fees and expense ratios, and assess whether the investment mandate still reflects the client's objectives and risk profile.

This tiered monitoring cadence is the industry standard for balancing thoroughness with efficiency. Skipping the quarterly deep dive is where most compliance gaps originate.

| Review Tier | Frequency | Time Budget | Primary Focus |

|---|---|---|---|

| Quick scan | Weekly | 5 minutes | Value changes, alert triggers |

| Trend review | Monthly | 30 minutes | Drift detection, concentration checks |

| Deep dive | Quarterly | 60–120 minutes | Full risk and allocation assessment |

| Comprehensive | Annual | Half day | IPS alignment, tax, and fee audit |

Pro Tip: Set automated risk alerts for concentration thresholds and allocation drift so that exception-based monitoring supplements your scheduled reviews. Alerts catch intra-period events that a monthly review would miss.

What are best practices for managing portfolio drift and rebalancing triggers?

Portfolio drift is inevitable. The discipline lies in defining when drift requires action and when it does not.

Best practice sets rebalancing triggers when asset allocation drifts 5–10% from target weights, or when a major portfolio sleeve deviates by 5% in absolute terms. These thresholds prevent both over-trading and under-reacting. A portfolio that drifts 3% from its equity target in a volatile month does not require immediate rebalancing. A portfolio that drifts 12% does.

Tax efficiency is a critical and often overlooked dimension of rebalancing discipline. Prioritizing rebalancing activity within tax-advantaged accounts first reduces the tax drag from realizing gains in taxable accounts. Specific-lot identification, which means selecting which tax lots to sell rather than defaulting to FIFO, can materially reduce the tax impact of rebalancing trades. Tax-aware rebalancing also helps high-net-worth clients avoid triggering the Net Investment Income Tax or Medicare surcharges from large capital gain realizations.

"Rebalancing is not just a portfolio maintenance task. It is a tax event. Every rebalancing decision in a taxable account requires a cost-benefit analysis that weighs the risk reduction benefit against the after-tax cost of the trade."

Documentation of rebalancing decisions is non-negotiable for audit readiness. Every rebalancing trade requires a written rationale. The rationale must explain what threshold was breached, what action was taken, and why. Equally, when a review concludes that no rebalancing is needed, that decision also requires documentation. Regulators expect to see evidence of active suitability management, not just a record of trades.

- Set drift thresholds at 5–10% from target allocation before triggering a rebalancing review

- Rebalance within tax-advantaged accounts first to minimize taxable gain realizations

- Use specific-lot identification to control the tax basis of securities sold

- Document every rebalancing decision, including the rationale for inaction

- Avoid emotional, reactive adjustments triggered by short-term market noise

What tools and documentation practices support compliance and audit readiness?

Technology does not replace judgment in portfolio monitoring. It removes the manual friction that causes professionals to skip steps or delay reviews.

Portfolio monitoring platforms for banks and institutional managers provide real-time dashboards that display allocation drift, concentration metrics, and risk-adjusted performance in a single view. Automated alerts for concentration limits above 10% and allocation drift above 5% enforce institutional discipline without requiring manual checks. When a single position crosses 15–20% of portfolio value, the platform flags it for manual review. This exception-based approach keeps attention focused on meaningful signals rather than routine noise.

Documentation practices must align with suitability requirements and regulatory expectations. A decision-focused audit trail records not just what happened, but why. Logs should capture the date of review, the metrics examined, the thresholds checked, the conclusion reached, and the rationale for any action or inaction. This level of documentation demonstrates active suitability management during regulatory exams and satisfies the standard that monitoring decisions require documented rationale equivalent to trade records.

Integrating risk reporting with institutional compliance workflows closes the gap between monitoring and regulatory reporting. Real-time risk monitoring platforms that feed directly into compliance dashboards reduce the manual effort of preparing exam-ready documentation.

Pro Tip: Build your documentation template around the question "What did I review, what did I find, and what did I decide?" A three-sentence log entry per review period satisfies most regulatory exam standards and takes less than two minutes to complete.

Common challenges and mistakes in portfolio monitoring

The most damaging mistakes in portfolio monitoring are structural, not technical. They reflect process failures rather than analytical errors.

Short-term return metrics are often misleading noise. Professionals who focus primarily on monthly or quarterly absolute returns miss the risk structure changes that precede losses. A portfolio can show strong returns while quietly accumulating concentration risk in a single sector. Risk-adjusted metrics like the Sharpe ratio and maximum drawdown tell the real story.

Emotional, reactive decision-making is the second major failure mode. Predefined risk thresholds and automated alerts exist precisely to prevent this. When a volatility spike triggers an alert, the correct response is to review the threshold, assess whether the structural risk has changed, and document the conclusion. The incorrect response is to trade immediately based on market anxiety.

- Focusing only on returns while ignoring concentration, volatility, and drawdown metrics

- Reacting to daily market noise instead of predefined threshold breaches

- Failing to document monitoring outcomes, especially when no action is taken

- Over-monitoring, which leads to unnecessary trades and elevated transaction costs

- Treating portfolio monitoring as a backward-looking report rather than a forward-looking suitability function

Key Takeaways

A disciplined portfolio monitoring process requires tiered review cadences, predefined drift thresholds, tax-aware rebalancing, and decision-focused documentation to satisfy both risk management and regulatory suitability standards.

| Point | Details |

|---|---|

| Tiered review cadence | Use weekly scans, monthly trend checks, quarterly deep dives, and annual IPS reviews. |

| Core metrics to track | Monitor volatility, maximum drawdown, Sharpe ratio, and allocation drift alongside returns. |

| Rebalancing thresholds | Trigger reviews when allocation drifts 5–10% from targets; rebalance tax-advantaged accounts first. |

| Documentation discipline | Record every review outcome, including the rationale for inaction, to satisfy regulatory exams. |

| Automated alerts | Set concentration alerts above 10% and drift alerts above 5% to catch intra-period exceptions. |

Why most portfolio monitoring fails before the quarterly review

Portfolio monitoring fails most often not because professionals lack the right tools, but because the process is not treated as a suitability function. It gets treated as a reporting function instead.

The distinction matters. A reporting function looks backward and summarizes what happened. A suitability function looks forward and asks whether the current portfolio still matches the client's risk profile, objectives, and circumstances. CIRO's framework is explicit on this point: monitoring must respond to trigger events, including market changes, client life events, and shifts in risk tolerance, not just scheduled review dates.

What I have seen work consistently is a simple but non-negotiable rule: every review produces a written output, even if that output is a single sentence stating that no action was required. That sentence is the evidence of active management. Without it, the review might as well not have happened from a regulatory standpoint.

The tax dimension of rebalancing is where I see the most value left on the table. Professionals who treat rebalancing as a pure allocation exercise, without modeling the after-tax cost of the trades, routinely generate unnecessary tax liability for clients. Specific-lot identification and sequencing rebalancing activity through tax-advantaged accounts first are not advanced strategies. They are baseline practices that every institutional professional should apply by default.

Technology should enforce the process, not replace the judgment. Automated alerts for concentration and drift thresholds free up attention for the decisions that actually require analysis. The goal is a monitoring system where routine checks run automatically and human judgment is reserved for threshold breaches and structural changes.

— Raj

How Riskinmind supports institutional portfolio monitoring

Financial institutions that need to move beyond manual spreadsheet-based monitoring have a direct path forward with Riskinmind's AI-powered risk platform.

Riskinmind's platform delivers real-time risk dashboards, automated concentration and drift alerts, and AI-driven analysis built for credit unions, community banks, and lenders. The CRE Loan Risk Predictor applies machine learning to commercial real estate loan portfolios, surfacing concentration risk and performance signals that manual reviews miss. The Peer Benchmarking tool lets institutions compare their portfolio risk profile against peers, adding the external context that internal monitoring alone cannot provide. Riskinmind holds SOC 2® certification and processes data with response times under half a second, meeting the security and speed standards that institutional compliance workflows require.

FAQ

What is the portfolio monitoring process?

The portfolio monitoring process is the ongoing practice of tracking portfolio performance, risk metrics, and allocation drift to maintain alignment with investment objectives and compliance requirements. It functions as an active suitability management tool, not a periodic report.

How often should a portfolio be reviewed?

Best practice uses a tiered cadence: weekly 5-minute scans, monthly 30-minute trend reviews, quarterly 60–120 minute deep dives, and annual half-day comprehensive evaluations covering tax planning and IPS alignment.

What triggers a portfolio rebalancing?

Rebalancing is triggered when asset allocation drifts 5–10% from target weights or when a major portfolio sleeve deviates by 5% in absolute terms. Automated alerts set at these thresholds enforce consistent, non-emotional rebalancing discipline.

Why does documentation matter in portfolio monitoring?

Regulators require evidence of active suitability management, which means documenting not just trades but also the rationale for maintaining a portfolio without changes. A decision to hold requires the same documented justification as a decision to rebalance.

What metrics should financial professionals prioritize?

Risk-adjusted metrics like the Sharpe ratio and maximum drawdown provide more reliable signals than absolute returns alone. Time-weighted returns are the correct measure for evaluating manager performance, while money-weighted returns reflect client-specific outcomes.