Financial institutions have spent the last decade deploying increasingly sophisticated AI models for credit decisioning, fraud detection, and portfolio risk monitoring. Yet a persistent and consequential problem has emerged alongside that progress: when a model flags a loan as high-risk or denies a credit application, no one can fully explain why. Understanding what is explainable AI in risk management is no longer an academic exercise. It is a regulatory obligation, a governance requirement, and, increasingly, a competitive differentiator. This guide covers the core concepts, technical methods, regulatory implications, and practical steps that risk professionals and data analysts need to apply explainable AI effectively within their institutions.

Table of Contents

- Key Takeaways

- What explainable AI in risk management actually means

- Types and techniques of AI risk model explainability

- Regulatory and governance dimensions of XAI

- Benefits and real limitations of XAI in risk assessment

- Implementing XAI in risk management workflows

- My perspective on the evolving role of explainability

- How Riskinmind supports explainable AI governance

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| XAI is a governance requirement | Explainable AI aligns AI outputs with regulatory obligations like ECOA, CFPB guidance, and the EU AI Act. |

| Local and global explanations serve different purposes | Local explanations address individual decisions; global explanations expose systemic bias and model behavior patterns. |

| Method selection demands alignment | Matching explanation techniques to model architecture and the explanation audience prevents misleading or non-actionable outputs. |

| XAI must be embedded, not bolted on | Integrating explainability into model validation packages produces more defensible and genuine explanatory evidence. |

| Explainability alone is not sufficient | XAI should be combined with runtime monitoring, bias audits, and lifecycle traceability to achieve trustworthy AI governance. |

What explainable AI in risk management actually means

Explainable AI (XAI) is the practice of making AI model operations and outputs understandable to those who rely on them. The OECD frames this as clarifying how a model reaches its conclusions so that stakeholders can verify its behavior and use it responsibly. In the context of financial risk, that means a credit analyst, compliance officer, or regulator can trace the reasoning behind a lending decision rather than simply accept a score.

Explainability, interpretability, and transparency are related but distinct attributes. Interpretability refers to the degree to which a model's internal logic is inherently understandable, as with a simple decision tree. Transparency is a broader attribute covering how openly an institution documents and discloses its AI systems. Explainability sits at the practical intersection, describing the tools and methods that produce human-readable rationales for model outputs.

There are several key attributes that define effective XAI in financial risk contexts:

- Accountability: Explanation outputs link decisions to responsible actors and auditable processes.

- Traceability: Every model output can be traced back through data inputs, modeling choices, and decision logic.

- Trustworthiness: Explanations genuinely reflect actual model behavior rather than serving as post-decision justifications.

- Fairness: Explanations help surface discriminatory patterns or disparate impact across protected classes.

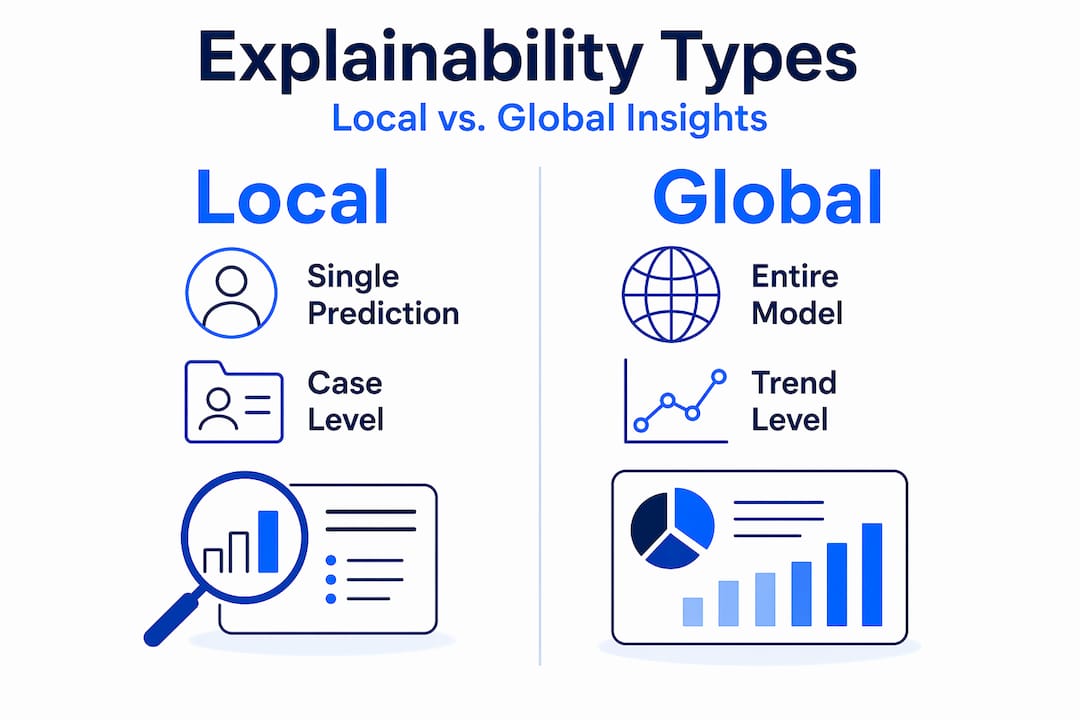

One distinction that every risk analyst should internalize is the difference between local and global explainability. Local explanations address a single prediction, such as why a specific borrower received a particular risk score. Global explanations describe how a model behaves across an entire population, which is where systemic bias and structural model failures tend to become visible. XAI makes model behavior understandable for validation teams, compliance officers, and consumer-facing decisions simultaneously. Model-agnostic methods, which apply across different model architectures, and model-specific methods, which are tailored to a particular algorithm, further shape the practical choices available to risk teams.

Types and techniques of AI risk model explainability

The landscape of explainable machine learning methods is wide, and selecting the wrong technique for a given risk use case can produce outputs that are technically correct but practically useless. The three most widely deployed methods in financial institutions are SHAP, LIME, and counterfactual explanations.

SHAP (SHapley Additive exPlanations) assigns each input feature a contribution value to a specific prediction, drawing from cooperative game theory. A credit risk model using SHAP can tell an underwriter that debt-to-income ratio contributed 40% of the elevated risk score for a given applicant, while recent delinquencies contributed 30%. SHAP supports both local and global analysis, making it particularly versatile for credit risk teams.

LIME (Local Interpretable Model-agnostic Explanations) works by perturbing input features around a specific prediction and fitting a simpler, interpretable model to approximate the complex model's behavior at that point. LIME is local and model-agnostic, meaning it can be applied to almost any model architecture without modification. Its limitations center on stability. LIME explanations for the same input can vary across runs, which creates challenges in regulated environments where consistency is expected.

Counterfactual explanations take a different approach entirely. Rather than assigning feature importance, they answer the question: "What is the minimal change to the input that would have produced a different outcome?" In credit decisioning, counterfactual explanations align directly with adverse action notice requirements, because they translate naturally into statements like "If your debt-to-income ratio were 5% lower, this application would have been approved."

| Method | Scope | Model dependency | Best use case |

|---|---|---|---|

| SHAP | Local and global | Model-agnostic | Feature attribution for credit scoring and portfolio risk |

| LIME | Local | Model-agnostic | Rapid instance-level explanations for compliance review |

| Counterfactual | Local | Model-agnostic | Adverse action notices and consumer-facing disclosures |

| Decision trees | Global | Model-specific | Inherently interpretable models in low-complexity risk tasks |

| Gradient-based methods | Local | Model-specific | Neural network risk models requiring layer-level attribution |

Inherently interpretable models, including logistic regression and decision trees, remain defensible choices in highly regulated environments precisely because their logic is transparent by design. The trade-off is predictive power. As risk models grow more sophisticated to capture non-linear borrower behavior, the interpretability gap widens and the need for post-hoc explanation methods grows.

Pro Tip: Before selecting a specific XAI technique, align explanation methods with both your model architecture and the intended explanation audience. A SHAP summary plot is meaningful to a data scientist but often unintelligible to a compliance officer or consumer. The right technique is the one your audience can act on.

Regulatory and governance dimensions of XAI

Financial regulators do not use the term "explainable AI" uniformly, but the expectations embedded in existing rules are unambiguous. The Equal Credit Opportunity Act (ECOA) requires that adverse action notices provide specific reasons for credit decisions. The CFPB has signaled that "the model said so" does not constitute a valid reason. The EU AI Act classifies credit scoring systems as high-risk AI applications subject to transparency and documentation requirements. Together, these frameworks create a de facto mandate for explainability in AI-driven credit and risk decisions.

The OECD's accountability principle goes further, requiring that AI actors ensure traceability across datasets, modeling processes, and decision outputs so that auditors and regulators can reconstruct the basis for any decision. This is not a one-time documentation exercise. It is a continuous obligation that must be embedded into the AI lifecycle from data ingestion through model deployment and monitoring.

From a model risk management perspective, the governance implications of XAI include:

- Auditability: Regulators and internal auditors must be able to reconstruct the reasoning behind individual risk decisions on demand.

- Adverse action compliance: XAI methods like counterfactual explanations must produce disclosures that are specific, accurate, and actionable for consumers.

- Model validation integration: XAI analyses embedded within validation evidence packages are far more defensible than explanations assembled after a regulator asks a question.

- Fair lending oversight: Global explanations, applied systematically across borrower populations, are necessary to detect disparate impact that local, case-by-case reviews will miss.

- Lifecycle traceability: Logging explanation outputs across the model lifecycle creates a documented record that satisfies both internal governance and external examination requirements.

The XAI framework for credit risk published in 2026 reinforces that combining local and global interpretation tools within a structured governance process produces explainability outputs that regulators can rely on rather than simply inspect. AI transparency in risk management is not about generating explanation artifacts. It is about creating a continuous, auditable connection between model behavior and documented decision rationale.

Benefits and real limitations of XAI in risk assessment

The explainable AI benefits for financial institutions are real and well-documented, but they come with constraints that risk professionals must understand to avoid overconfidence in their governance frameworks.

-

Improved stakeholder trust: When underwriters, risk committees, and board-level oversight functions can see why a model assigns a particular risk rating, confidence in AI-driven decisions increases across the organization. Stakeholder trust does not come from model performance metrics alone; it comes from the ability to explain and defend decisions under scrutiny.

-

Bias and fairness detection: Local explanations for individual cases are necessary but insufficient for fair lending governance. Global explanation checks reveal whether a model systematically disadvantages protected groups in ways that no individual case review would surface.

-

Clearer cross-functional communication: XAI creates a shared language between technical modeling teams and risk governance functions. A feature attribution output bridges the gap between a data scientist's gradient-boosted model and a chief risk officer's need to justify portfolio decisions to regulators.

-

Support for AI in risk assessment maturity: Institutions that integrate explainability into financial risk processes demonstrate a higher level of AI governance maturity, which increasingly factors into regulatory examinations and supervisory expectations.

The limitations deserve equal attention. Explainability methods do not guarantee that the explanation accurately reflects the model's actual decision logic. Wharton research highlights the risk of interpretability arbitrage, where explanation plots satisfy regulatory optics without genuinely testing real model behavior on real cases. Large language models and generative AI introduce additional complexity, as their internal reasoning processes are far less tractable than gradient-boosted trees or logistic regression models.

Pro Tip: Treat XAI outputs as one input into a broader AI governance process, not as a substitute for runtime monitoring, ongoing bias audits, and documented model validation. Explanation artifacts that are not regularly tested for fidelity to actual model behavior can become a source of regulatory exposure rather than protection.

Implementing XAI in risk management workflows

Deploying explainable AI effectively within a financial institution requires more than installing a SHAP library. It requires deliberate design choices across people, process, and technology.

- Define your explanation audience first. A credit analyst, a compliance officer, a consumer, and a bank examiner all need different types of explanations. Identify who will receive explanations and what decisions they need to make before selecting a technique.

- Integrate XAI into model validation proactively. Embedding XAI analyses into validation evidence packages from the start produces more defensible documentation than generating explanations reactively when regulators ask.

- Build logging and monitoring infrastructure. Explanation outputs should be logged alongside model predictions so that any decision can be reconstructed and reviewed. Without this infrastructure, explainability is a point-in-time exercise rather than a governance capability.

- Align disclosure practices to jurisdiction. Adverse action notice requirements differ between ECOA, state-level fair lending rules, and the EU AI Act. Explanation outputs must be tailored to the specific regulatory context in which they will be used.

- Avoid mismatched methods and audiences. The operational pitfall of misaligned explanation methods and decision audiences is one of the most common failures in XAI implementation. A global feature importance plot is not a valid adverse action notice.

- Combine XAI with complementary governance tools. Runtime monitoring detects model drift. Bias audits assess disparate impact over time. XAI supports but does not replace these functions. Refer to advanced AI risk management strategies for a framework that integrates all three.

My perspective on the evolving role of explainability

I've spent considerable time working through how financial institutions approach explainability, and the most consistent pattern I see is that organizations treat explanation artifacts as a destination rather than a starting point. A SHAP plot lands in the model validation package, regulators don't object, and the team moves on. That is not explainability. That is explainability theater.

What I've observed in the more sophisticated institutions is a genuine shift toward runtime AI governance, where explanation outputs are continuously monitored and tested for fidelity to actual model behavior. The institutions that get this right don't just produce explanations on demand. They ask, every quarter, whether the explanation they are producing today still reflects how the model is actually deciding.

The regulatory trend line points toward harder requirements, not softer ones. The importance of explainable AI will only grow as supervisors in the US and abroad become more technically sophisticated. The institutions that build genuine explainability capability now, integrated into lifecycle traceability and real-time governance, will face far less remediation pressure than those who treat it as a compliance checkbox. Explainability doesn't just protect your models. It protects your institution.

— Raj

How Riskinmind supports explainable AI governance

Riskinmind's AI-powered risk management platform is designed for exactly the governance challenges described throughout this article. The platform's suite of specialized AI agents handles credit risk assessment, regulatory compliance, and portfolio monitoring with traceability and auditability built into the workflow rather than added as an afterthought. Products like the CRE Loan Risk Predictor and the AI Credit Card Analyzer incorporate explainability features that align with ECOA, CFPB, and model risk management expectations. For credit unions, community banks, and lenders seeking to advance their AI governance maturity, Riskinmind provides the infrastructure to move from black-box decisioning to auditable, explainable AI at the enterprise risk management level. Explore the platform to see how explainability and compliance work together in practice.

FAQ

What is explainable AI in risk management?

Explainable AI in risk management refers to methods and frameworks that make AI model outputs understandable and auditable for risk professionals, regulators, and consumers. It enables financial institutions to trace the reasoning behind credit decisions, risk scores, and compliance determinations.

How does explainable AI work in credit decisioning?

Explainable AI works by applying techniques like SHAP, LIME, or counterfactual explanations to translate complex model outputs into human-readable rationales. These rationales can be used to support adverse action notices, model validation, and fair lending compliance reviews.

What are the main types of AI risk model explainability?

The primary types are local explainability, which addresses individual predictions, and global explainability, which describes overall model behavior across a population. Methods are further categorized as model-agnostic (applicable to any model) or model-specific (tailored to a particular architecture).

What are the key regulatory drivers for explainable AI?

ECOA requires specific reasons for adverse credit decisions, the CFPB has emphasized that algorithmic model outputs alone are insufficient justification, and the EU AI Act classifies credit scoring as a high-risk AI application requiring transparency documentation. These regulations collectively mandate explainability in AI-driven financial decisions.

What are the limitations of explainable AI in financial risk?

Explainability methods do not guarantee that the explanation accurately reflects actual model behavior, and Wharton research has documented risks of interpretability arbitrage where explanation outputs satisfy regulatory optics without testing real decisioning logic. XAI must be combined with runtime monitoring, bias audits, and lifecycle traceability to function as genuine governance.