Credit risk professionals at community banks and credit unions are under more pressure than ever before, facing rising delinquencies, tightening regulatory scrutiny, and a competitive landscape that demands faster, more defensible lending decisions. Legacy evaluation methods built on paper-based analysis and basic scoring models simply cannot keep pace with today's credit environment, where the volume, velocity, and complexity of loan applications demand a more rigorous approach. This guide decodes the full risk assessment process, from foundational frameworks and supervisory rating scales to machine learning performance benchmarks and hybrid decisioning models, giving your institution the clarity and tools needed to build smarter, more compliant lending practices.

Table of Contents

- Defining risk assessment in lending

- Key frameworks: From the Five Cs to advanced models

- How machine learning is transforming lending risk assessment

- Hybrid approaches: When expert judgment matters most

- Supervisory ratings and regulatory expectations

- Why the best lending risk assessments combine AI with expert oversight

- Power your risk assessment with intelligent AI solutions

- Frequently asked questions

Automate Regulatory Model Risk Governance

Examine models against 32 qualitative criteria and resolve risk Tiers with pre-deployment checklists per OCC 2011-12 guidelines.

Key Takeaways

| Point | Details |

|---|---|

| Risk assessment basics | Lending risk assessment systematically evaluates and controls credit risk to support safe, compliant lending. |

| Framework variety | Modern risk assessment blends traditional factors, statistical models, and loss forecasting methods for robust analysis. |

| AI advantages | Machine learning dramatically improves predictive accuracy, enabling faster, smarter credit decisions for lenders. |

| Need for hybrid models | Even advanced AI solutions rely on expert human judgment for regulatory compliance and edge case handling. |

| Regulatory alignment | Supervisory ratings and explainable models ensure that risk management meets or exceeds regulatory expectations. |

Defining risk assessment in lending

With the context set on why risk assessment needs to evolve, let's clarify exactly what this process entails and why each step is essential for modern lending teams.

At its core, risk assessment in lending is the process of identifying, measuring, evaluating, monitoring, reporting, and controlling credit risk in lending activities to ensure sound credit-granting practices. This Basel Committee definition is not abstract: it maps directly to the workflows your credit analysts, loan officers, and compliance officers execute every single day. Each element of that definition carries weight in a regulated environment, and ignoring any one of them creates gaps that examiners will find.

The core components of a sound lending risk assessment framework include:

- Risk identification: Recognizing the borrower characteristics, industry exposures, collateral types, and macroeconomic conditions that introduce credit risk into the portfolio.

- Measurement: Applying both quantitative analysis (probability of default, loss given default, exposure at default) and qualitative judgment (management quality, competitive position) to size potential losses.

- Ongoing monitoring: Tracking loan performance, covenant compliance, and borrower financial condition between origination and maturity.

- Controls: Implementing credit policies, concentration limits, approval thresholds, and exception tracking to prevent excessive risk accumulation.

- Reporting: Producing timely, accurate reports for senior management, the board, and examiners to support governance and supervisory requirements.

Governance sits at the center of all five components. Board-approved credit risk appetite statements set the direction; senior management translates strategy into underwriting standards and portfolio monitoring programs. Robust management information systems are not optional. Without reliable data pipelines and reporting infrastructure, even the best frameworks collapse under the weight of portfolio growth. Exploring the full range of methods and models for financial risk assessment can give your team a stronger foundation for building these systems correctly.

"Sound credit risk management involves identifying, measuring, monitoring, and controlling credit risk as well as determining that capital is adequate to compensate for the risk taken." — Basel Committee on Banking Supervision

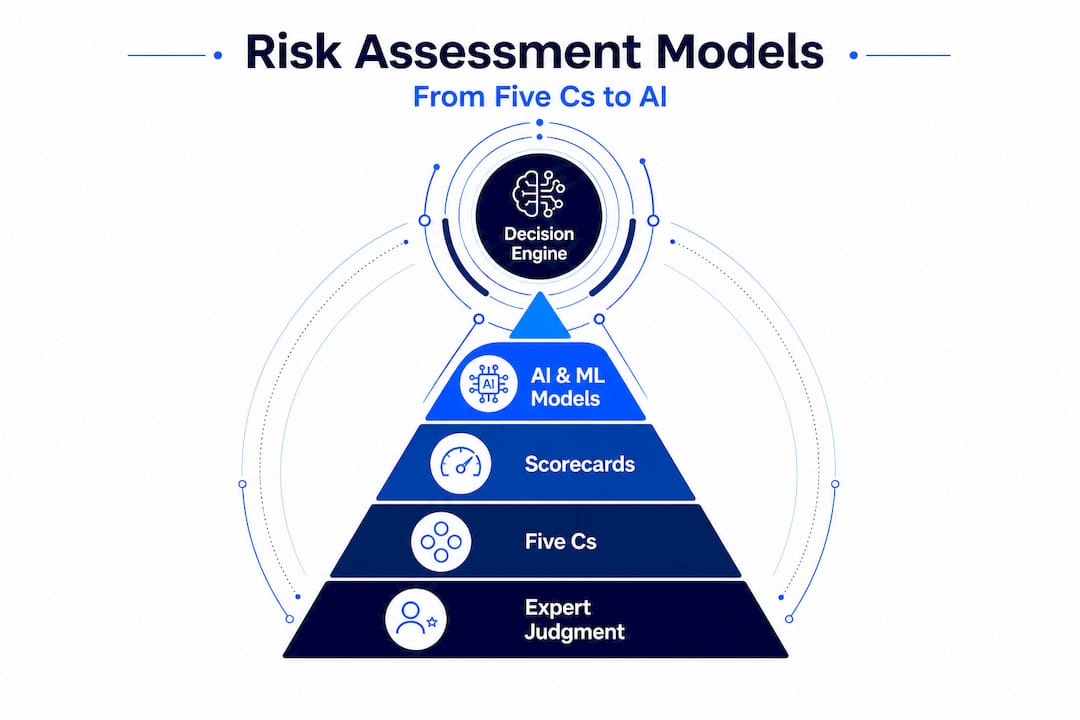

Key frameworks: From the Five Cs to advanced models

Now that the pieces of the risk assessment puzzle are clear, let's examine how different methodologies, old and new, fit together and what they offer lending institutions today.

Key methodologies span a wide range, from the qualitative Five Cs of Credit (character, capacity, capital, collateral, and conditions) to internal risk rating systems, scorecards, expected loss models using probability of default (PD), exposure at default (EAD), and loss given default (LGD), and for community banks implementing CECL, the Weighted Average Remaining Maturity (WARM) method, roll-rate analysis, and discounted cash flow modeling.

| Framework | Core criteria | Primary strengths | Regulatory fit |

|---|---|---|---|

| Five Cs of Credit | Qualitative borrower attributes | Holistic, relationship-based | Strong for smaller institutions |

| Internal scorecards | Weighted financial ratios | Consistent, auditable | Supports risk rating systems |

| PD/EAD/LGD models | Statistical default probability | Quantitative rigor, Basel alignment | Required for IRB approaches |

| WARM/CECL methods | Loss estimates over remaining life | Forward-looking allowance | FASB ASC 326 compliance |

Integrating these approaches does not happen automatically. Here is a practical, stepwise path for blending legacy and statistical frameworks without disrupting your existing workflows:

- Map your current rating system to identify where qualitative overrides are most frequent and where scorecard inputs have the most predictive power.

- Validate statistical models against historical loss data before expanding their role in credit decisions.

- Establish override governance so that when expert judgment departs from model output, the rationale is documented, reviewed, and tracked.

- Pilot hybrid reviews on a defined portfolio segment before full deployment across loan types.

- Integrate model outputs into board reporting so that risk appetite alignment is visible at the governance level.

Small community banks can blend expert judgment with model-driven methods without abandoning the relationship-based approach that distinguishes them. The key is not to replace intuition but to anchor it in data. Modern approaches to credit risk modeling show how institutions of all sizes are achieving this balance. For commercial real estate portfolios specifically, tools like the CRE loan risk predictor can sharpen quantitative assessments significantly.

Pro Tip: Prioritize transparency and interpretability in every model you deploy. Examiners and internal auditors need to follow the logic of a credit decision from input to output, and "the model said so" is not an acceptable audit trail for any loan above your materiality threshold.

How machine learning is transforming lending risk assessment

With established frameworks as a foundation, leaders are now exploring how machine learning and AI models are reshaping risk assessment for superior accuracy and process automation.

The performance data is compelling. XGBoost outperforms logistic regression on credit default prediction tasks: in a study using a 1.2 million record Turkish loan dataset with a 3.3% default rate, XGBoost with oversampling achieved an ROC-AUC of 0.914 compared to 0.865 for logistic regression. That differential is not academic. At scale, a difference of 5 percentage points in ROC-AUC can translate to materially fewer misclassified high-risk loans, reducing charge-offs and protecting net interest margin.

| Model | ROC-AUC score | Approach | Relative performance |

|---|---|---|---|

| XGBoost (with oversampling) | 0.914 | Ensemble, gradient boosting | Highest |

| Random forest | ~0.895 | Ensemble, bagging | Strong |

| Logistic regression | 0.865 | Linear, traditional | Baseline |

| Naive Bayes | ~0.840 | Probabilistic | Below baseline |

The challenge is not just performance. AI interpretability is a compliance requirement, particularly under ECOA and Regulation B, which mandate that institutions provide specific adverse action reasons to declined applicants. A black-box gradient boosting model that cannot generate plain-language declination reasons creates regulatory exposure regardless of its predictive accuracy. Hybrids are strongly recommended for regulated lending, pairing model-driven risk scoring with rules-based explanations or post-hoc explainability layers.

Common pitfalls include deploying ML models trained on unrepresentative historical data, failing to monitor for model drift as economic conditions change, and underinvesting in the documentation that regulators expect to see during model risk management exams. AI also enables scalable portfolio-level assessments that were not feasible with analyst-driven methods: running stress scenarios across thousands of loans simultaneously, flagging emerging concentrations before they breach policy limits, and automating routine covenant tracking.

Deeper reading on ML in credit assessment and how machine learning strengthens financial risk assessment provides additional context for institutions at various stages of AI adoption.

Pro Tip: Use model explainability tools such as SHAP (SHapley Additive exPlanations) values to generate feature-level contribution scores for each credit decision. These outputs can be mapped to adverse action notice templates, bridging the gap between AI accuracy and compliance documentation without requiring a full model rebuild.

Hybrid approaches: When expert judgment matters most

While machine learning brings accuracy and efficiency, certain risk scenarios defy full automation. Let's outline when and how expert judgment re-enters the picture.

Hybrid decision models combine algorithmic scoring with structured human review at defined decision points. In regulated lending, this is not a design choice; it is often a regulatory requirement. Edge cases requiring manual review include scenarios like GDPR-triggered regulatory manual reviews, fraud detection and correction notices, high credit utilization above 70%, subprime borrowers with scores below 620, and portfolio concentrations in declining industries. Each of these triggers represents a situation where statistical pattern recognition may be inadequate or where the stakes of an incorrect decision are high enough that human accountability is essential.

Typical edge-case scenarios where fully automated decisioning falls short include:

- Fraud and identity verification: Sophisticated fraud patterns may mimic legitimate borrower profiles closely enough to fool models trained on historical clean data.

- Complex collateral valuations: Commercial real estate or specialized assets require appraisal expertise that cannot be reduced to input variables.

- Borrower disputes and corrections: FCRA-related disputes require human review of the underlying facts, not just a model rerun with updated inputs.

- Concentration risk triggers: When a credit decision would push sectoral or geographic exposure past policy limits, a committee review is almost universally required by sound credit policy.

- New-to-credit or thin-file applicants: Insufficient credit history produces high model uncertainty, which demands qualitative judgment to supplement quantitative gaps.

"Hybrid human-AI models are increasingly recognized as the appropriate standard for regulated lending, where accountability, explainability, and governance cannot be delegated to an algorithm alone."

Practically, escalation protocols should be built directly into your loan origination system workflow. When a model produces a score in a defined uncertainty band or flags a specific risk attribute, the file routes automatically to a senior credit analyst or committee. That escalation, its rationale, and the outcome must all be captured in the audit trail. Exploring AI risk best practices and advanced AI risk tools can help institutions structure these workflows effectively. For a broader strategic view, essential AI-driven risk management insights provides additional perspective on integrating automation with accountability.

Supervisory ratings and regulatory expectations

Understanding hybrid assessments in context, it's vital to also consider how external supervisory scrutiny and asset quality ratings shape internal practices.

The FDIC and NCUA both use a 1-5 asset quality rating scale to assess the credit risk profile of the institutions they supervise. These ratings directly influence examination frequency, enforcement actions, and capital planning conversations with your primary regulator.

| Rating | Asset quality descriptor | Supervisory implication |

|---|---|---|

| 1 | Strong, minimal credit concerns | Minimal oversight, infrequent examination |

| 2 | Satisfactory, limited weaknesses | Standard examination cycle |

| 3 | Less than satisfactory, material weaknesses | Increased monitoring, formal supervisory attention |

| 4 | Deficient, significant risk of loss | Formal action likely, corrective plans required |

| 5 | Critically deficient, imminent threat | Immediate corrective action, potential enforcement |

Several factors move institutions toward lower (worse) ratings: rapid loan growth without commensurate underwriting controls, high classified asset ratios, inadequate allowance coverage, weak credit administration practices, and poor exception management. Conversely, institutions with strong credit policies, proactive problem loan identification, conservative concentration management, and robust internal audit functions consistently maintain ratings of 1 or 2.

Best practices for aligning your risk assessment process with regulatory expectations include:

- Document credit policy exceptions with full approval chains so examiners can see the decision logic rather than just the outcome.

- Maintain a forward-looking allowance using CECL methodology, updated with current economic scenarios rather than historical averages alone.

- Conduct periodic internal loan reviews that mirror examiner methodology, including criticized and classified asset identification.

- Track and trend delinquency metrics by portfolio segment, flagging deterioration to the board before it reaches examiner attention.

- Use AI-driven portfolio analytics to identify emerging concentrations and risk outliers before they appear on the examiner's classified list.

AI-driven insights can directly support better supervisory ratings by enabling proactive portfolio surveillance: flagging covenant breaches as they occur, generating real-time concentration reports, and automating exam preparation workflows so credit administration teams spend less time compiling data and more time addressing issues.

Why the best lending risk assessments combine AI with expert oversight

Pulling together all aspects, from regulatory supervision to analytics and human expertise, here is our perspective on why integrated, hybrid risk assessment workflows are the only defensible standard for forward-thinking institutions.

The institutions that struggle most with AI adoption are not the ones that lack technology. They are the ones that treated AI as a cost-cutting substitute for experienced credit judgment rather than a force multiplier for it. Most failed implementations share a common pattern: the model is deployed, the team is not retrained, documentation of subjective overlays is not standardized, and when the first regulatory inquiry arrives, no one can explain why the model output was accepted in one case and overridden in another.

The real competitive differentiator is not the algorithm. It is the workflow architecture around the algorithm. Institutions that invest in training credit staff to interpret model outputs, establishing clear escalation criteria, and embedding AI scores into board-level reporting are the ones that emerge from exams with clean ratings and the confidence to grow their portfolios. How AI empowers credit union growth offers a concrete look at this dynamic in practice.

Interpretability, regulatory accountability, and ethical lending requirements will not diminish as AI capabilities improve. They will intensify. The institutions building hybrid frameworks today, where AI improves speed and accuracy while human oversight provides accountability and context, are creating a structural compliance advantage that purely manual or purely automated approaches simply cannot match. Risk does not live in a model. It lives in portfolios, decisions, and the people accountable for both.

Power your risk assessment with intelligent AI solutions

For credit unions and banks ready to modernize their risk management and compliance practices, advanced AI solutions are within reach.

RiskInMind's platform is purpose-built for community lenders navigating the full spectrum of credit risk and regulatory compliance. From initial loan evaluation to ongoing portfolio surveillance, the platform's specialized AI agents work together under the direction of Ava, our central AI director, to deliver real-time risk insights with response times under half a second.

The AI-powered loan assessor automates credit analysis at origination, surfacing risk signals and generating documentation that supports both internal review and regulatory audit. For commercial real estate portfolios, the CRE loan risk predictor delivers property-level risk scoring integrated with market and collateral data. Compliance teams benefit from the AI regulatory risk agent, which monitors regulatory changes, automates reporting workflows, and keeps your institution current with NCUA, FDIC, and CFPB requirements. All solutions operate within a SOC 2® certified, bank-grade security environment.

Frequently asked questions

What are the Five Cs of credit in lending risk assessment?

The Five Cs are character, capacity, capital, collateral, and conditions, and they form the qualitative foundation for evaluating borrower risk profiles in both consumer and commercial lending contexts.

How does AI improve lending risk assessment accuracy?

XGBoost models and other machine learning approaches identify complex, nonlinear risk patterns across large datasets that traditional logistic regression models miss, producing materially higher predictive accuracy for default classification.

When is human judgment required over AI in lending risk?

Manual reviews are essential for edge cases including fraud flags, regulatory compliance triggers, borrowers with subprime profiles, and situations where model uncertainty is high enough to make an automated decision indefensible in audit or examination.

What is the FDIC/NCUA asset quality rating scale?

The 1-5 rating scale assigns supervisory grades to asset quality, with 1 representing strong performance and minimal regulatory concern and 5 signaling critical deficiencies that require immediate corrective action.

Why must AI models be explainable in banking?

ECOA and Regulation B require institutions to provide specific, actionable adverse action reasons to declined applicants, which means any AI model driving credit decisions must be capable of generating compliant, plain-language explanations for each outcome.

Recommended

- Risk management for credit unions: frameworks and AI solutions | RiskInMind

- Why risk management is essential for lenders: AI-driven insights | RiskInMind

- Financial institution risk: Core types and mitigation | RiskInMind

- Loan risk modeling explained: Strategies for better credit decisions | RiskInMind