Regulatory reporting in financial institutions has never been more demanding. Compliance officers and risk managers face mounting pressure from regulators who expect data that is both timely and accurate, not merely complete. A poorly structured compliance reporting workflow is more than an operational inconvenience. It creates supervisory exposure, delays corrective action, and undermines the audit readiness that examiners increasingly scrutinize. This guide addresses the full lifecycle of regulatory reporting, from foundational prerequisites through data collection, report execution, and post-submission improvement, giving you a practical framework to sharpen your institution's reporting posture in 2026.

Key takeaways

| Point | Details |

|---|---|

| Build foundational structure first | Map regulatory obligations, assign ownership, and deploy a compliance tracking system before optimizing execution. |

| Data quality is a supervisory lever | The Federal Reserve treats timeliness and accuracy as inputs to early problem identification, not administrative formalities. |

| Automate with governance intact | Automated reporting solutions reduce errors and accelerate production, but immutable audit logs must be preserved throughout. |

| Incident disclosures require urgency | Regulators expect prompt self-reporting at the earliest opportunity, not deferred to the next periodic cycle. |

| Continuous assessment drives improvement | Quarterly workflow reviews and operational dashboards help identify gaps before examiners do. |

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

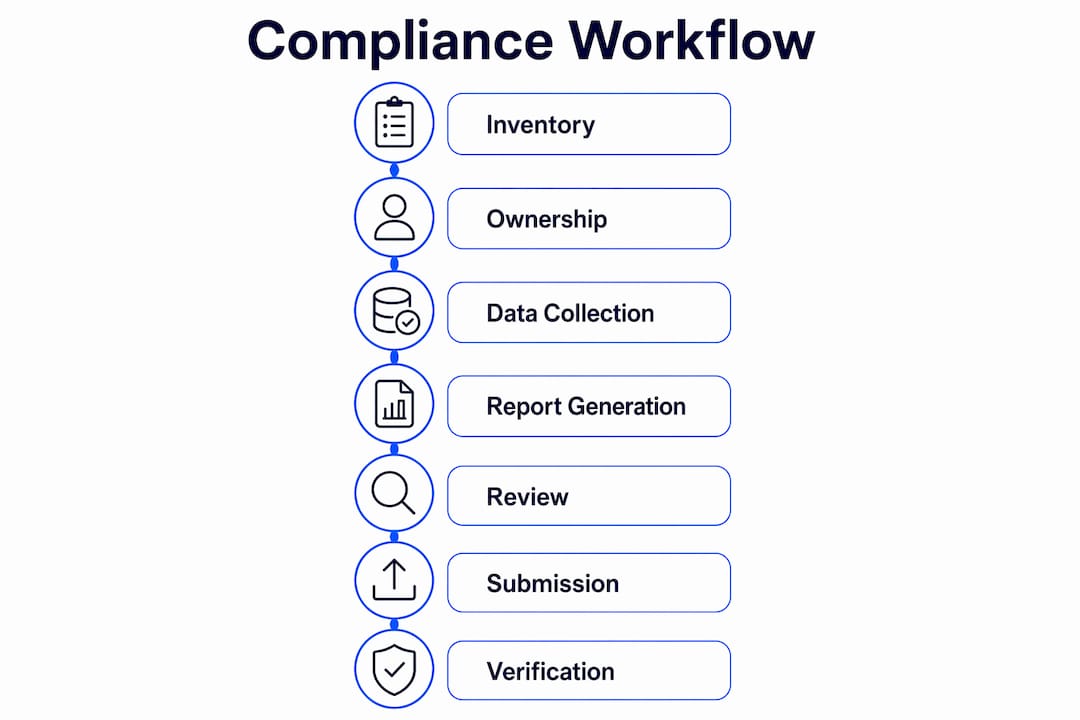

What your compliance reporting workflow actually needs first

The industry term covering this discipline is "regulatory reporting," and the compliance reporting workflow is how institutions execute that obligation at the operational level. Many optimization efforts fail because they address execution before the foundation is solid. Getting the prerequisites right determines whether every downstream step succeeds or compounds existing problems.

The starting point is a complete inventory of your reporting obligations across all applicable frameworks, whether that is the Call Report, BSA/AML filings, stress testing submissions, or consumer protection disclosures. Each obligation carries its own data requirements, submission format, and timing rules, and EU Regulation 2024/3117 is a useful reference for how regulators formalize these requirements, specifying submission dates and threshold-based start and stop criteria for Annex I data submitted monthly, quarterly, semi-annually, or annually.

Equally critical is defining who owns what. Ambiguous ownership is the single most common source of late or incomplete submissions in community banks and credit unions. Every report line, data element, and submission step should map to a named owner with a documented backup. Once ownership is clear, your compliance tracking system becomes a genuine operational tool rather than a reference document. The control-to-evidence-to-report framework, where every report element links to an owned control with time-bounded evidence, is the gold standard for audit readiness and traceability.

Your toolkit should include automated reporting solutions capable of pulling data from core banking systems, loan origination platforms, and third-party data providers without manual re-keying. Defensible record-keeping is not optional. Every data pull, transformation, and submission step must generate tamper-evident documentation that an examiner can follow without ambiguity.

The table below summarizes the foundational components and their primary function:

| Foundational component | Primary function |

|---|---|

| Regulatory obligation inventory | Maps all reporting requirements, frequencies, and deadlines |

| Ownership and accountability matrix | Assigns named owners to each data element and submission step |

| Compliance tracking system | Monitors status, flags gaps, and documents evidence |

| Automated data integration | Pulls from source systems without manual re-keying |

| Tamper-evident record-keeping | Supports audit readiness and chain-of-custody questions |

Preparing, collecting, and validating compliance data

Data readiness is where most reporting failures originate. A report that misses a submission window or contains material errors often traces back to a broken data collection process, not a last-minute execution problem. The following sequence gives compliance teams a repeatable approach to data preparation.

-

Define the data universe for each report. Before collecting anything, document exactly which data fields are required, which source systems hold them, and which business unit is responsible for producing them. This specification should live in your workflow management tools as a standing requirement, updated whenever regulatory guidance changes.

-

Set collection triggers and deadlines upstream. Collection deadlines should sit at least five business days before the regulatory submission deadline. This buffer accommodates validation, escalation, and correction cycles without creating last-minute pressure.

-

Apply structured validation immediately upon receipt. Automated validation checks, including range tests, completeness checks, and cross-field consistency rules, should run as soon as data enters the workflow. Automated regulatory reporting solutions standardize data formats and perform variance analysis to flag anomalies before a human reviewer ever sees the file.

-

Conduct variance analysis against prior periods. Material changes in reported figures without a documented business explanation are a common exam finding. A formal variance analysis step, comparing current period data against prior submissions and internal forecasts, forces departments to explain movements before the report leaves the institution.

-

Document the data lineage for every material line item. Regulators increasingly expect institutions to demonstrate not just what was reported, but where the data came from and who verified it. This documentation requirement ties directly to the control-to-evidence-to-report chain referenced earlier.

-

Apply start and stop reporting criteria systematically. For institutions subject to threshold-based requirements like those in EU supervisory frameworks, your workflow must automatically flag when a reporting obligation activates or deactivates based on current period thresholds, rather than relying on a compliance officer to remember.

The Federal Reserve's supervisory expectations are explicit: timeliness and accuracy in regulatory reporting directly affect supervisory interventions. A missed deadline or a material restatement is not a paperwork problem. It is a signal to examiners that internal controls may be weak.

Pro Tip: Set automated alerts in your compliance tracking system to flag data that has not been received from a source department by the collection deadline. Silent non-delivery is harder to catch than an outright error, and it surfaces far too late when discovered manually.

Executing report generation and submission

Execution is where well-designed workflows separate themselves from improvised ones. The goal at this stage is to eliminate manual touchpoints wherever governance allows, while maintaining the audit trail integrity that regulators and internal audit teams require.

Automating report production through workflow management tools offers the highest leverage point in the entire process. The last-mile automation of template standardization and validation reduces reconciliation time and errors more than any other single intervention. When report templates are locked to the validated data source and populated programmatically, the risk of transcription errors drops to near zero.

The review and signoff protocol matters as much as the automation. A well-structured workflow routes the draft report to the appropriate reviewer based on report type and materiality threshold. Escalation paths should be defined in advance, so that a reviewer who is unavailable does not become a submission bottleneck. Every review action, including who reviewed, what was changed, and when approval was granted, must be captured in an immutable audit log that is cryptographically chained and exportable to regulatory formats on demand.

Incident disclosures require a separate workflow track. Regulators expect disclosure at the earliest possible opportunity, not deferred to the next quarterly submission cycle. Early self-reporting improves cooperation credit and remediation outcomes materially. Your workflow should include a dedicated incident escalation path that bypasses standard periodic reporting timelines when a disclosable event occurs.

The comparison below illustrates the difference between manual and automated execution on key workflow dimensions:

| Workflow dimension | Manual execution | Automated execution |

|---|---|---|

| Data population | Spreadsheet re-keying, high error rate | Programmatic pull from validated source |

| Validation | Spot-check by reviewer | Systematic rules applied at ingestion |

| Audit trail | Email chains and file versions | Immutable, timestamped log entries |

| Incident disclosure | Dependent on staff awareness | Triggered alert with escalation routing |

| Submission confirmation | Manual filing confirmation email | System-generated receipt with timestamp |

Pro Tip: Review your risk reporting optimization practices periodically to identify where manual steps have crept back into automated workflows, particularly after staff turnover or system upgrades.

Reducing unnecessary interface steps for compliance reviewers is also worth prioritizing. Workflow redesign that cuts friction for reviewers can cut investigation time by up to 50% without compromising auditability, provided that governance controls and immutable records remain intact. Fewer clicks between receiving a report and approving it means faster throughput and fewer errors introduced at the review stage.

Post-submission verification and continuous improvement

Submission is not the end of the process. The highest-performing compliance programs treat the post-submission phase as a structured cycle of verification and refinement.

-

Confirm regulatory receipt and acknowledgment. Do not assume a submitted report was received. Your workflow should require documented confirmation from the regulatory authority or submission portal before closing the reporting cycle for that period.

-

File amendments without delay when errors surface. If a material error is identified after submission, the instinct to wait until the next reporting period is the wrong one. Prompt amendment demonstrates good faith and reduces the risk of an examiner discovering the error independently, which carries a significantly worse outcome.

-

Run a post-submission debrief within 48 hours. Gather the compliance team to document what worked, what broke down, and what near-misses occurred. This debrief should feed directly into your workflow documentation as an updated risk log entry.

-

Review operational dashboards monthly. Operational dashboards that surface metrics on alert rates, data delivery timeliness, and reviewer workload allow compliance leaders to measure program health between exam cycles, not just during them. This is also where patterns of recurring data quality issues become visible before they become exam findings.

-

Conduct a formal quarterly compliance assessment. Frameworks such as SOX 404 and NIST 800-53 recommend audit record reviews at least once every 90 days. Applying the same discipline to your regulatory reporting workflow, with defined review scripts and documented outcomes, operationalizes compliance effectiveness rather than leaving it to intuition.

-

Incorporate examiner feedback into workflow updates. When regulators provide commentary on your submissions, whether in examination findings, MRAs, or informal feedback, that input should trigger a documented workflow review within 30 days. Treating examiner feedback as a product of continuous improvement rather than a one-time remediation event changes the posture of the entire compliance function.

The AI-driven compliance monitoring practices now available to financial institutions make this continuous improvement cycle faster and less resource-intensive than it was even three years ago. The key is building the habit of measurement before the capability for automation arrives.

My perspective on getting compliance workflows right

I've spent enough time working with compliance teams at financial institutions to know that the failures rarely happen at the point everyone is watching. They happen in the quiet spaces between collection and validation, or between submission and confirmation, where no one thought to build a checkpoint.

What I've found is that most institutions understand the importance of accuracy. Fewer actually treat timeliness with the same seriousness. The Federal Reserve is explicit that late data affects supervisory interventions. A report filed two days late does not just trigger a procedural finding. It signals to examiners that the institution's internal controls may not be functioning as described.

The other thing I've observed is that the value of immutable audit logs is consistently underestimated until an examiner asks a chain-of-custody question that no one can answer. Building cryptographically chained records is not about bureaucracy. It's about being able to prove, without ambiguity, that your reported data is what you say it is.

My honest take on AI support in this space: it's most valuable not in generating reports but in monitoring the workflow that produces them. Identifying a data delivery failure before the collection deadline, or flagging a variance that exceeds historical norms, is where automation earns its keep in a compliance function.

— Raj

How Riskinmind supports your compliance reporting process

Riskinmind's AI-powered platform is built for exactly the operational reality this article describes. Financial institutions using Riskinmind gain access to a suite of specialized AI agents, coordinated by Ava, that automate data collection, validation, and regulatory reporting functions with response times under half a second. The platform's risk management solutions are SOC 2® certified and purpose-built for credit unions, community banks, and lenders operating under demanding regulatory schedules.

For institutions managing credit-related compliance, tools like the CRE loan risk predictor generate the kind of structured, audit-ready outputs that feed directly into regulatory submissions without manual rework. Real-time dashboards give compliance officers a continuous view of portfolio risk and reporting status, reducing the end-of-cycle scramble that characterizes underpowered workflows. If you want to see how AI-driven automation translates into audit readiness and operational efficiency for your institution, the platform is worth a close look.

FAQ

What is a compliance reporting workflow?

A compliance reporting workflow is the structured sequence of steps a financial institution follows to collect, validate, produce, and submit regulatory reports. It includes data sourcing, review and approval protocols, submission, and post-submission verification.

How does automation improve the regulatory reporting process?

Automated reporting solutions standardize data formats, run validation checks at ingestion, and populate report templates programmatically, reducing manual errors and accelerating submission timelines without sacrificing audit trail integrity.

Why do immutable audit logs matter for compliance reporting?

Immutable audit logs capture every access and action with tamper-evident records, giving institutions a defensible chain of custody for every reported data element and enabling rapid response to examiner questions about data provenance.

When should incident disclosures be made in a compliance workflow?

Regulators expect incident disclosures at the earliest possible opportunity rather than deferred to the next periodic reporting cycle, because early self-reporting improves cooperation credit and supports better remediation outcomes.

How often should compliance workflows be formally reviewed?

Quarterly assessments aligned with frameworks like SOX 404 and NIST 800-53 represent a recognized standard, supplemented by post-submission debriefs after each reporting cycle and prompt reviews following examiner feedback.