Most financial professionals assume AI-powered underwriting is simply a faster version of what underwriters already do. That framing undersells the transformation and, more dangerously, sets institutions up to deploy AI in ways that add cost without adding value. Understanding what is AI-powered underwriting, in precise operational terms, means grasping how machine learning, natural language processing, and predictive analytics are restructuring how risk is identified, scored, and priced. This guide breaks down the mechanics, the measurable results, the real implementation challenges, and the workforce implications your team needs to understand before making any adoption decisions.

Table of Contents

- Key Takeaways

- What is AI-powered underwriting and how it works

- Measurable benefits of AI underwriting for financial institutions

- Implementation challenges you cannot ignore

- AI vs. traditional underwriting

- Practical guidance for implementing AI underwriting

- My take on where AI underwriting actually stands

- How Riskinmind supports AI-powered underwriting decisions

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| AI augments human underwriters | AI automates routine data extraction and scoring while human judgment handles complex, high-stakes decisions. |

| Speed and accuracy gains are measurable | Standard policies now move from days to minutes with over 99% accuracy using AI-driven risk assessment. |

| Verification Collapse is a real structural risk | AI systems that validate their own input data create systemic error exposure without independent verification layers. |

| Embedding beats bolt-on | AI integrated directly into underwriter workflows produces more value than separate decision-support tools. |

| Governance determines success | The biggest implementation failures come from organizational change issues, not technology limitations. |

What is AI-powered underwriting and how it works

AI-powered underwriting replaces rule-based, manually driven risk assessment with models that learn from large datasets, recognize complex patterns, and generate risk scores with a degree of consistency no human team can replicate at scale. The core technologies involved are machine learning algorithms, natural language processing (NLP), optical character recognition (OCR), and predictive analytics. Each plays a specific role in turning raw data into credit or insurance decisions.

Machine learning models train on historical loan performance data, claims records, and financial statements to identify variables that predict default, loss, or underperformance. NLP allows the system to extract meaning from unstructured sources: borrower narratives, medical records in life insurance applications, environmental impact reports in commercial real estate files. OCR handles document ingestion, converting scanned tax returns, bank statements, and appraisal reports into structured data fields the model can process. The result is a system that aggregates financial and claims data from sources that traditional rule engines would never touch, producing a more complete risk picture at every decision point.

The workflow shift is material. Where traditional underwriting required a human to manually pull data, apply static rules, and document a decision, automated underwriting with AI moves from document receipt to preliminary risk score in minutes. Straight-through processing handles standard, lower-complexity applications without human review at all. Complex files are flagged, enriched with AI-generated scenario analyses, and routed to senior underwriters who review context rather than collect it.

- Document ingestion and extraction: OCR and NLP parse application documents, financial statements, and third-party data feeds into structured inputs.

- Risk pattern recognition: ML models score applicants against patterns learned from thousands of historical cases, flagging anomalies a rules-based system would miss.

- Straight-through processing: Standard policies that fall within defined confidence thresholds clear without human intervention, freeing underwriters for judgment-intensive files.

- Real-time scenario modeling: In commercial real estate, AI generates underwriting in minutes by building live financial models and stress tests from ingested property data.

Pro Tip: Before selecting an AI underwriting platform, map your current workflow in granular detail. AI delivers its highest return when deployed against specific bottlenecks, not dropped over an entire process at once.

Measurable benefits of AI underwriting for financial institutions

The performance data from deployed AI underwriting systems is compelling, and it is concrete enough to support a business case. Standard policy decision times drop from days to 12.4 minutes with 99.3% accuracy. Commercial lines cycle times compress from two to three days down to one to two hours. These are not projections; they are reported outcomes from institutions that have moved beyond pilot stages.

The financial impact extends beyond speed. Institutions using agentic AI in underwriting report loss ratio improvements of three to five points. On a large commercial portfolio, three points of loss ratio improvement translates directly to millions of dollars in underwriting profit. Accuracy in risk pricing improves because the model draws on data sources, such as alternative financial records, behavioral signals, and third-party enrichment feeds, that no human underwriter could process within a standard review window.

| Metric | Traditional underwriting | AI-powered underwriting |

|---|---|---|

| Standard policy decision time | 3 to 5 days | 12.4 minutes |

| Commercial lines cycle time | 2 to 3 days | 1 to 2 hours |

| Risk assessment accuracy improvement | Baseline | Up to 43% improvement |

| Loss ratio impact | Baseline | 3 to 5 point improvement |

| Underwriting timeline reduction | Baseline | Up to 50% faster |

Operational efficiency data supports the financial case further. Among insurance executives who have deployed AI, 40% cite operational efficiency and 35% cite better use of complex data sources as their primary realized benefits. These are not soft gains. Fewer manual touchpoints, lower error rates on data entry, and faster decisioning create measurable cost reductions per policy processed and per loan file reviewed.

For credit unions and community banks, the implications for AI-driven risk assessment are particularly significant. Smaller institutions that cannot staff large underwriting teams gain the ability to process more volume without proportional headcount growth, which changes the unit economics of consumer and small business lending in ways that would have been structurally impossible five years ago.

Implementation challenges you cannot ignore

The business case for AI underwriting is real, but the path to realizing it is not straightforward. Three categories of risk deserve serious attention from decision-makers before any commitment to a platform.

The first is Verification Collapse. This is a structural condition where an AI underwriting system validates its own input data, creating a closed loop that cannot catch errors or fraud at the source. If the data feed the model consumes is compromised, the model's output is compromised, and nothing in the loop raises an alert. The mitigation requires building an independent verification layer that cross-validates multiple data sources before any underwriting decision is generated. This is not optional; it is the structural difference between a system that scales risk management and one that scales errors.

"The biggest failures in AI underwriting projects will stem from poor organizational change and governance, not technology limitations." — Hyperexponential Research

The second challenge is integration depth. Embedding AI directly into underwriter workflows), where pricing and risk assessment decisions actually get made, consistently outperforms deploying AI as a separate decision-support tool that underwriters consult on a second screen. Bolt-on implementations tend to be ignored under time pressure or used selectively, which undermines the consistency benefits that make AI underwriting valuable in the first place.

The third challenge is organizational. Governance structures, change management processes, and accountability frameworks need to exist before the technology goes live. Who owns a decision when AI generates the risk score? How do you audit model behavior for fair lending compliance? What review protocol applies when AI output conflicts with underwriter judgment? Institutions that answer these questions after deployment struggle; institutions that answer them before deployment tend to succeed.

Pro Tip: Treat your AI underwriting rollout as a governance project with a technology component, not a technology project that will eventually need governance. The sequencing matters more than most teams expect.

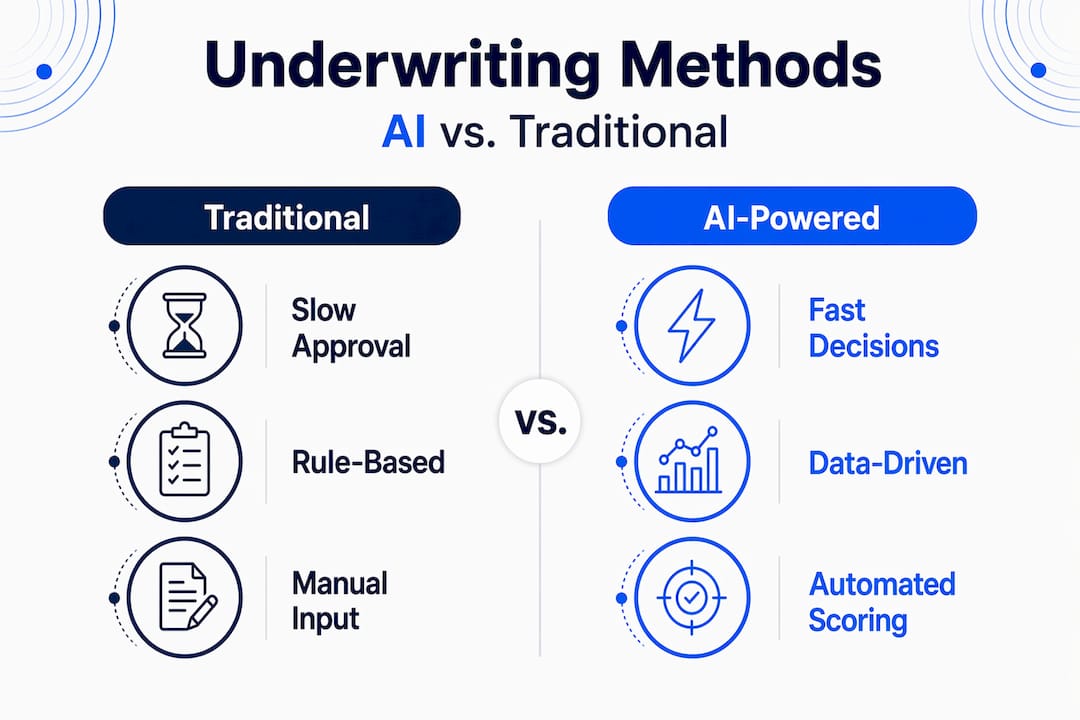

AI vs. traditional underwriting

Understanding the contrast between traditional and AI-enhanced underwriting helps decision-makers build realistic adoption strategies. Traditional underwriting depends on human analysts working through static rule sets, applying experience-based judgment to each file. The process is consistent within a single underwriter's portfolio but highly variable across a team, especially as file complexity increases and bandwidth constraints force prioritization.

AI-powered underwriting replaces that variability with model consistency. Every file gets scored against the same variables, with the same weighting, at the same depth of data analysis, regardless of what else is in the queue. That consistency is itself a risk management asset.

The role of human underwriters does not disappear in an AI-enhanced model. It restructures. Workforce roles shift away from manual data collection and initial risk sorting toward strategic risk analysis, portfolio oversight, exception handling, and relationship management. Senior underwriters become decision validators and complex-case specialists rather than processors of standard applications. This is a meaningful upgrade for experienced professionals, though it requires deliberate planning for roles in the mid-tier of the skills distribution.

- Processing consistency: AI applies identical criteria across every application; human review varies with workload and experience.

- Data volume handled: AI ingests and analyzes structured and unstructured data at scale; manual review is bounded by human capacity.

- Decision speed: AI scores standard files in minutes; manual workflows require days even for straightforward applications.

- Regulatory auditability: AI models produce traceable, logged decision factors; manual decisions rely on underwriter documentation quality.

- Complex judgment: Human underwriters retain an advantage in novel risk scenarios where model training data is thin or market conditions are shifting rapidly.

The institutions that will capture the most value from this transition are those that deploy AI for the high-volume, pattern-recognizable portion of their portfolio and preserve human expertise for the tail risk and relationship-driven cases where contextual judgment is irreplaceable.

Practical guidance for implementing AI underwriting

Deploying AI underwriting successfully comes down to execution discipline across four areas, each of which requires deliberate attention rather than assumption.

-

Embed AI in existing workflows. Position AI models inside the tools your underwriting team already uses, not alongside them. If your team prices risk in a loan origination system, the AI-generated score and supporting data context should surface there, not in a separate application. The value of workflow-embedded AI) is that it shapes decisions at the moment they are made rather than being consulted after the fact.

-

Build a Truth Protocol from day one. Establish an independent data validation layer that cross-verifies applicant-provided data against third-party sources before the AI model scores the file. A Truth Protocol approach is the primary defense against Verification Collapse and should be treated as a foundational architecture requirement, not an add-on.

-

Develop your workforce in parallel with your technology. AI adoption without workforce development creates a skills gap that undermines the technology's effectiveness. Identify which roles will shift toward model oversight, exception review, and strategic portfolio analysis, and build training programs around those transitions. The institutions that get this right are developing what industry observers describe as "financial results steward" roles that combine human judgment with data interpretation skills.

-

Establish model governance protocols. Define how model performance is monitored, when recalibration is triggered, and who holds accountability for model-generated decisions under fair lending and credit risk frameworks. Connect your AI monitoring to automated risk assessment governance processes so compliance obligations are met without manual reconciliation after the fact.

-

Choose technology partners aligned with regulatory requirements. For credit unions, community banks, and lenders operating under specific regulatory frameworks, your AI underwriting platform must support auditability, data residency requirements, and fair lending analysis. Evaluate partners on security certifications and compliance infrastructure alongside model performance metrics.

Pro Tip: Run a shadow-scoring pilot before full deployment. Let the AI model score files in parallel with your existing process for 60 to 90 days, then compare outcomes. The divergence data will reveal both where the model adds clear value and where it needs recalibration before going live.

My take on where AI underwriting actually stands

I've observed enough AI underwriting implementations to know that the most common failure mode has nothing to do with the model architecture. Organizations invest in sophisticated technology, get through the integration work, and then watch adoption stall because underwriters don't trust what they can't see inside. The explainability problem is real, and it is primarily a change management challenge, not a technical one.

What I've learned is that the institutions making the most progress are the ones that treat AI output as a starting point for the underwriter's conversation, not as a verdict. When a model surfaces a risk flag, the underwriter who understands why that flag matters and has the data context to validate or override it is genuinely more effective than one working from intuition alone. That is the productive relationship between human expertise and machine consistency.

The forward view concerns me slightly in one respect. Top-quartile carriers will reduce underwriting touchpoints significantly by 2028) by embedding AI deeply, and the institutions that delay integration now will face a compounding gap that becomes structurally difficult to close. AI in underwriting is not a long-term strategic consideration anymore. It is a near-term operational decision with compounding consequences.

The organizations I've seen get this right share one common characteristic: they treat AI risk management best practices as core institutional discipline rather than a technology department initiative. That framing changes everything about how the rollout proceeds.

— Raj

How Riskinmind supports AI-powered underwriting decisions

Riskinmind builds AI risk management infrastructure specifically for credit unions, community banks, and lenders that need more than a generic analytics platform. The platform's AI agents, working under the coordination of Ava, cover credit risk assessment, regulatory compliance, and portfolio monitoring in an integrated architecture that embeds directly into your existing workflows rather than operating as a separate system.

For loan underwriting, Riskinmind's David AI Loan Assessor processes credit applications with real-time risk scoring, giving your underwriting team structured intelligence at the point of decision rather than after the file has moved through a separate review queue. The CRE Loan Risk Predictor applies the same architecture to commercial real estate portfolios, generating financial models and stress tests from ingested property data in minutes. Both tools operate within Riskinmind's SOC 2® certified, bank-grade security environment, with sub-half-second response times. If your institution is evaluating AI underwriting solutions with genuine workflow integration and compliance infrastructure built in, Riskinmind's platform is worth a closer look.

FAQ

What is AI-powered underwriting in simple terms?

AI-powered underwriting uses machine learning, natural language processing, and predictive analytics to automate risk assessment, data extraction, and credit or insurance decisioning. It replaces manual, rule-based processes with models that learn from historical data and score risk with greater speed and consistency.

How does AI underwriting improve on traditional methods?

AI underwriting processes structured and unstructured data at scale, reduces standard policy decision times from days to minutes, and applies consistent scoring criteria across every application. Traditional methods are limited by human bandwidth, static rule sets, and variable documentation quality.

What is the Verification Collapse risk in AI underwriting?

Verification Collapse occurs when an AI underwriting system validates its own input data, creating a closed loop that cannot detect errors or fraud at the source. Independent verification layers that cross-validate multiple data sources before generating a decision are required to prevent this structural risk.

Does AI underwriting replace human underwriters?

No. AI augments underwriters by automating routine data tasks and standard-file processing, freeing experienced professionals to focus on complex risk analysis, exception handling, and portfolio strategy. The role evolves rather than disappears.

What adoption rates has AI reached in insurance underwriting?

Nearly 50% of insurance executives have incorporated AI into underwriting, with 20% reporting full workflow integration, 24% using it as decision support, and 38% in active pilot programs as of the most recent industry survey data.