Conventional risk tracking often captures averages, but regulators and today's operating environment demand something faster and more precise. As NCUA 2026 priorities make clear, examiners focus on tail-loss scenarios and real-time responsiveness, not just where your numbers sit on a given quarter's summary. Credit unions that still rely on static reports and monthly spreadsheet reviews are leaving meaningful exposure gaps that can widen before anyone notices. This guide walks through the core frameworks, key risk categories, concentration risk discipline, and how AI-powered tools are reshaping what exam-ready risk management actually looks like in practice.

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

Table of Contents

- Core principles of risk management for credit unions

- Key risk types and how the NCUA evaluates them

- Concentration risk: focus area, methodologies, and best practices

- AI-powered risk management: real-time insights, automation, and compliance gains

- Growth versus safety: strategic risk decisions and edge cases

- A smarter playbook: what most miss about credit union risk management

- Ready to modernize your credit union's risk management?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| CAMELS is foundational | NCUA examiners use CAMELS to assess all critical financial and risk categories for credit unions. |

| AI boosts compliance | AI solutions offer real-time insights and automation for risk, compliance, underwriting, and portfolio monitoring. |

| Concentration risk requires vigilance | Stress testing, peer benchmarking, and diversification help credit unions avoid outlier losses in their loan portfolios. |

| Frameworks must fit size | Overly complex or too-simple frameworks can both be dangerous—tailor your approach to your credit union’s scale and complexity. |

| Growth and safety are in tension | Aggressive asset growth often increases risk; monitor capital buffers closely to prevent solvency issues. |

Core principles of risk management for credit unions

Now that we've seen why basic risk tracking isn't enough, let's clarify what advanced risk management really looks like for today's credit unions.

Credit union risk management is structured around identifying, assessing, monitoring, addressing, and reporting risks to align with risk appetite, strategy, and NCUA requirements. That definition sounds straightforward, but in practice it requires coordinated governance, documented policies, and consistent execution across every line of business. It also means your risk appetite statement must be more than a compliance checkbox. It should drive real decisions about lending programs, product launches, and capital allocation.

Alignment with NCUA expectations is non-negotiable. The CAMELS rating system underpins how examiners evaluate credit unions across six dimensions: Capital adequacy, Asset quality, Management, Earnings, Liquidity, and Sensitivity to market risk. Each element ties back to how well your risk framework captures real exposures and how promptly leadership responds when conditions shift.

A well-structured framework includes three core elements: governance (board-level oversight and clear accountability), ongoing monitoring (not just quarterly reviews), and regular risk assessments that feed directly into strategic planning. Without that feedback loop, even the most detailed risk register becomes a historical document rather than a decision-support tool.

One important nuance: the sophistication of your framework should match your institution's size and complexity. Structured risk management approaches that work for a $2 billion credit union may overwhelm a smaller institution and produce more confusion than clarity.

"Don't over-complicate if you're a small CU. Regulators want clarity, not complexity. A simple, well-executed framework consistently outperforms a sophisticated one that nobody actually follows."

The core elements every credit union needs, regardless of size, include:

- A documented risk appetite statement tied to capital and earnings targets

- Clear ownership for each major risk category

- A monitoring cadence with escalation triggers

- Board reporting that highlights emerging trends, not just trailing averages

AI-driven risk intelligence is increasingly what separates credit unions that pass exams with confidence from those that scramble before each cycle.

Key risk types and how the NCUA evaluates them

With the high-level framework in mind, let's get practical by mapping out what risks truly matter and how regulators expect you to measure them.

The CAMELS framework gives examiners a holistic lens, but it's the specific risk categories within each component that drive examiner findings. Top risks for credit unions include credit, interest rate, liquidity, compliance, cyber and fraud, and strategic risk. NCUA evaluates each through both quantitative benchmarks and qualitative assessments of management's ability to identify and respond to emerging issues.

Here's a snapshot of system-wide benchmarks based on Q4 2024 data that help contextualize where your portfolio stands:

| Metric | System average | Examiner concern threshold |

|---|---|---|

| Delinquency rate | 0.87% | Above 1.50% |

| Net charge-off (NCO) ratio | 0.72% | Above 1.00% |

| Net worth ratio | 10.5% | Below 7.00% (well-capitalized) |

| Loan-to-share ratio | 82.4% | Elevated if above 90% |

What examiners dig into goes beyond these averages. Concentration exposure, tail-loss scenarios, and business model vulnerabilities are where most findings originate. A credit union with a 0.6% delinquency rate but heavy commercial real estate concentration in a single geographic market will draw more scrutiny than one with a 1.0% rate spread across a diversified portfolio.

The six primary risk categories every risk officer should track with precision:

- Credit risk: Loan performance, underwriting standards, CRE loan analytics, and CECL reserve adequacy

- Interest rate risk: Duration mismatches, repricing exposure, and sensitivity scenarios

- Liquidity risk: Access to funding, contingency funding plans, and stress scenarios

- Compliance risk: Regulatory adherence including BSA, fair lending, and consumer protection

- Cyber and fraud risk: IT controls, vendor management, and incident response readiness

- Strategic risk: Growth strategy sustainability, merger activity, and business model assumptions

Pro Tip: Stress-test for tail events at least quarterly. CECL readiness and credit card risk analysis are two areas where early stress-testing consistently uncovers exposures that static models miss entirely.

Concentration risk: focus area, methodologies, and best practices

Credit unions face many risks, but none attract examiner attention quite like concentrations. Here's what you need to know to avoid becoming the next warning signal.

Concentration risk emerges when a large portion of your portfolio is tied to a single borrower, industry, geography, or loan product. Post-2024, with commercial real estate valuations under pressure in multiple markets, examiners have sharpened their focus on credit unions that allowed concentrations to drift upward during the growth years without building matching capital buffers or policy controls.

Concentration risk methodologies that regulators expect to see include scenario stress-testing, board-approved concentration limits, quarterly monitoring cycles, and capital-at-risk assessments that translate exposure into potential loss impact.

Here's how basic versus advanced approaches compare:

| Approach | Basic | Advanced |

|---|---|---|

| Measurement | Simple exposure totals | Capital-at-risk and loss estimates |

| Stress testing | Annual or ad hoc | Quarterly, scenario-based |

| Policy limits | Set and reviewed annually | Dynamic, tied to capital and market shifts |

| Board reporting | Summary totals | Trend analysis with peer benchmarks |

| Mitigation tools | Internal diversification | Loan participations, derivatives, ALCO integration |

A practical step-by-step approach to managing concentrations effectively:

- Map your full concentration landscape by product type, geography, borrower industry, and collateral type.

- Set board-approved limits for each concentration category before they become findings.

- Run quarterly stress tests that model realistic loss scenarios under adverse conditions.

- Assess capital impact: how much would net worth drop under each stress scenario?

- Use loan participations or portfolio sales to diversify when a category approaches its limit.

- Integrate concentration data directly into your ALM and CECL processes for a unified risk view.

The board's role here is active, not passive. Directors should receive concentration reports that clearly flag trend direction, not just point-in-time totals. Reviewing ALM best practices alongside concentration data helps ensure that interest rate and credit concentration exposures are managed in coordination rather than silos.

Pro Tip: Use peer benchmarking data from NCUA's call report database to identify whether your concentrations are outliers relative to similarly sized credit unions. Being an outlier in concentration metrics without a clear strategic rationale is a reliable way to increase examiner scrutiny.

Credit risk memo automation tools can help standardize the documentation required to support concentration limit decisions and stress test narratives.

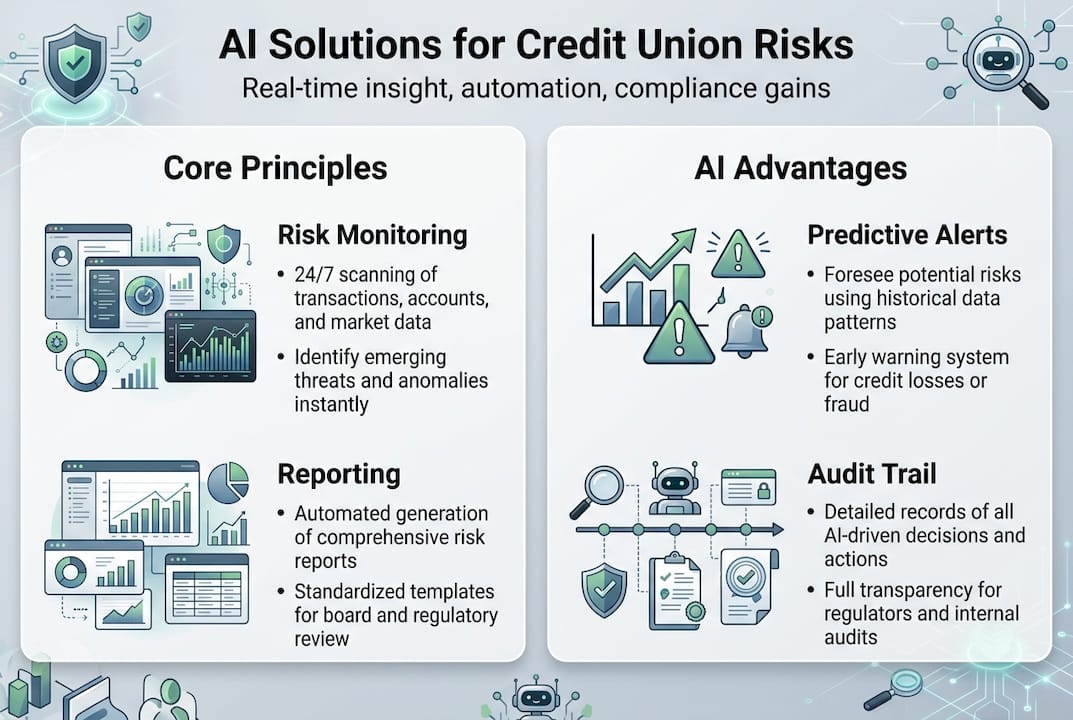

AI-powered risk management: real-time insights, automation, and compliance gains

Concentration risk is best managed with advanced tools. Here's how AI elevates your risk program from check-the-box to proactive and exam-ready.

Artificial intelligence is not a replacement for sound risk judgment. It is an accelerant that removes the manual bottlenecks slowing down your ability to act on emerging signals. AI enhances KRI tracking, predictive underwriting, and automated reporting in alignment with NCUA's technology focus, and the 2026 supervisory priorities signal that examiners increasingly expect institutions to use technology-driven monitoring.

The areas where AI delivers the most measurable value for credit union risk teams:

- Key risk indicator (KRI) monitoring: Automated tracking of portfolio metrics against thresholds, with real-time alerts when trends shift

- Predictive credit scoring: Machine learning models that identify borrower stress signals earlier than traditional scorecards

- Loss forecasting: Neural network-driven models that incorporate macroeconomic variables and portfolio-specific factors simultaneously

- Regulatory reporting automation: Reducing the manual effort in NCUA call report preparation and CECL documentation

- Data aggregation: Consolidating loan-level, market, and operational data into a unified risk dashboard with sub-second response times

AI-powered risk transformation works best when it is implemented methodically. Start with the risk categories that carry the highest potential loss impact for your institution, ensure data quality before deploying models, and tie every AI output back to a specific CAMELS discipline so examiners can follow the logic.

Real-time risk monitoring with AI has proven particularly valuable in catching early-stage delinquency migration before it reaches the level of a formal finding. Institutions that rely on monthly batch processing often miss the window where intervention is cheapest and most effective.

Pro Tip: Even the most advanced AI is wasted without clean data and clear ownership chains. Before deploying any model, audit your data pipelines and assign explicit accountability for each risk domain. AI as early warning only works when the humans behind it know who acts on the signal and how fast.

Growth versus safety: strategic risk decisions and edge cases

As technology drives better detection, some risks edge in through aggressive growth strategies. Here's what every credit union leader must get right.

Growth and safety are not natural adversaries, but pursuing one without disciplined guardrails on the other is how credit unions end up on NCUA's watch list. Non-core lending can drive asset growth at the expense of higher credit losses and lower net worth ratios, with examiners focusing directly on tail risks and solvency under stress.

The Q4 2024 system-wide trends in delinquency and NCO rates reflect a broader tension: credit unions that pushed loan growth aggressively between 2021 and 2023 are now working through the credit quality consequences.

"The institutions that grow fastest are not always the most resilient. Examiners have seen this cycle before, and their first question when NCOs spike is always: what did your concentration and underwriting policies look like two years ago?"

Edge cases that demand extra scrutiny in any risk framework:

- Purchased loan portfolios: Third-party underwriting standards may not match your own; ongoing monitoring is essential

- Derivatives for IRR hedging: Effective tools when properly governed, but complex enough that many smaller credit unions lack adequate expertise

- Indirect lending at scale: Volume growth that outpaces servicer monitoring capacity introduces layered credit and operational risk

- Aggressive pricing strategies: Rate-driven loan growth often correlates with adverse selection in the borrower pool

For smaller, non-complex credit unions, the three lines of defense model should be scaled to fit. A small team does not need three separate risk committees, but it does need clear separation between the people originating loans, the people reviewing them, and the people reporting results to the board. Balancing growth and safety requires that every strategic initiative go through a risk filter before it becomes a policy, not after it produces losses.

Recent academic research confirms that institutions with formalized risk appetite frameworks tied to capital planning consistently outperform peers during stress periods, even when they carry slightly lower pre-stress earnings.

A smarter playbook: what most miss about credit union risk management

Here is where most credit unions miss the mark, and how you can get ahead.

Too many risk programs are built for examiner consumption rather than operational protection. Teams spend weeks polishing policy documents before an exam cycle and then return to running on autopilot once the examiners leave. The uncomfortable truth is that your policies do not protect you. Your ability to act before bad numbers become headlines does.

The credit unions with the strongest risk posture share a specific mindset: risk management is a daily operating discipline, not a compliance deliverable. Governance frameworks matter only when they are connected to real-time data and clear escalation paths. When a portfolio segment starts deteriorating, the window for effective intervention is measured in weeks, not quarters.

Combining clear board-level governance with automated, real-time alerts from a platform like RiskInMind creates a genuine early-warning system rather than a retrospective reporting function. Real-world AI-driven interventions consistently show that the gap between a manageable problem and a regulatory finding is almost always a detection lag, not an inherent portfolio weakness. Closing that lag is the single highest-return investment most credit unions can make in their risk infrastructure right now.

Ready to modernize your credit union's risk management?

If you're ready to move beyond theory and see how the newest AI solutions can transform your credit union's risk workflow, here's a resource to help.

RiskInMind is built specifically for credit unions, community banks, and lenders that need more than a static dashboard. Our platform delivers real-time KRI monitoring, predictive underwriting through AI underwriting tools, and automated regulatory workflows through compliance automation, all backed by SOC 2® certification and sub-second response times.

Whether you are strengthening concentration controls, preparing for an NCUA exam cycle, or looking to automate CECL documentation, RiskInMind solutions give your team the visibility and speed to act on risk before it escalates. Request a demo today and see how Ava, our central AI director, coordinates specialized risk agents across every domain your program requires.

Frequently asked questions

What is the main goal of risk management for credit unions?

Credit union risk management aligns with stability and regulatory goals by protecting financial health through proactive identification, assessment, and mitigation of risks in alignment with board-approved policies and NCUA requirements.

How does the CAMELS framework impact risk oversight?

CAMELS is NCUA's primary framework for evaluating credit union risk, providing examiners a holistic view across capital, asset quality, management, earnings, liquidity, and sensitivity to ensure institutions meet safety and soundness standards.

Which risk types should credit unions prioritize in 2026?

NCUA has prioritized credit risk, interest rate risk, liquidity, compliance, cyber and fraud, and concentration risk as the top examination focus areas for 2026, per current supervisory guidance.

How does AI improve risk management for credit unions?

AI solutions enhance credit union risk management by delivering real-time KRI analysis, predictive risk detection, and automated compliance reporting, enabling faster decisions and more resilient portfolios.

What are common pitfalls in credit union risk management frameworks?

Frameworks must match institution size and risk profile; the most common mistakes include over-engineering governance for small credit unions, underestimating concentration and tail risks, and failing to build real-time monitoring capabilities into daily operations.

Recommended

- Transforming Credit Union Growth with AI-Powered Risk Intelligence | RiskInMind

- Stopping the Next 1st Choice: How RiskinMind.ai Helps Credit Unions Catch Trouble Before Failure | RiskInMind

- Credit RiskinMind AI Credit Memo Generator | RiskInMind

- RiskInMind - AI-Powered Risk Management Solutions

- How technology transforms trading education with AI