Most risk management professionals think of their platform as a place to document what already happened. A repository for post-incident reports, a dashboard updated quarterly, a system that tells you where you failed after regulators are already asking questions. That framing is not just outdated. It is operationally dangerous. The real question driving investment decisions right now is why secure risk platforms have become the operational backbone of financial compliance, not just a supporting tool. When security is built into the risk platform architecture itself, through zero-trust access, immutable logs, and real-time monitoring, the entire posture of your institution shifts from reactive documentation to continuous, defensible control.

Table of Contents

- Key Takeaways

- What security in risk platforms actually means

- Why regulatory compliance now demands secure platforms

- Handling high-velocity and digital asset risk

- How to choose risk platforms with the right security foundation

- My perspective on secure risk platforms

- See how Riskinmind approaches platform security

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Security is architectural, not add-on | Zero-trust access, encryption, and immutable logs must be embedded in platform design, not bolted on afterward. |

| Compliance requires continuous proof | Regulations like DORA and SOC 2 demand real-time evidence, making periodic checklist audits legally insufficient. |

| Speed matters in digital asset risk | Platforms screening hundreds of millions of transactions monthly with sub-300ms response times define the new standard. |

| Integration determines evidence quality | Platforms must connect to identity and cloud infrastructure automatically to avoid manual bottlenecks that undermine audit reliability. |

| Platform selection is a strategic decision | Evaluating scalability, automation depth, and regulatory alignment separates capable platforms from ones that create compliance gaps. |

What security in risk platforms actually means

The phrase "secure risk platform" gets used loosely, but for financial institutions the definition has precise, operational implications. Security in risk platforms refers to the combination of confidentiality, integrity, and availability controls embedded directly into the platform's architecture, not layered on afterward as optional features.

Confidentiality means that data about credit exposures, borrower profiles, regulatory filings, and internal risk models is accessible only to those with verified, role-based authorization. Integrity means every record created in the system remains tamper-evident and trustworthy, even under audit pressure. Availability means the platform maintains uptime and performance under the transaction volumes that modern financial institutions actually generate.

The specific types of risk platform security features that matter most for financial institutions include:

- Zero-trust access control: Every user, device, and session is verified continuously, not just at login. This closes the insider threat window that traditional perimeter-based security leaves wide open.

- Immutable audit trails: Logs must be append-only and cryptographically signed to provide regulatory-grade evidence. Simply storing logs in a database is insufficient for modern audit requirements.

- Encryption in transit and at rest: Sensitive risk data, from loan officer notes to portfolio stress test outputs, requires encryption at the field level, not just at the connection level.

- Automated evidence collection: Integration with identity and cloud infrastructure is mandatory so the platform pulls evidence automatically, eliminating the manual data-gathering bottlenecks that become compliance liabilities at scale.

- Real-time monitoring and alerting: Security events, access anomalies, and control failures surface immediately rather than surfacing in a monthly report.

What makes these features collectively powerful is that they transform the platform from a passive documentation tool into an active control environment. A secure risk platform does not just record what happened. It enforces what is permitted, generates forensic-ready evidence as a byproduct of normal operations, and reduces the gap between a control failure and the response to it.

Pro Tip: When evaluating platforms, ask vendors specifically whether audit logs are cryptographically signed and append-only, or whether they are standard database records. The technical answer to that one question reveals the actual security architecture more clearly than any marketing document.

Why regulatory compliance now demands secure platforms

The compliance environment for financial institutions has shifted fundamentally, and the shift is not temporary. Regulatory frameworks including DORA (the Digital Operational Resilience Act), SOC 2, and ISO 27001 now require financial institutions to demonstrate continuous, verifiable control, not periodic documentation that everything was fine at the time of the last review.

DORA, which carries direct enforcement weight across EU financial services, mandates cryptographically signed audit logs stored in append-only repositories with millisecond-level precision. That specific technical requirement exists because regulators understand that standard database logs can be altered, selectively deleted, or reconstructed after the fact. Immutable, signed logs cannot be. The regulation is, in effect, mandating a security architecture decision.

SOC 2 and ISO 27001 have moved in the same direction. Treating compliance as a periodic checklist leads to weak evidence and higher audit costs, and governance leaders across the industry have emphasized that continuous oversight and real-time evidence gathering are the only defensible posture. Regulators now expect that evidence not just exists, but that it was generated automatically and cannot be selectively curated before an audit.

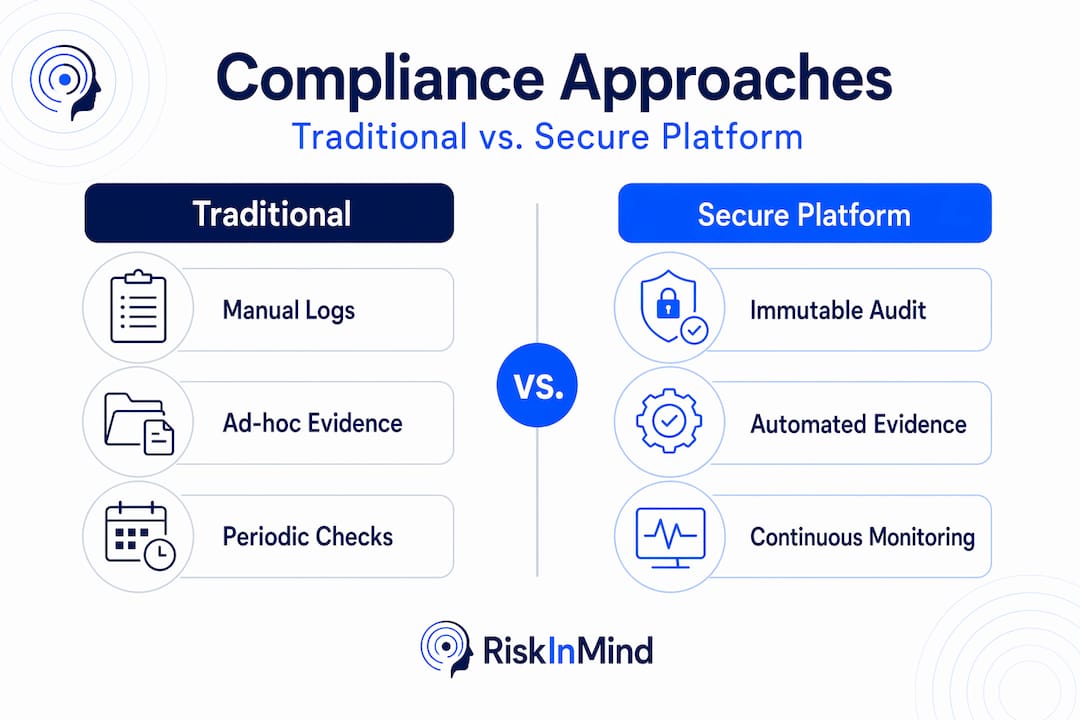

The table below illustrates how the compliance posture of institutions using secure risk platforms compares to those relying on traditional approaches.

| Compliance dimension | Traditional approach | Secure platform approach |

|---|---|---|

| Audit evidence | Manually assembled pre-audit | Continuously auto-generated |

| Log integrity | Standard database records | Cryptographically signed, append-only |

| Access control | Role-based at login | Zero-trust, session-level verification |

| Incident reporting | Post-incident reconstruction | Real-time capture with millisecond timestamps |

| Multi-framework coverage | Separate programs per framework | Unified evidence serving SOC 2, ISO 27001, DORA simultaneously |

AI-powered compliance platforms that automate evidence collection across multiple frameworks simultaneously reduce manual audit effort, accelerate preparation timelines, and increase accuracy across all of them at once. For institutions subject to multiple overlapping regulatory mandates, this is not a convenience. It is a material reduction in operational risk.

The NIST Risk Management Framework reinforces this logic. The monitor step in the NIST RMF is explicitly the starting point for continuous authorization, requiring immediate escalation when control metrics slip below acceptable thresholds. A platform without real-time monitoring cannot satisfy this requirement in practice, regardless of what documentation says.

Pro Tip: Map your current platform's evidence outputs directly against the specific technical requirements in DORA Articles 17 and 19 before your next audit cycle. Most institutions discover gaps in log integrity or access control granularity that only become visible when you compare platform capabilities to the actual regulatory text.

Handling high-velocity and digital asset risk

Modern financial institutions increasingly face risk environments that traditional platforms were not designed to handle. Digital asset exposure, onchain lending, and decentralized finance participation generate transaction volumes and exposure velocity that manual or batch-processing systems cannot monitor effectively.

The scale involved is not theoretical. Risk infrastructure operating in the digital asset space screens over 500 million blockchain transactions monthly with 99.99% accuracy and response times under 300 milliseconds. That performance standard matters because exposure in onchain environments can change materially in seconds, not hours. A platform that reports portfolio risk daily or even hourly is operationally blind to the risk that actually exists.

For institutions entering or managing digital asset portfolios, secure risk platforms that can operate at this velocity provide several distinct advantages:

- Pre-transaction policy enforcement: Risk policies execute before a transaction settles, not after, which means exposure limits are enforced rather than reported on retrospectively.

- Continuous exposure monitoring: Position-level risk is updated in real time as market conditions and counterparty behaviors change, providing portfolio managers with an accurate picture at every moment.

- Automated response triggers: When a position crosses a risk threshold, the platform initiates a predefined response automatically, whether that is an alert, a hold, or an escalation, without waiting for a human to notice the data.

- Forensic-ready transaction records: Every screening decision and policy verdict is logged with the precision required for regulatory incident reporting, creating an unbroken chain of evidence across millions of daily events.

The broader lesson for risk management professionals is that platforms screening onchain activity continuously represent a fundamentally different operational model. Compliance doesn't just happen at the end of a reporting period. It is enforced, recorded, and verified as a continuous operational function. This is what it means for a risk platform to be genuinely secure and genuinely real-time, and it is the standard that real-time risk monitoring now sets for institutions serious about portfolio protection.

How to choose risk platforms with the right security foundation

Decision-makers evaluating risk platforms face a market where every vendor claims robust security and continuous compliance. The practical challenge is separating architectural capability from marketing language. Here is a structured approach to how to choose risk platforms that will hold up under actual regulatory scrutiny.

-

Verify immutable audit trail architecture. Ask whether logs are stored in append-only repositories and cryptographically signed at the point of creation. Request technical documentation, not a sales summary. Platforms that cannot provide this documentation likely do not have the architecture.

-

Assess zero-trust implementation depth. Zero-trust is not a binary feature. Ask how access decisions are made within an active session, whether device health is verified continuously, and whether privileged access to risk data requires additional verification beyond standard login credentials.

-

Evaluate integration with your existing identity and cloud infrastructure. Policy enforcement layered at build-time, deployment, and runtime via automated tools creates the defense-in-depth that continuous compliance requires. A platform that requires manual data exports to populate compliance evidence is not actually continuous, regardless of what the dashboard shows.

-

Test scalability under your actual transaction volumes. Request performance benchmarks at volumes that match or exceed your peak operational load. Platforms that perform well in a demo environment but slow under real transaction volume create both operational and compliance risk.

-

Confirm multi-framework regulatory coverage. If your institution is subject to DORA, SOC 2, ISO 27001, or NIST RMF simultaneously, the platform should generate evidence that satisfies all of them from a single operational stream. Maintaining separate compliance programs for each framework is an organizational liability.

One area that frequently blinds institutions during procurement is the distinction between compliance monitoring best practices and what a platform actually delivers in production. The gap between a vendor's compliance claims and the platform's real behavior under an audit is where institutions get surprised. Reference checks with existing clients at comparable institutions are not optional. They are part of the security due diligence.

Pro Tip: Request a sample of auto-generated audit evidence from a prospective vendor's existing financial institution clients. Reviewing actual artifacts tells you more about evidence quality than any product demonstration.

My perspective on secure risk platforms

I've spent years watching financial institutions treat platform security as something to address after deployment, a configuration setting to enable, a compliance module to activate when an audit approaches. That approach fails consistently, and the pattern is predictable.

What I've found is that the institutions with the strongest compliance postures do not think of security as a feature of their risk platform. They think of it as the operating condition that makes the platform's outputs trustworthy at all. Immutable audit trails and zero-trust controls are not compliance decorations. They are the mechanisms that make a risk assessment credible to a regulator, a board, or a counterparty.

The harder lesson I've observed is cultural. Technology alone does not close the gap between a secure platform and a secure institution. Teams need to understand why the continuous evidence stream exists, what it captures, and how to use it when regulators start asking questions. Institutions that invest in the technology without investing in that operational understanding end up with a sophisticated system that generates excellent logs and a staff that doesn't know how to present them.

My advice to any CRO or risk committee evaluating platforms today: start with the audit trail architecture, verify zero-trust implementation at the session level, and then spend as much time on operational training as you do on the procurement process. The platform is the starting point. The culture that uses it correctly is the real competitive advantage.

— Raj

See how Riskinmind approaches platform security

Riskinmind is built specifically for credit unions, community banks, and lenders that need a risk platform with the security architecture this article describes. The platform carries SOC 2® certification and delivers AI-powered risk management with response times under 500 milliseconds, continuous compliance monitoring, and automated evidence generation across regulatory frameworks. Ava, the platform's central AI director, coordinates specialized agents across credit risk, regulatory compliance, and market analysis. All of them operating on a zero-trust, bank-grade security foundation. Explore transparent pricing options or review the automated risk management case to understand how institutions like yours are moving from periodic reporting to continuous, defensible compliance.

FAQ

What does security mean in a risk platform?

Security in risk platforms refers to confidentiality, integrity, and availability controls built into the platform architecture, including zero-trust access, immutable audit logs, and encryption. These features make risk data trustworthy and defensible under regulatory scrutiny.

Why do secure risk platforms matter for regulatory compliance?

Regulations like DORA and SOC 2 require continuous, verifiable evidence rather than periodic documentation. Secure platforms generate cryptographically signed audit logs automatically, which satisfies these mandates in ways that traditional systems cannot.

What are the most important security features to look for?

The features that most directly affect regulatory defensibility are immutable audit trails, zero-trust access control, automated evidence collection integrated with identity systems, and real-time monitoring that triggers escalation when controls fail.

How should financial institutions evaluate platform security claims?

Request technical documentation on log architecture, ask for zero-trust implementation details at the session level, and review actual audit artifacts from existing clients rather than relying on vendor demonstrations or marketing materials.

Can secure risk platforms handle digital asset and high-volume transaction environments?

Yes. Modern secure risk infrastructure screens over 500 million transactions monthly with sub-300ms response times, enabling policy enforcement before transactions settle rather than after exposure has already spread.