Financial institutions are deploying AI at a pace that their governance structures have not yet matched, and the role of AI director in risk is becoming the linchpin that holds accountability together. 76% of organizations now have a Chief AI Officer in place as of 2026, up from just 26% a year prior, yet formal governance authority remains rare. For credit union executives, CROs, and risk officers navigating this gap, understanding what an AI director actually does, and where this role fits within your enterprise risk framework, is no longer optional.

Table of Contents

- Key takeaways

- Defining the role of AI director in risk governance

- Core components of AI governance frameworks

- AI risk challenges unique to financial institutions

- Practical steps for AI directors to strengthen risk management

- My perspective on what most AI directors get wrong

- How Riskinmind supports AI directors in financial institutions

- FAQ

Key takeaways

| Point | Details |

|---|---|

| AI governance gap is real | Only 18% of organizations have an enterprise-wide AI governance body with actual decision authority. |

| AI directors span functions | The role requires coordination across compliance, legal, credit risk, and technology units simultaneously. |

| Traditional MRM is not enough | SR 11-7 frameworks must be expanded with ethics, data governance, and third-party risk components. |

| Real-time monitoring is required | Quarterly validation cycles are insufficient for AI models that drift rapidly in production. |

| Dynamic controls outperform checklists | Risk-tier based validation prevents governance bottlenecks without slowing the pace of innovation. |

Defining the role of AI director in risk governance

The AI director in a financial institution is not simply a technology officer with a new title. This role sits at the intersection of enterprise risk management, regulatory compliance, and AI strategy, with accountability that runs in all three directions at once. Where a Chief Technology Officer focuses on capability and infrastructure, the AI director focuses on how AI systems affect the institution's risk profile, its regulatory standing, and its obligations to customers.

In practice, AI director responsibilities cover four broad areas. First, strategy: setting the institution's AI risk appetite and aligning AI deployment decisions with overall enterprise risk tolerance. Second, oversight: reviewing AI model inventories, validating governance documentation, and confirming that materiality thresholds are applied consistently. Third, accountability: serving as the named officer responsible when regulators ask who owns the AI risk framework. Fourth, cross-functional coordination: working continuously with compliance, legal, model risk management, and individual business line risk owners to keep AI governance from becoming a siloed function.

What makes this role particularly demanding is the technical fluency required alongside the risk and regulatory knowledge. An AI director who cannot distinguish between a gradient-boosted model and a large language model will struggle to set appropriate validation standards for each. At the same time, a role focused purely on technology without deep grounding in credit risk, fair lending obligations, and SR 11-7 principles will produce governance frameworks that look complete on paper but fail under examination.

- Own the institution's AI model inventory and risk classification system

- Set validation standards differentiated by model type, use case, and risk tier

- Chair or co-chair the AI governance committee with formal charter authority

- Brief the board on material AI risks, including documented case examples of AI failures

- Manage relationships with third-party AI vendors and review their risk disclosures

The role also requires building culture, not just policy. An AI director who treats governance as a compliance checkbox will find that business units route around it. The most effective AI directors position governance as an enabler of speed, because clear risk classification and pre-approved validation pathways let teams deploy lower-risk models faster.

Pro Tip: Position your AI governance framework as a tiered approval process rather than a universal gate. Low-risk models with narrow, well-documented use cases should move through validation in days, not months. Reserve intensive review for high-risk applications like credit decisioning and fraud detection where regulatory exposure is material.

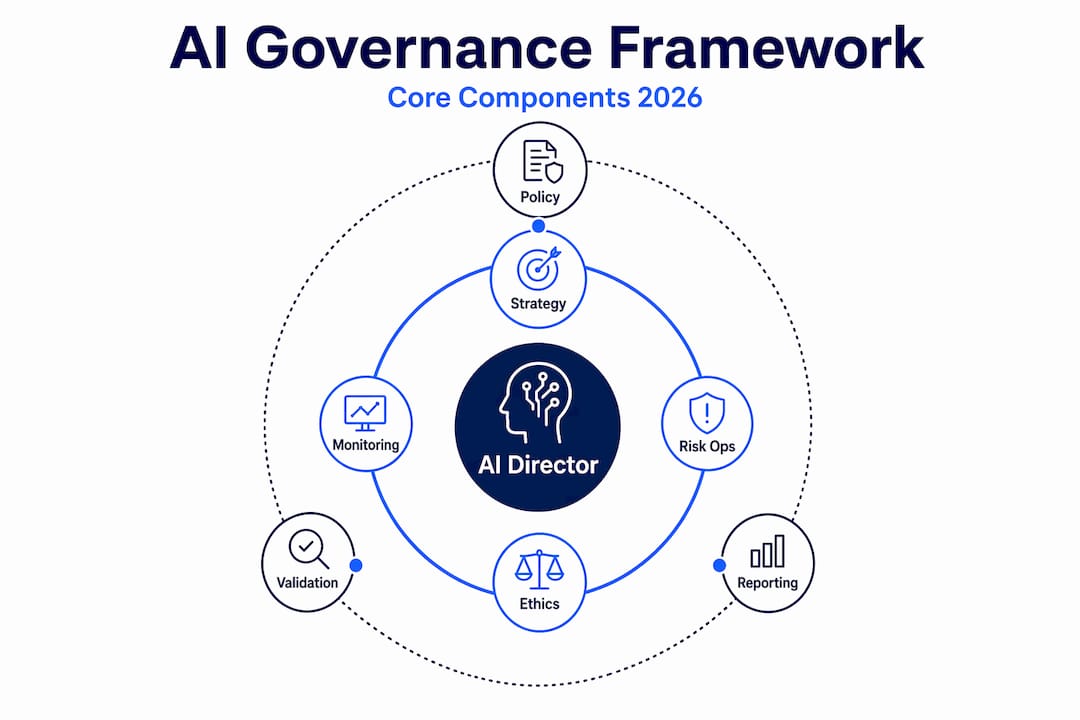

Core components of AI governance frameworks

AI governance connects strategy with risk management by defining clear responsibilities, decision rights, and escalation processes. For financial institutions, a functioning AI governance framework typically includes four structural components: an organizational structure with named roles and authorities, written policies covering the full AI lifecycle, a governance committee with a formal charter, and a set of controls that are calibrated to risk rather than applied uniformly.

The table below compares the coverage of traditional Model Risk Management under SR 11-7 against what a broader AI governance framework must address.

| Governance dimension | SR 11-7 MRM coverage | AI governance framework requirement |

|---|---|---|

| Model validation | Covered | Covered, plus continuous automated monitoring |

| Fairness and bias | Not addressed | Required, with documented fairness testing |

| Ethics review | Not addressed | Formal ethics lead role and review process |

| Third-party AI vendor risk | Partial | Explicit vendor risk assessment and contractual controls |

| Data governance | Partial | Full lineage, quality, and privacy requirements |

| Regulatory compliance (EU AI Act) | Not addressed | Required for cross-border or high-risk AI systems |

MRM frameworks are necessary but insufficient on their own. The SR 11-7 model lifecycle covers development, validation, and use, but it was not designed to address algorithmic bias, the opacity of deep learning models, or the ethical implications of automated credit decisions. AI directors must build on that foundation rather than replace it.

Governance committees require particular attention to composition. Effective AI governance demands cross-functional committees with formal charters that include a committee chair, an AI ethics lead, a data governance representative, and model risk owners from the business lines most exposed to AI. Without these roles formally assigned, accountability diffuses and decisions stall.

On the regulatory side, full compliance for high-risk AI systems under the EU AI Act is now extended to December 2, 2027, giving institutions additional time to align their governance frameworks. That extension should not be read as an invitation to delay. Institutions that treat the additional runway as preparation time rather than relief will be better positioned when regulators in the U.S. adopt analogous standards, which most observers expect within the same timeframe.

Pro Tip: Integrate your AI governance framework directly into your existing GRC platform rather than building a parallel system. AI governance integration with GRC platforms produces auditable, immutable records of risk assessments and control execution, exactly what regulators will request during examination.

AI risk challenges unique to financial institutions

The challenges AI directors face in financial institutions differ from those in other industries in ways that matter for how governance frameworks are designed. Credit decisions, fraud detection, and liquidity modeling are not just high-stakes; they are regulated activities where model failures carry legal consequences under the Equal Credit Opportunity Act, the Fair Housing Act, and various state-level analogs.

The most significant divergence from traditional model risk management is the monitoring requirement. Quarterly or annual validation cycles are insufficient for AI models in production, particularly machine learning models that respond to shifting data distributions. A credit scoring model trained on pre-2024 data may behave differently as delinquency patterns evolve, and that drift may not surface until it has already produced materially biased or inaccurate outputs. AI directors must implement near-real-time monitoring that tracks model performance, fairness segmentations, and data quality on a continuous basis.

Third-party AI vendor risk compounds this challenge. Many community banks and credit unions are deploying AI through fintech partnerships rather than building models internally. This creates a governance gap: the institution bears the regulatory risk, but the model documentation, training data, and validation records reside with the vendor. AI directors must negotiate contractual access to model documentation, mandate third-party audits for material models, and classify vendor-provided AI under the same risk tiers as internally developed models.

Additional AI-specific risk categories that AI directors must address include:

- Model opacity: Deep learning and LLM-based systems often cannot produce explanations that satisfy adverse action notice requirements under Regulation B.

- Data quality and lineage: AI models amplify data problems rather than absorbing them; a biased training dataset produces systematically biased outputs at scale.

- Scope creep: Models approved for one use case are sometimes extended to adjacent applications without re-validation, creating unmanaged risk exposure.

- Rapid iteration cycles: Development teams operating under agile methodologies may push model updates faster than governance review cycles can process them.

Only 18% of organizations have an enterprise-wide AI governance body with genuine decision authority, which means the vast majority of financial institutions are managing these risks through ad hoc structures. The AI director role exists precisely to change that reality.

Practical steps for AI directors to strengthen risk management

Translating governance theory into daily practice requires a structured approach that scales without creating bottlenecks. The following steps represent a progression from foundational infrastructure through ongoing operational discipline.

-

Build an interdisciplinary governance team. No single function owns all the expertise required for AI risk management. The AI director should convene a standing team that includes credit risk, compliance, legal, IT security, and at least one business line representative. This team defines standards collectively and shares accountability for outcomes.

-

Establish a risk classification and materiality threshold system. Not every AI model carries the same risk. A document summarization tool used internally carries different implications than an automated credit decisioning model. Tiering models by risk level, materiality, and regulatory exposure allows the AI director to allocate validation resources where they matter most.

-

Implement continuous, automated monitoring. Continuous monitoring powered by automation should track performance metrics, fairness segmentations, and prompt auditing for LLMs on an ongoing basis. This is not a luxury for large institutions only. Even community banks running vendor-provided AI tools need dashboard visibility into model behavior.

-

Deliver substantive board briefings. Boards need briefings on AI risks that go beyond technical summaries, including documented case examples of AI failures at other institutions and clear articulation of the institution's current risk exposure. Board literacy on AI is a governance obligation, and the AI director owns it.

-

Align governance milestones with compliance deadlines. With the EU AI Act timeline now set and U.S. regulatory guidance continuing to evolve, AI directors should map their internal governance milestones to external compliance requirements. This alignment also makes the business case for governance investment more concrete when presenting to senior leadership.

Consider a concrete illustration: a credit union deploying a vendor-provided AI underwriting tool discovers, through continuous fairness monitoring, that approval rates for a demographic segment have declined materially over six months with no corresponding change in credit quality indicators. An AI director with a functional governance framework detects this through automated alerts, initiates a formal review, and engages the vendor under existing contractual audit rights, all before the pattern produces a regulatory examination finding. That is AI risk management working as designed.

Pro Tip: When briefing your board, lead with the business consequence of an AI failure, not the technical mechanism. A board that understands what a biased underwriting model costs in litigation, regulatory fines, and reputational exposure will support governance investment far more readily than one presented with model architecture diagrams.

For institutions examining AI risk management strategies in depth, understanding how the AI director role interacts with board oversight structures is one of the most consequential decisions a financial institution can make.

My perspective on what most AI directors get wrong

I've spent a significant amount of time working through AI governance questions with financial institutions of varying sizes, and what I consistently observe is a version of the same mistake: AI directors who treat governance as a compliance function rather than a risk function.

The distinction matters more than it sounds. Compliance asks "are we following the rules?" Risk asks "what could go wrong, and how bad would it be?" When AI governance is positioned as a compliance exercise, it produces documentation that satisfies an examiner but does not protect the institution from the failure modes that actually cause harm.

The uncomfortable truth is that AI governance transparency and calibrated controls are not self-executing. You can publish all the right policies, assign all the right roles, and still have a governance framework that fails because business units don't believe it serves their interests. The AI directors I've seen succeed are the ones who make governance faster for low-risk use cases while being genuinely rigorous for high-risk ones. That trade creates buy-in.

I've also found that AI directors underestimate how quickly their own technical knowledge needs to evolve. LLMs, agentic AI systems, and multimodal models present governance challenges that didn't exist when most current model risk frameworks were written. Continuous learning isn't a professional development aspiration for this role. It's a core job requirement. The institutions that build AI leadership capable of growing alongside the technology will earn regulatory trust. The ones that don't will spend the next decade catching up.

— Raj

How Riskinmind supports AI directors in financial institutions

Riskinmind's AI-powered risk management platform is built for exactly the governance and monitoring challenges that AI directors in community banks, credit unions, and lenders face daily. The platform's suite of specialized AI agents, coordinated by a central AI director named Ava, provides real-time oversight across credit risk, regulatory compliance, and portfolio monitoring, with response times under half a second and SOC 2® certified security. Tools like the AI Loan Assessor and the CRE Loan Risk Predictor give AI directors the model-level insight they need to classify risk, monitor performance, and satisfy board reporting requirements without building infrastructure from scratch. Explore the platform and view pricing options to find the configuration that matches your institution's risk profile.

FAQ

What is the primary role of an AI director in risk management?

The AI director is responsible for setting AI risk strategy, overseeing the AI model inventory, chairing governance committees, and serving as the named accountability point for AI-related risk within the enterprise risk framework.

How does the AI director role differ from traditional model risk management?

Traditional MRM under SR 11-7 addresses the model lifecycle but does not cover fairness testing, ethics review, or third-party vendor risk. The AI director role expands that scope to address the full range of AI-specific risks in financial institutions.

Why is real-time monitoring required for AI models?

AI models can drift rapidly as underlying data distributions shift, meaning quarterly validation cycles may miss material changes in model behavior. Continuous automated monitoring tracks performance, fairness, and data quality on an ongoing basis.

What governance structures does an AI director need to establish?

An AI director needs a formal governance committee with a charter, a tiered risk classification system for AI models, written policies covering the full AI lifecycle, and integration with the institution's existing GRC platform to produce auditable records.

How should an AI director approach board reporting on AI risk?

Board briefings on AI risk should focus on business consequences rather than technical mechanisms, and should include case examples of AI failures at peer institutions to build board literacy and support governance investment.