Technology risk doesn't announce itself. It accumulates quietly across IT infrastructure, third-party vendors, AI-driven systems, and regulatory obligations until the cost of ignoring it becomes undeniable. For risk management professionals at credit unions, community banks, and lenders, the question of why focus on risk technology is no longer theoretical. 61% of finance leaders report significant increases in risk volume and complexity over the past five years, and institutions that rely on spreadsheets and manual controls are falling further behind with each passing quarter.

Table of Contents

- Key takeaways

- Why focus on risk technology: the case for financial institutions

- From compliance checkbox to strategic risk enabler

- Concrete benefits of advanced risk management tools

- Practical guidance for implementing risk technology

- My perspective: why this shift cannot wait

- See how Riskinmind transforms risk operations

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Technology risk is multidimensional | Cyber, AI, third-party, and IoT risks combine to create exposure that manual controls cannot adequately address. |

| ERM must become strategic | Risk technology enables real-time decision support, moving ERM beyond quarterly compliance checkboxes. |

| Automation delivers measurable ROI | Automated workflows cut audit prep from weeks to hours and improve operational efficiency by 30 to 50 percent. |

| Adoption determines platform value | Simple, frequently updated tools that teams actually use outperform complex systems left unmaintained. |

| RegTech is the scalable path forward | Distributed RegTech platforms provide continuously updated regulatory expertise at lower cost than internal builds. |

Why focus on risk technology: the case for financial institutions

The importance of risk technology becomes clear once you map the actual scope of what financial institutions are managing. Technology risk is not a single category. It spans traditional IT infrastructure, operational technology, IoT-connected devices, third-party and vendor platforms, and now a rapidly expanding frontier of AI-driven systems. Each category introduces distinct exposure and requires different governance responses.

Consider the asset sprawl challenge alone. A mid-sized community bank may have hundreds of connected endpoints, dozens of third-party integrations, and multiple cloud environments, many of which are only partially inventoried. Fragmented technology asset landscapes undermine risk visibility and control across all of these environments, and manual monitoring simply cannot keep pace with the rate at which new exposures appear.

The threat environment compounds the problem. Frontier AI models now exceed skilled practitioners in the speed and scale of potential cyber attacks, which means institutions relying on human-speed detection and response are structurally disadvantaged against adversaries using AI to probe defenses. Regulatory complexity layers on further: with fragmented ownership across compliance, IT, and operations, risk accountability becomes diffuse and slow.

The categories of technology risk your institution faces today include:

- IT and cybersecurity risk: Data breaches, ransomware, unauthorized access, and system outages

- Third-party and vendor risk: Concentration risk from critical service providers and inadequate vendor controls

- AI and model risk: Bias, opacity, and governance failures in credit decisioning and automated processes

- Operational technology risk: Vulnerabilities in systems that support core banking operations

- Regulatory and compliance risk: Evolving rules from the CFPB, FFIEC, and prudential regulators that change faster than manual frameworks can track

Understanding this full scope is step one. Acting on it requires technology purpose-built for the task.

From compliance checkbox to strategic risk enabler

Here is an uncomfortable truth that most risk executives already know but rarely say out loud: more than 50% of organizations still treat enterprise risk management primarily as a compliance function rather than a strategic decision tool. Meanwhile, 98% of risk leaders want ERM to directly inform strategic decisions. That gap is where competitive advantage is won or lost.

COSO's 2026 ERM guidance makes this explicit. The new framework pushes organizations to embed risk thinking directly into strategy-setting and performance management rather than treating it as a periodic documentation exercise. Technology is what makes that embedding possible at scale.

"The shift from documentation to action is the defining challenge of modern enterprise risk management. Organizations that cannot move from risk identification to real-time response will find their frameworks decorative rather than functional." — COSO 2026 ERM Guidance commentary

When risk assessment technology is properly integrated, the operational differences are substantial:

- Real-time risk visibility replaces quarterly snapshots, giving CROs and board members current portfolio exposure rather than historical reporting

- Data-driven prioritization allows institutions to direct capital and operational resources toward the risks with the highest probability-adjusted impact

- Faster risk response compresses the time between identifying an emerging threat and adjusting controls, credit policies, or liquidity positions

- Scenario modeling at speed enables leadership to stress-test decisions against multiple risk environments before committing resources

The ERM and AI integration question is not whether to do it. It is how quickly you can move from intent to execution.

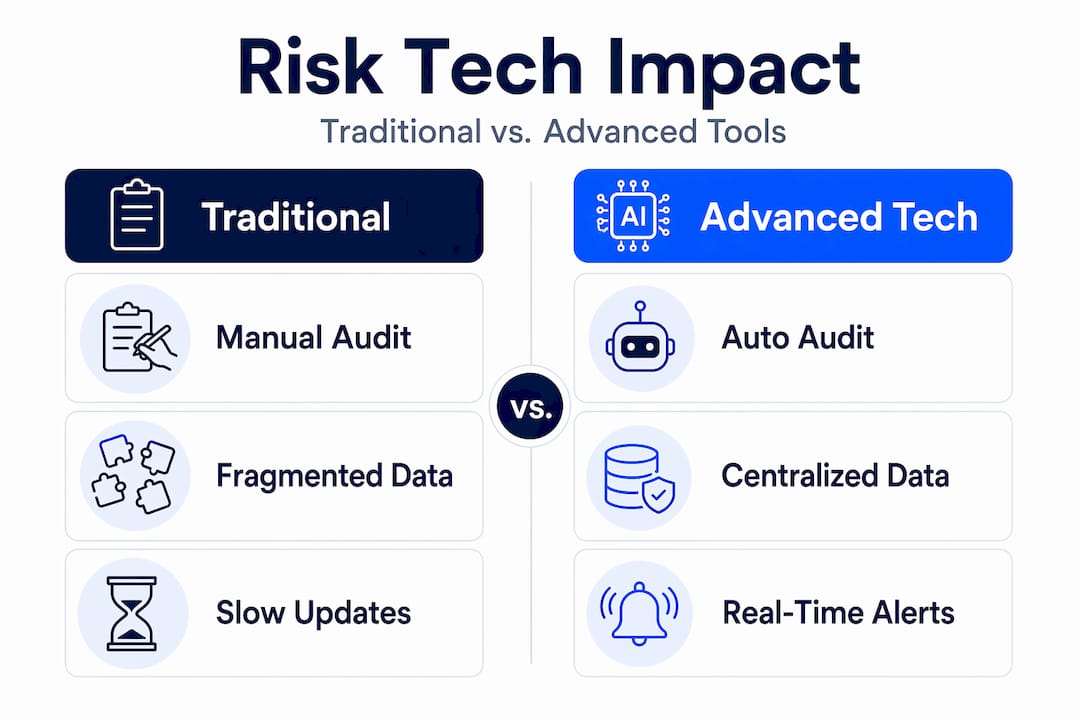

Concrete benefits of advanced risk management tools

The benefits of risk management tools are most convincing when grounded in specific, measurable outcomes rather than general claims. Here is what the data shows for institutions that have made the shift.

| Benefit | Traditional Approach | Technology-Enabled Approach |

|---|---|---|

| Audit preparation time | 2 to 4 weeks | Hours (automated evidence collection) |

| Risk assessment cycle | Monthly or quarterly | Continuous, real-time |

| Regulatory reporting | Manual compilation | Automated, audit-ready dashboards |

| Cross-departmental visibility | Siloed and inconsistent | Unified risk register across functions |

| Compliance cost trend | Rising with regulatory volume | Contained through automation |

Automation cuts ISO 27001 audit prep from weeks to hours, and institutions report 30 to 50 percent improvements in operational efficiency after deploying purpose-built risk platforms. These are not marginal gains.

Here is how the advantages compound in practice:

- Centralized risk visibility eliminates the version control problem that plagues spreadsheet-based programs. One authoritative risk register, accessible across departments, means assessors and executives are always working from the same data.

- Automated workflow management replaces manual follow-ups on control remediation, vendor assessments, and policy reviews with rule-based escalations that trigger without human intervention.

- Regulatory alignment becomes continuous rather than periodic. RegTech platforms with live rule updates keep pace with CFPB, FFIEC, and Basel requirements as they evolve, rather than waiting for annual policy reviews.

- Risk-based budgeting improves when risk data is quantified and comparable. Boards can see which risk domains carry the most exposure relative to control investment, enabling defensible capital allocation decisions.

Pro Tip: When evaluating risk technology platforms, require a demonstration of how the system handles a regulatory update workflow. This single test reveals whether the platform is truly designed for financial compliance or adapted from a generic risk tool.

The productivity improvements from risk tech also flow to customer experience. Faster, more accurate credit decisioning and reduced operational friction directly support the service quality that credit union members and community bank customers expect.

Practical guidance for implementing risk technology

Knowing why adopt risk technology is easier than knowing how to do it well. The most common failure mode is not technology selection. It is adoption. Well-maintained simple tools that teams consistently use outperform sophisticated enterprise platforms that generate low engagement and slow update cycles. This is a pattern that appears repeatedly across institutions of all sizes.

Effective implementation follows a predictable set of principles:

- Prioritize usability in the selection process. A risk platform that requires extensive training to run basic queries will not be used for daily decision support. Evaluate platforms on time-to-insight, not just feature depth.

- Establish governance before deploying tools. Technology does not solve ownership problems. Define who is responsible for each risk domain, how risk data flows across departments, and who has authority to act on findings before rolling out any platform.

- Use RegTech for regulatory currency. Distributed RegTech platforms provide continuously updated regulatory expertise at far lower cost than internal compliance systems built once and rarely updated. For community banks and credit unions operating without large compliance teams, this is a material advantage.

- Start with a focused scope. Attempting to automate every risk function simultaneously creates change management challenges that defeat even well-resourced programs. Choose one domain, credit risk, vendor management, or regulatory reporting, and build demonstrable value before expanding.

- Secure senior leadership sponsorship early. Automated risk management programs that lack executive visibility lose priority when operational pressure builds. CRO-level engagement is not optional; it is the deciding factor in sustained adoption.

Pro Tip: Build your risk technology roadmap in 90-day increments with defined success metrics at each stage. This gives leadership concrete evidence of progress and gives your team achievable milestones rather than a distant, abstract destination.

The balance between automation and human judgment also matters more than most vendors will tell you. CROs consistently emphasize that the goal is AI-assisted decision-making, not AI-replaced judgment, particularly in credit risk and regulatory interpretation where context and accountability remain human responsibilities.

My perspective: why this shift cannot wait

I've spent enough time talking with risk executives at community banks and credit unions to know that the compliance-checkbox mentality is deeply embedded, and not because those leaders don't understand the stakes. It's because the incentive structures inside most institutions reward avoiding findings on the last exam, not building for the next wave of risk. That's the real barrier technology has to overcome.

What I've seen work is when a CRO treats the technology investment as a capability argument rather than a cost argument. The institutions that moved early to automate risk assessment are not just saving time on audits. They are making fundamentally better credit and capital decisions because their risk data is current, clean, and comparable across portfolios. That's a competitive advantage that compounds.

The failure stories follow a consistent pattern too. An institution invests in an enterprise platform, underinvests in change management and training, and watches the platform become shelfware within 18 months. The lesson isn't that technology doesn't work. It's that technology adoption is a human problem as much as a technical one.

My honest take is that the institutions most at risk in the next three years are not those with gaps in their technology stack. They are the ones that have convinced themselves their current processes are adequate because they haven't experienced a major incident yet. Risk doesn't care about your incident history. It cares about your current controls.

— Raj

See how Riskinmind transforms risk operations

Riskinmind's AI-powered platform was built specifically for the risk challenges that credit unions, community banks, and lenders face every day. The platform's specialized AI agents handle regulatory compliance monitoring, credit risk assessment, and portfolio surveillance simultaneously, with real-time processing and response times under half a second. Rather than forcing your team to manage fragmented tools, Riskinmind centralizes risk visibility into a single dashboard with mobile access and automated reporting that keeps you audit-ready at all times.

For institutions evaluating where to start, the AI risk management platform covers the full spectrum from loan underwriting automation to enterprise portfolio risk monitoring. You can also review the platform pricing to find the right tier for your institution's size and risk function complexity. Riskinmind carries SOC 2® certification and bank-grade security, so the deployment conversation begins from a compliance-ready foundation.

FAQ

Why focus on risk technology over traditional methods?

Traditional risk management relies on periodic assessments and manual controls that cannot keep pace with real-time threat environments or the volume of regulatory change. Risk technology provides continuous monitoring, automated workflows, and data-driven decision support that manual processes cannot replicate at scale.

What is the biggest benefit of risk management tools for financial institutions?

The most immediate benefit is replacing fragmented, siloed risk data with a centralized, real-time view of portfolio exposure, which directly improves credit decisions, capital allocation, and regulatory readiness. Automation also cuts audit preparation from weeks to hours, delivering measurable cost efficiency.

How does risk technology improve decision-making for CROs?

Risk technology gives CROs current, quantified risk data rather than historical snapshots, enabling scenario modeling and faster escalation when thresholds are breached. 70% of banks are already testing AI in credit decisioning, reflecting how central technology has become to risk-informed strategy.

What should financial institutions prioritize when adopting risk technology?

Usability and governance structure should come before platform sophistication. A simple, consistently used tool with live regulatory updates delivers more value than a complex system with low adoption, and establishing clear risk ownership across departments before deployment is critical to sustained use.

How does AI change the risk technology equation for community banks?

AI enables community banks to process risk signals across loan portfolios, vendor relationships, and regulatory changes at a speed and depth that would otherwise require large dedicated teams. The key requirement is responsible AI governance, including explainability in credit decisions and clear accountability for model outputs.