Risk management professionals at financial institutions face a convergence of pressures that makes knowing how to manage risk data securely more consequential than ever. Regulatory frameworks like GLBA and NYDFS Part 500 demand specific technical controls, while threat actors increasingly target the sensitive loan performance data, stress test outputs, and credit model inputs that sit at the core of your operations. A breach in this data does not just create remediation costs. It undermines regulatory confidence, triggers mandatory disclosure timelines, and can erode the trust your institution has built over decades.

Table of Contents

- Key takeaways

- How to manage risk data securely: the foundational layer

- Technical execution: controls across the risk data lifecycle

- Ongoing verification: monitoring, testing, and compliance assurance

- Common pitfalls in risk data security strategies

- My perspective on where institutions actually struggle

- How RiskInMind supports secure risk data management

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Start with a written security program | GLBA requires a documented program covering nine security elements before any technical controls make sense. |

| Classify and tag risk data at creation | Data you cannot identify cannot be protected; classification drives every downstream access and encryption decision. |

| Apply controls across the full lifecycle | Encryption, access management, and audit logging must follow risk data from creation through archival and deletion. |

| Monitor continuously, not periodically | Real-time anomaly detection and ongoing access reviews sustain compliance between formal audit cycles. |

| Integrate security into risk workflows | Stress test models, credit analyses, and portfolio reports each represent sensitive data pathways requiring embedded controls. |

How to manage risk data securely: the foundational layer

Before a single technical control is deployed, your institution needs a governing policy structure that makes those controls coherent and defensible to examiners. The GLBA Safeguards Rule requires a written information security program with nine defined elements, updated in 2023, including a designated Qualified Individual, formal access controls, encryption standards, and continuous monitoring obligations enforced by the FTC. That program is not a compliance checkbox. It is the architecture specification that every technical decision should trace back to.

Data classification comes next, and it is where many institutions lose traction. Risk data is not homogeneous. A loan officer's credit memorandum contains intermittent sensitive fields mixed with routine commentary. A stress test dataset includes both public macroeconomic inputs and confidential portfolio exposures. Your classification schema must distinguish between these categories at a granular level, applying labels that trigger appropriate handling rules automatically rather than relying on individual judgment.

Assigning formal data ownership is equally critical. Each risk data asset should have a named steward, typically a business unit leader who accepts accountability for access decisions and classification accuracy, supported by an information security officer who enforces technical compliance.

- Define data tiers: confidential (individual credit data, model inputs), internal (aggregate portfolio reports), and public (regulatory disclosures).

- Require data owners to review classification labels at least annually, particularly after product launches or regulatory changes.

- Document your classification criteria in the written security program so examiners can trace decisions to policy.

NYDFS Part 500 mandates encryption of nonpublic information both in transit and at rest, multi-factor authentication, audit trail requirements, and incident reporting within 72 hours. If your institution operates under New York licensure, those requirements are not aspirational. They are the minimum bar.

Pro Tip: Map each of your GLBA and NYDFS obligations to a specific technical control and a named owner. When an examiner asks for your control evidence, that mapping document alone can compress a regulatory inquiry by days.

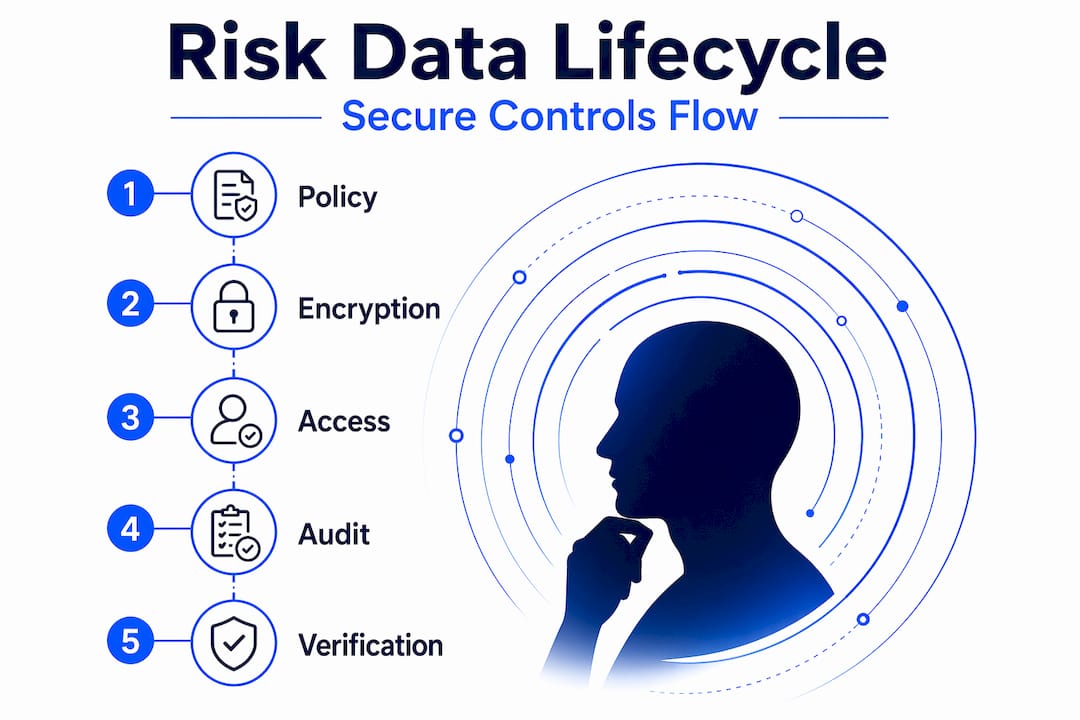

Technical execution: controls across the risk data lifecycle

Understanding what is risk data management at a technical level means recognizing that protection must follow data through creation, processing, storage, sharing, and deletion. A risk-based lifecycle approach combines discovery, appropriate safeguards, and continuous monitoring rather than applying blanket protections to everything and calling it done.

The execution sequence below reflects the order that controls should be implemented, not the order they are typically remembered.

-

Discover and profile your risk data assets. Before encrypting anything, map where sensitive data lives across your systems, including unstructured data artifacts such as loan review memos, model validation reports, and examiner correspondence. These documents contain intermittent sensitive fields that require targeted inspection at the column and row level, not just dataset-level governance.

-

Apply encryption at rest and in transit. The Critical Security Controls v8.1 specify encryption alongside audit logging and access control lists as minimum safeguards for sensitive data handling. For risk data specifically, this means encrypting your credit model databases, portfolio analytics outputs, and stress test archives, not just customer-facing transaction records.

-

Enforce least-privilege access. Fine-grained access policies drastically reduce the blast radius when credentials are compromised by ensuring that a stolen account accesses only what that role genuinely requires. For a credit analyst, that means read access to assigned portfolios, not write access to model configuration files or audit logs.

-

Implement de-identification for shared datasets. When risk data crosses internal boundaries, such as moving from the credit team to the finance team for capital planning, de-identification and obfuscation preserve analytical utility while preventing overexposure of individual borrower attributes. Masking specific fields at query time, rather than creating anonymized copies, is a more maintainable approach at scale.

-

Maintain tamper-resistant audit logs. Logs themselves constitute sensitive assets. The security control framework mandates that audit logs be protected against unauthorized modification or deletion, since their integrity is what makes incident traceability and compliance evidence defensible.

-

Embed controls into risk workflows. Stress testing, model validations, and loan underwriting workflows each pass sensitive data through multiple systems. Controls cannot be bolted on at the end of those pipelines. They need to be integrated at each handoff point.

| Control | Protects against | Implementation priority |

|---|---|---|

| Encryption at rest and in transit | Unauthorized data extraction | Immediate |

| Least-privilege access | Credential compromise, insider threat | Immediate |

| De-identification for shared data | Overexposure during cross-team transfers | High |

| Tamper-resistant audit logs | Evidence destruction, compliance gaps | High |

| MFA on all data access points | Account takeover | Immediate |

Pro Tip: Treat your audit log infrastructure as a separate security domain. Store logs in a write-once system with access restricted to your security team and external auditors only. An attacker who can delete logs can erase the evidence of their own intrusion.

Ongoing verification: monitoring, testing, and compliance assurance

Secure risk data management is not a project with a completion date. It is a continuous operating posture. Regulators expect ongoing monitoring of IT control effectiveness with documented escalation procedures and management oversight, not just point-in-time assessments.

Your verification program should operate across three timeframes simultaneously. Daily automated monitoring should surface anomalous access patterns, failed authentication attempts, and unexpected data transfers. Quarterly security testing should include vulnerability scans of systems that store or process risk data. Annual penetration tests should specifically target the pathways through which risk data flows, including API endpoints connecting risk systems to reporting tools and regulatory submission platforms.

Incident response readiness deserves particular attention. Many institutions have a plan on paper but have never run a tabletop exercise that actually simulates a risk data exfiltration scenario. When sensitive credit model inputs are compromised, the 72-hour NYDFS reporting clock starts immediately, and your response team needs to operate with precision under that pressure.

Vendor and third-party risk management is a frequently underweighted component of best practices for risk data. Consider the following areas when assessing your control environment:

- Validate that critical service providers maintain controls equivalent to your internal standards, and do not accept SOC 2 reports as a substitute for your own vendor risk assessments.

- Require contractual notification provisions aligned with your regulatory reporting timelines.

- Review real-time risk monitoring capabilities to understand how technology can support continuous assurance rather than manual review cycles.

- Conduct annual role-based security training that covers the specific data types each team handles, not generic phishing awareness modules.

Common pitfalls in risk data security strategies

Even well-resourced institutions make predictable errors in how to protect risk data, and those errors tend to cluster around four failure modes.

The first is classification decay. Institutions often classify data accurately at system deployment and then fail to re-classify as data volumes grow and new fields are added. A model that initially captured five data elements may now ingest forty, with the additional fields never reviewed against your sensitivity criteria.

The second is orphaned access. Staff changes, role transitions, and system migrations leave behind access privileges that no longer match current responsibilities. A former credit analyst who moved to marketing two years ago may still have read access to current portfolio stress test files. Quarterly access reviews are not optional if you are operating under GLBA or NYDFS.

The third is encryption gaps at integration points. Most institutions encrypt their primary databases correctly. The exposure typically occurs at API layers, middleware caches, and logging pipelines where data passes through in plaintext. An integrated data security approach requires governance artifacts to travel with the data across all system boundaries, not just at endpoints.

- Audit integration point encryption separately from database encryption.

- Review service account permissions alongside user account permissions.

- Test your incident response plan with a scenario specifically involving risk data, not a generic IT breach.

Pro Tip: Schedule a semi-annual "access rights purge" as a formal agenda item for your data governance committee. The discipline of blocking calendar time for it is what separates institutions that maintain least privilege in practice from those that maintain it only in policy.

The fourth failure mode is neglecting secure risk platforms that unify classification, access control, and audit logging under a single governance layer, requiring manual coordination across disconnected tools instead.

My perspective on where institutions actually struggle

I've spent years working alongside risk management teams at community banks and credit unions, and the pattern I see most consistently is not a lack of technical knowledge. It is the disconnection between governance artifacts and technical execution. Security policies sit in a SharePoint folder while the systems those policies are supposed to govern operate on different assumptions entirely.

What I've learned is that the institutions that navigate regulatory examinations most confidently are the ones where the CRO and the CISO share a common vocabulary and a common dashboard. When the governance team and the technical team are solving the same problem in separate rooms, you end up with policies that cannot be verified and controls that cannot be explained.

The other uncomfortable truth I'd offer is this: incident response readiness is almost always overestimated. Every team I've spoken with believes they could execute a response within regulatory timelines until they actually run a simulation. The 72-hour NYDFS notification window is unforgiving, and the steps required before notification can even be assessed, including evidence preservation, scope determination, and legal review, consume far more time than most teams anticipate.

Future-proofing risk data security against AI-generated threats and increasingly sophisticated supply chain attacks requires building adaptive controls, not just compliant ones. Compliance confirms you met the standard yesterday. Adaptive controls protect the data you hold today.

— Raj

How RiskInMind supports secure risk data management

RiskInMind's AI-powered platform was built specifically for the operational realities of credit unions, community banks, and lenders managing sensitive data under GLBA and NYDFS requirements. Its suite of specialized AI agents handles risk data discovery, classification, and continuous monitoring within a SOC 2® certified environment, giving your team the assurance of bank-grade security without the manual coordination burden that typically comes with it. The platform's real-time processing and compliance automation integrate directly with regulatory reporting workflows, so that governance and technical controls operate from a single source of truth. Explore the full platform capabilities or review pricing options scaled to your institution's size and risk profile.

FAQ

What is risk data management in financial institutions?

Risk data management refers to the systematic process of identifying, classifying, protecting, and governing the data used in credit risk assessment, portfolio monitoring, stress testing, and regulatory reporting. Secure risk data management adds the layer of technical and administrative controls required to protect that data from unauthorized access and ensure regulatory compliance.

What does GLBA require for risk data security?

The GLBA Safeguards Rule requires a written information security program covering nine elements, including designated oversight, access controls, encryption, and monitoring. Financial institutions subject to FTC enforcement must maintain and periodically test these safeguards across all systems that process customer financial data.

How does least-privilege access protect risk data?

Least-privilege access limits each user or system account to only the data and functions required for their specific role. This reduces the potential damage from compromised credentials, since an attacker or insider can only access what that account was authorized to reach, not the full dataset.

How often should access rights to risk data be reviewed?

Access rights should be reviewed at least quarterly for systems holding confidential risk data, with immediate revocation triggered by role changes, departures, or security incidents. Institutions operating under NYDFS Part 500 have explicit access review obligations tied to their cybersecurity program.

What is the biggest security gap in risk data workflows?

The most common gap is unprotected integration points between systems, particularly API layers and middleware caches where data passes in plaintext between otherwise encrypted databases. Encryption and access controls must be applied at every data transit point, not just at storage endpoints.

Recommended

- Why Secure Risk Platforms Matter for Financial Institutions | RiskInMind

- Risk analytics step by step: A practical guide for financial institutions | RiskInMind

- Why Focus on Risk Technology for Financial Institutions | RiskInMind

- Real-time risk assessment guide for financial institutions | RiskInMind