Mobile risk management is defined as the structured, continuous process of organizing, testing, and proving the security and compliance readiness of mobile applications across an enterprise environment. For financial institutions, credit unions, and community banks, this discipline carries regulatory weight that generic app security programs simply cannot address. The industry term for this practice is Mobile App Risk Management, or MARM, and it extends well beyond vulnerability scanning to cover privacy governance, AI/ML model oversight, and audit-ready evidence collection. MARM is a four-pronged framework built on clarity of production readiness, consistency to standards like OWASP MAS, efficient resource allocation by business impact, and provability for auditors. Financial institutions that lack this structure face compounding exposure across customer data, regulatory standing, and operational continuity.

What is mobile risk management and how does it work?

Mobile App Risk Management is a formalized program that maps every mobile application to a business impact tier, applies the appropriate testing regimen, and generates continuous evidence that satisfies both internal audit and external regulatory review. The distinction from ad hoc security testing is significant. A MARM program defines what "production ready" means for each app category before a single line of code ships, which removes ambiguity from release decisions and gives risk officers a defensible position during examinations.

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

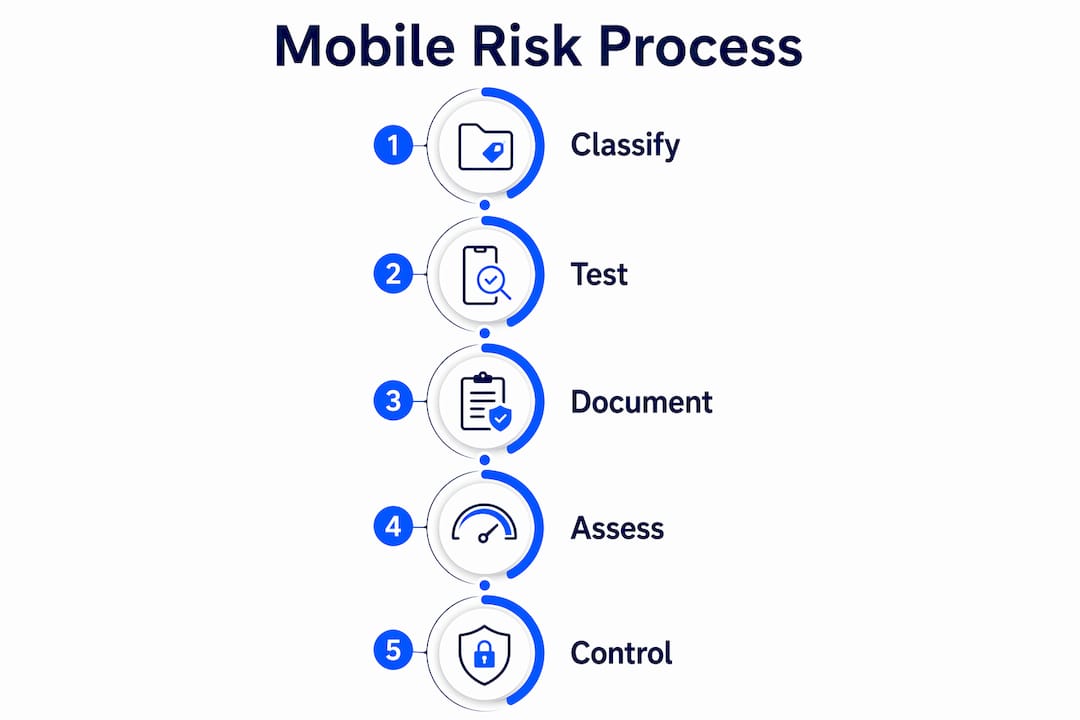

The program's architecture rests on three pillars: classification, testing, and documentation. Classification assigns each mobile app a tier, typically high, medium, or low, based on criteria such as data sensitivity, transaction volume, and regulatory exposure. A mobile banking app handling ACH transfers sits in the high tier; an internal employee scheduling tool sits in the low tier. Testing intensity scales accordingly, and documentation captures every result in a format auditors can interrogate.

| Business impact tier | Criteria | Testing requirements |

|---|---|---|

| High | Customer PII, financial transactions, regulatory scope | Automated testing, penetration testing, MFA verification, privacy assessment |

| Medium | Internal data, limited external exposure | Automated testing, periodic manual review, compliance spot checks |

| Low | Non-sensitive, internal tooling | Automated scanning, annual review |

Standards like OWASP MASVS, GDPR, HIPAA, and SOC 2 serve as the compliance baseline for each tier. A MARM program maps testing results directly to these frameworks, enabling real-time remediation guidance and continuous audit-ready evidence collection integrated into DevSecOps pipelines. This is the operational difference between a financial institution that scrambles during an exam and one that produces a complete evidence package within hours.

How does privacy risk fit into mobile security management?

Privacy risk is no longer a subset of security risk. It is a distinct and critical domain requiring its own quantification methodology, particularly for mobile apps that collect behavioral data, location signals, and biometric inputs. Financial institutions operating under GDPR, CCPA, or state-level privacy statutes face direct liability when mobile apps fail to honor data minimization or consent requirements.

The SafeMountain framework, published in peer-reviewed research, demonstrates how AI-driven privacy risk assessment can systematically quantify and visualize privacy risks in mobile apps using a combination of static code analysis, dynamic runtime analysis, and natural language processing of privacy policies. It evaluates risk across dimensions including predictability, manageability, and disassociability, producing scores that developers, compliance officers, and regulators can act on independently. This is a materially different output from a binary pass/fail security scan.

For a credit union deploying a mobile lending app, this means the privacy risk assessment runs alongside the security assessment, not after it. The NLP component flags discrepancies between what the app's code actually collects and what the privacy policy discloses to users. That gap, when undetected, is precisely the kind of finding that generates regulatory enforcement actions.

Pro Tip: Treat privacy risk scoring as a release gate, not a post-launch review. Integrating SafeMountain-style NLP analysis into your CI/CD pipeline catches policy-to-code mismatches before they reach production, where remediation costs multiply.

Privacy risk programs that treat privacy as a first-class risk alongside security, aligned to GDPR and other international standards, produce more objective compliance postures and more credible remediation plans. For financial institutions with cross-border customers, this alignment is not optional.

How does AI/ML in mobile apps change the risk equation?

Financial institutions are embedding machine learning models directly into mobile apps for credit scoring, fraud detection, and behavioral authentication. Each embedded model introduces a category of risk that standard application security testing does not cover: model risk. Understanding mobile risks in this context requires expanding the MARM program to include model governance.

Oracle's Financial Services Model and AI Risk Management platform provides a working template. Oracle's MARM framework governs the AI/ML lifecycle with multi-stage validation, automated drift detection, back-testing, and comprehensive findings management, all mapped to regulatory mandates including SR 11-7 and SR 15-18. These Federal Reserve guidance documents establish the standard of care for model risk in supervised financial institutions, and they apply equally to models running on a server and models running inside a mobile app.

The operational steps for managing AI risk in mobile financial apps follow a defined sequence:

- Model inventory and classification. Register every AI/ML model embedded in mobile apps, including third-party SDKs that contain pre-trained models, and assign each a risk rating based on its decision authority and data inputs.

- Multi-stage validation. Conduct conceptual soundness review, outcome analysis, and sensitivity testing before any model reaches production in a mobile release.

- Automated drift detection. Monitor model performance continuously post-deployment. A fraud detection model that degrades in accuracy after a mobile OS update represents an unacceptable operational risk.

- Back-testing and findings management. Run periodic back-tests against historical data and track all findings through a formal remediation workflow with documented closure evidence.

"Mobile AI/ML risk management requires governance that extends beyond application security, incorporating enterprise model risk frameworks with validation, monitoring, drift detection, and comprehensive findings management." — Oracle Financial Services documentation

Model risk governance frameworks used in financial services serve as operational templates for managing embedded AI risk in mobile financial applications. For risk officers at community banks and credit unions, this means the model risk policy must explicitly address mobile deployment scenarios, not just server-side inference.

How to implement a mobile risk management program

Operationalizing a MARM program in a financial institution requires cross-functional alignment before any tooling decision. The step-by-step risk assessment process for financial institutions provides a structural foundation, but mobile-specific implementation adds several layers that general frameworks do not address.

The first requirement is a production-readiness definition. Every mobile app release must clear a documented checklist that specifies which security controls, privacy assessments, and compliance checks must pass before deployment. This definition is the anchor for the entire program. Without it, teams make inconsistent release decisions and auditors find inconsistent evidence.

The second requirement is automation integrated into the CI/CD pipeline. Mobile security risk assessments covering dynamic and static analysis, OWASP Mobile Top 10 checks, and penetration testing should run on every build for high-tier apps, with quarterly manual penetration tests supplementing automated coverage. Automation does not replace human judgment; it removes the manual bottleneck that causes security reviews to become release delays.

- Map evidence to controls. Every test result must link to a specific OWASP MASVS control, GDPR article, or SOC 2 criterion. Unmapped results are operationally useless during an audit.

- Assign ownership by tier. High-tier apps require a named risk owner accountable for remediation timelines. Medium and low-tier apps can operate under shared ownership models.

- Schedule continuous improvement reviews. Quarterly reviews of the MARM program itself, not just the apps it covers, identify gaps created by new mobile OS features, new regulatory guidance, or new AI capabilities embedded in the app portfolio.

- Maintain a third-party SDK register. Third-party SDKs introduce permissions and data flows that the institution did not write and may not fully understand. Each SDK in a high-tier app requires its own risk assessment.

Pro Tip: The biggest obstacle in MARM programs is not tooling. It is the absence of a structured, continuously updated framework that defines production readiness and generates audit-ready evidence. Solve the process problem first, then select tools that fit the process.

Audit questions become expensive without clear provability frameworks that tie each test result to specific controls and business impact tiers. Financial institutions that build this mapping into their MARM program from the start spend significantly less time reconstructing evidence during examinations. The risk management documentation standards that apply to broader enterprise risk programs apply with equal force to mobile app portfolios.

Key takeaways

Mobile App Risk Management is the structured discipline that separates financial institutions with defensible mobile security postures from those that reconstruct evidence under regulatory pressure.

| Point | Details |

|---|---|

| Define production readiness first | Establish documented release criteria before selecting tools or running tests. |

| Tier apps by business impact | High-tier apps require penetration testing, MFA checks, and privacy assessments; low-tier apps need annual automated scans. |

| Treat privacy as a separate risk domain | Use AI-driven frameworks like SafeMountain to score privacy risk independently from security risk. |

| Extend MARM to cover AI/ML models | Embedded models in mobile financial apps require SR 11-7 compliant validation, drift detection, and back-testing. |

| Automate evidence mapping | Link every test result to a specific control standard and business impact tier to satisfy audit requirements efficiently. |

Why the process problem matters more than the tool problem

The most persistent misconception I encounter among risk officers at community banks and credit unions is that mobile security is a tooling problem. Buy the right scanner, run it on schedule, and the risk is managed. That framing is wrong, and it is expensive to be wrong about it.

The real gap, as NowSecure CEO Alan Snyder articulated in 2025, is the absence of a structured framework that defines production readiness and generates consistent, audit-ready evidence. Tools produce data. A MARM program produces defensible decisions. Those are not the same thing, and examiners know the difference.

What I find particularly underappreciated is the AI/ML governance dimension. Financial institutions have spent years building model risk programs for server-side models. The moment those models move into a mobile app, many institutions treat them as an app security problem rather than a model risk problem. The regulatory expectation under SR 11-7 does not change based on where the model runs. A credit scoring model embedded in a mobile lending app carries the same validation and monitoring obligations as one running in a core banking system.

The institutions that will manage mobile risk well over the next three years are the ones building MARM programs that span application security, privacy governance, and model risk governance as a single integrated discipline. That requires policy evolution, not just tool procurement. The AI risk management practices that apply to enterprise AI programs need explicit mobile deployment chapters added now, before the next examination cycle.

— Raj

How Riskinmind supports mobile risk and compliance readiness

Riskinmind's AI-powered platform is built specifically for the risk and compliance demands of financial institutions, including the mobile risk assessment and governance requirements that modern MARM programs require.

The platform's AI agents, coordinated by Ava, automate credit risk assessment, regulatory compliance monitoring, and portfolio analysis with response times under half a second. For institutions managing mobile lending workflows, Riskinmind's loan application risk evaluation tool integrates AI-driven underwriting with the audit-ready documentation standards that examiners expect. The peer benchmarking and risk analytics module gives risk officers comparative context for mobile risk posture across peer institutions. Riskinmind holds SOC 2® certification and operates at bank-grade security standards, making it a credible partner for institutions building or scaling their mobile risk programs.

FAQ

What is mobile app risk management (MARM)?

Mobile App Risk Management is a structured, continuous program that organizes, tests, and documents the security and compliance readiness of mobile applications, mapped to business impact tiers and standards like OWASP MASVS, GDPR, and SOC 2.

How often should financial institutions test mobile apps for security risks?

Critical and high-tier mobile apps require automated testing on every build cycle and manual penetration testing at least quarterly, per VISTA InfoSec guidance, with medium and low-tier apps reviewed on annual or semi-annual schedules.

What standards apply to mobile risk management in financial institutions?

OWASP MASVS, GDPR, HIPAA, SOC 2, and Federal Reserve guidance SR 11-7 and SR 15-18 are the primary frameworks governing mobile app security, privacy, and AI/ML model risk in regulated financial institutions.

How does AI/ML in mobile apps affect model risk obligations?

Embedding AI/ML models in mobile financial apps does not reduce model risk obligations. SR 11-7 validation, drift detection, and back-testing requirements apply regardless of whether the model runs server-side or within a mobile application.

What is the biggest gap in most mobile risk management programs?

The primary gap is the absence of a structured framework that defines production readiness and generates audit-ready evidence, not a shortage of security tools, as NowSecure's 2025 analysis confirms.