Automated underwriting is defined as a software-based process that evaluates loan or insurance applications using predefined rules, statistical models, and algorithms to generate objective, data-driven risk decisions without requiring manual review for every file. The term "automated underwriting system" (AUS) is the recognized industry standard for this technology, used across mortgage lending, commercial credit, and insurance policy issuance. Where a manual underwriter might spend hours reviewing a single file, an AUS processes the same application in seconds. For credit unions, community banks, and lenders managing high application volumes, that speed difference is not a convenience. It is a competitive necessity. Understanding how these systems work, what they produce, and where human judgment still belongs is the foundation of sound risk management in 2026.

What is automated underwriting and how does it work?

The automated underwriting process operates as a staged, rules-based engine that handles clean applications immediately and routes complex files for human review. That architecture is not accidental. It reflects a deliberate design to separate high-confidence decisions from borderline cases that require judgment.

The process follows a clear sequence:

-

Data collection and validation. The system ingests structured inputs: borrower financials, credit bureau data, debt-to-income ratios, asset documentation, and property or policy details. Data readiness is the most critical factor for successful implementation. Unstructured or incomplete data produces unreliable outputs regardless of how sophisticated the engine is.

-

Rules engine evaluation. The system applies the institution's credit policy and risk appetite as a set of coded business rules. These rules check eligibility thresholds: minimum credit scores, maximum loan-to-value ratios, income verification requirements, and regulatory compliance criteria.

-

AI and machine learning scoring. Beyond static rules, modern systems combine rules-based engines with AI and machine learning models that generate risk scores. These models identify patterns across thousands of historical applications to predict default probability with greater accuracy than any single rule can achieve.

-

Decision output. The system produces one of three outcomes: Approve/Eligible, Refer for manual review, or Ineligible/Deny. Each outcome carries a defined meaning within the decision workflow and triggers a corresponding next step.

-

Audit trail generation. Every rule applied and every score generated is logged. This audit trail documents the full decision path for compliance review, dispute resolution, and regulatory examination.

Pro Tip: An automated approval is a validated recommendation, not a final loan approval. Human verification of the underlying documentation remains required before any commitment is made.

What are the main benefits of automated underwriting for finance professionals?

The benefits of automated underwriting extend well beyond processing speed. The measurable impact on portfolio quality, operational cost, and regulatory standing makes a strong case for adoption across lending and insurance.

-

Speed and throughput. An AUS evaluates an application in seconds. That turnaround compresses the loan origination cycle and improves borrower experience without adding headcount.

-

Decision consistency. Every application runs through the same rules and models. Human underwriters, regardless of skill, introduce variability based on experience, workload, and unconscious bias. Automated systems reduce human bias by relying on consistent, data-driven decisioning that meets regulatory expectations.

-

Improved portfolio metrics. Institutions that adopt automated underwriting report loss ratio improvements of 3–5 points, premium growth of 10–15%, and retention increases of 5–10%. Those figures reflect better risk selection, not just faster processing.

-

Regulatory transparency. The logged audit trail produced by every AUS decision supports examination readiness and reduces the risk of fair lending violations. Regulators can trace every decision back to a specific rule or model output.

-

Operational cost savings. Automating high-volume, straightforward applications frees underwriting staff to focus on complex files. That reallocation reduces per-application cost and improves the quality of human review where it matters most.

The benefits of automated credit scoring are closely tied to these outcomes. When credit scoring models feed directly into the AUS, the combined system produces risk assessments that are both faster and more granular than manual scoring alone. For finance professionals managing auto loan decisions or commercial credit portfolios, that granularity translates directly into lower loss rates.

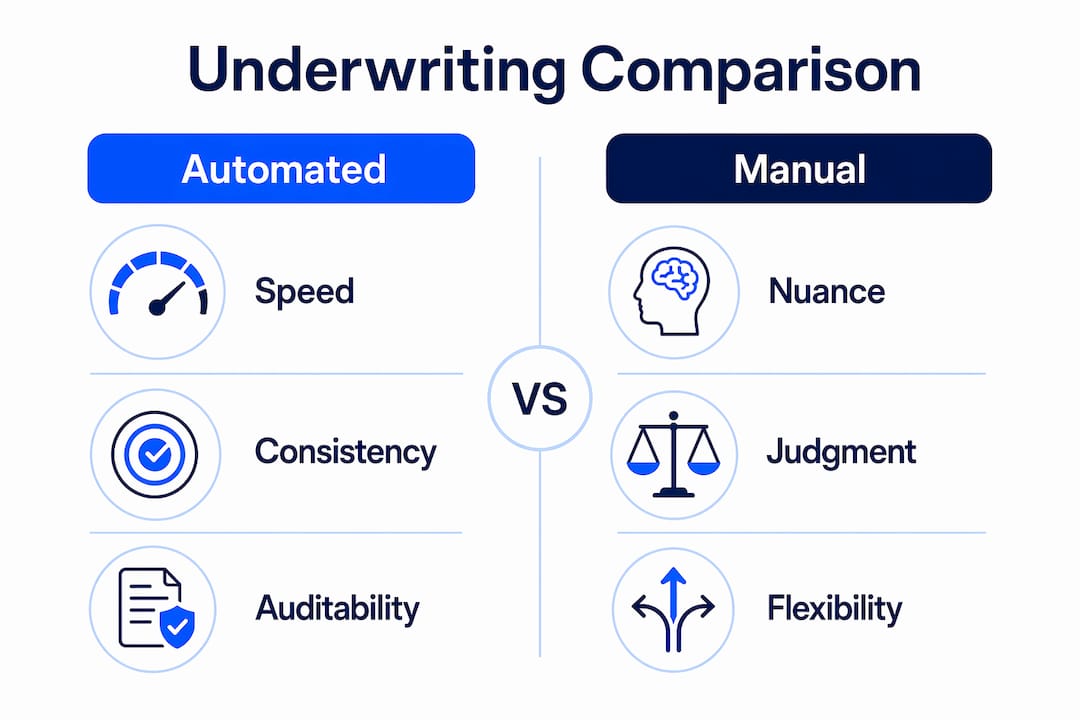

Automated underwriting versus manual underwriting: What finance professionals need to know

The distinction between automated and manual underwriting is not a question of which is better. It is a question of which is appropriate for a given file.

Manual underwriting relies on a human underwriter reviewing documents, applying judgment, and making a credit decision based on experience and policy guidelines. That process works well for complex borrowers: self-employed applicants with non-standard income, commercial loans with unusual collateral structures, or files where the data tells an incomplete story. Manual review captures context that a rules engine cannot code.

Automated underwriting handles the opposite end of the spectrum. Clean files with complete, structured data and straightforward risk profiles move through an AUS without delay. The system applies policy rules and model scores consistently, producing a decision that would take a human underwriter significantly longer to reach. Automation reallocates human underwriters to focus on complex or borderline cases, which is where their judgment adds the most value.

The most effective institutions run hybrid workflows. The AUS handles volume. Human underwriters handle nuance. That division of labor improves both accuracy and resource allocation.

| Dimension | Automated underwriting | Manual underwriting |

|---|---|---|

| Speed | Seconds per application | Hours to days per application |

| Consistency | Uniform across all files | Variable by underwriter |

| Best fit | Clean, structured, standard files | Complex, borderline, or non-standard files |

| Audit trail | Automatic and complete | Dependent on documentation discipline |

| Bias risk | Low, rules-driven | Higher, subject to human judgment |

A common misconception is that automated decisions are inherently less fair than human decisions. The evidence runs the other way. Automated systems apply the same criteria to every applicant. Human underwriters, even well-trained ones, are susceptible to unconscious bias. The fairness advantage of consistent, data-driven decisioning is one of the strongest arguments for AUS adoption in fair lending compliance programs.

Pro Tip: Review your AUS referral rate quarterly. A rising referral rate often signals that your data inputs are degrading or that your rules engine needs recalibration against current portfolio performance.

Practical applications of automated underwriting in risk management

Automated underwriting software operates across three primary domains in financial services: mortgage lending, insurance policy issuance, and commercial credit.

In mortgage lending, AUS platforms evaluate borrower credit profiles, income documentation, and property appraisals against agency guidelines. The system routes approvals directly to closing preparation and flags referrals for underwriter review. That workflow compresses origination timelines and reduces the cost per funded loan.

In insurance, automated underwriting improves risk assessment accuracy, workflow efficiency, and customer satisfaction. Carriers use AUS platforms to evaluate applicant risk profiles against actuarial models, issue policies faster, and personalize coverage terms based on data rather than broad demographic assumptions.

In commercial credit, the applications are more varied. Lenders use automated scoring to evaluate small business loan applications, commercial real estate risk, and line-of-credit renewals. The role of AI in loan underwriting has expanded significantly as machine learning models become better at processing non-traditional data sources alongside standard financial statements.

The implications for risk management are direct:

- Decision traceability improves examination readiness under frameworks like the Equal Credit Opportunity Act (ECOA) and the Fair Housing Act (FHA).

- Portfolio monitoring becomes more consistent when the same models that score new applications also flag deteriorating credits in the existing book.

- Regulatory reporting is faster when the AUS generates structured data outputs that feed directly into compliance workflows.

The future of automated underwriting points toward greater integration between origination systems and ongoing portfolio surveillance. Automation in financial compliance is no longer a back-office function. It is a front-line risk management tool that shapes credit quality from the moment an application enters the system.

Key Takeaways

Automated underwriting systems deliver faster, more consistent, and more auditable credit decisions than manual processes, but their effectiveness depends entirely on the quality of structured data inputs and continuous model calibration.

| Point | Details |

|---|---|

| Core definition | An AUS uses rules engines and AI models to generate risk decisions from structured application data. |

| Three decision outcomes | Every AUS produces Approve/Eligible, Refer for manual review, or Ineligible/Deny as its output. |

| Measurable portfolio impact | Adoption correlates with 3–5 point loss ratio improvements and 10–15% premium growth. |

| Hybrid workflows win | Automated systems handle volume; human underwriters handle complex and borderline files. |

| Data quality is the constraint | Unstructured or incomplete inputs undermine AUS accuracy regardless of model sophistication. |

The case for treating automation as a discipline, not a deployment

The finance professionals I respect most treat automated underwriting as an ongoing discipline rather than a one-time technology deployment. The temptation after go-live is to trust the system and move on. That is where institutions get into trouble.

The models inside an AUS are trained on historical data. When economic conditions shift, when borrower behavior changes, or when your institution's risk appetite evolves, the model's assumptions can drift out of alignment with reality. I have seen institutions run AUS platforms for years without recalibrating the underlying scoring models, then wonder why their referral rates climbed or their approval quality declined.

The audit trail is your best diagnostic tool. If you are not reviewing it regularly, you are flying without instruments. Every referral pattern, every rule trigger frequency, and every model score distribution tells you something about the health of your decisioning engine.

The fairness argument for automation is real, but it requires active management. A biased training dataset produces a biased model. The system will apply that bias consistently, which makes it harder to detect than the variable bias of individual underwriters. Institutions that take fair lending compliance seriously audit their AUS outputs for disparate impact on a regular schedule, not just at examination time.

My strongest recommendation: treat your AUS as a living system. Calibrate it. Challenge it. And never let an automated approval substitute for the human verification that turns a recommendation into a commitment.

— Raj

How Riskinmind supports intelligent underwriting decisions

Riskinmind's AI-powered risk management platform is built for credit unions, community banks, and lenders that need faster, more defensible credit decisions without sacrificing accuracy or compliance.

The platform's AI agents handle credit risk assessment, regulatory compliance monitoring, and portfolio surveillance in real time, with response times under half a second. Ava, Riskinmind's central AI director, coordinates specialized agents to deliver consistent, audit-ready outputs that support both origination and ongoing portfolio management. For institutions ready to move beyond manual workflows, the loan application underwriting tools and the broader AI risk management platform offer a practical starting point. SOC 2® certification and bank-grade security mean your data and your borrowers' data stay protected throughout every decision.

FAQ

What is the automated underwriting definition in simple terms?

Automated underwriting is a software process that evaluates loan or insurance applications using predefined rules and statistical models to produce a risk decision without requiring manual review for every file.

How does automated underwriting differ from a credit score?

A credit score is a single numeric output from a credit bureau model. An automated underwriting system uses that score as one input among many, applying the lender's full credit policy to produce an Approve, Refer, or Deny decision.

Are automated underwriting approvals final?

Automated approvals are validated recommendations, not final commitments. Human verification of the underlying documentation is required before any loan is funded or policy is issued.

What data does an automated underwriting system require?

An AUS requires structured, validated inputs including credit bureau data, income documentation, debt-to-income ratios, asset statements, and property or policy details. Incomplete or unstructured data degrades decision accuracy.

What is the biggest risk of automated underwriting?

The biggest risk is model drift. When economic conditions or borrower behavior change, an uncalibrated AUS can produce decisions that no longer reflect the institution's actual risk appetite or current portfolio performance.