Machine learning models can reduce non-performing loans by 15 to 20% compared to traditional approaches, yet most financial institutions still rely on legacy scoring methods that were designed for a different economic era. That gap between capability and practice is where credit losses quietly accumulate. For risk management professionals and compliance officers, understanding modern loan risk modeling is no longer optional. It shapes underwriting quality, capital adequacy, and regulatory standing simultaneously. This article breaks down the core definitions, quantitative frameworks, technology trade-offs, and regulatory requirements that every serious risk team needs to master in 2026 and beyond.

Table of Contents

- Defining loan risk modeling and its core objectives

- Frameworks and key parameters: PD, LGD, and EAD

- Traditional vs. machine learning models: Performance and compliance trade-offs

- Meeting regulatory standards: Basel, IFRS 9, and CECL compliance

- Future trends and best practices in loan risk modeling

- A practitioner's take: Why modeling nuance matters more than ever

- Taking the next step: Smarter loan risk solutions

- Frequently asked questions

Automate Regulatory Model Risk Governance

Examine models against 32 qualitative criteria and resolve risk Tiers with pre-deployment checklists per OCC 2011-12 guidelines.

Key Takeaways

| Point | Details |

|---|---|

| Loan risk modeling essentials | It quantifies borrower default and potential losses for sound credit decisions and compliance. |

| PD, LGD, and EAD explained | Understanding these parameters is vital for modern regulatory and portfolio risk assessment. |

| Machine learning advantages | ML models can significantly boost predictive accuracy but must be explainable to meet regulations. |

| Critical compliance needs | Basel, IFRS 9, and CECL shape modeling requirements and demand robust, forward-looking frameworks. |

| Future-ready strategies | Ongoing best practices focus on scenario analysis, model validation, and embracing advanced tools for competitive edge. |

Defining loan risk modeling and its core objectives

At its foundation, loan risk modeling is the discipline of quantifying loan risk by estimating the probability that a borrower will default and calculating the financial loss that default would produce. The MathWorks credit risk reference defines it precisely: modeling quantifies default likelihood and potential loss to support sound lending decisions. That definition sounds straightforward, but the operational reality is considerably more complex.

Risk models serve multiple stakeholders inside a financial institution, each with distinct needs. Underwriters rely on model outputs to approve, price, or decline loan applications. Compliance officers use model documentation and validation records to satisfy regulatory examiners. Portfolio managers depend on aggregate model outputs to monitor concentration risk, set loss reserves, and stress test the book under adverse economic scenarios. When a model fails to serve all three groups simultaneously, the institution pays the price in either mispriced credit or regulatory findings.

The core objectives of loan risk modeling can be summarized as follows:

- Assessing borrower default probability using financial, behavioral, and alternative data inputs

- Estimating expected and unexpected losses across individual loans and portfolio segments

- Supporting capital allocation by linking model outputs to reserve and capital requirements

- Enabling regulatory reporting under frameworks such as Basel III/IV, IFRS 9, and CECL

- Informing pricing decisions so that loan rates reflect the true risk-adjusted cost of capital

"A risk model that only satisfies the regulator but fails to improve underwriting decisions is not a risk management tool. It is a compliance artifact."

Common use cases extend well beyond origination. Models are applied in annual reviews of commercial borrowers, in early warning systems that flag deteriorating credits before delinquency occurs, and in portfolio stress testing that estimates losses under recession or rate shock scenarios. The breadth of these applications means that model quality has a compounding effect: a well-calibrated model improves decisions at every stage of the loan lifecycle.

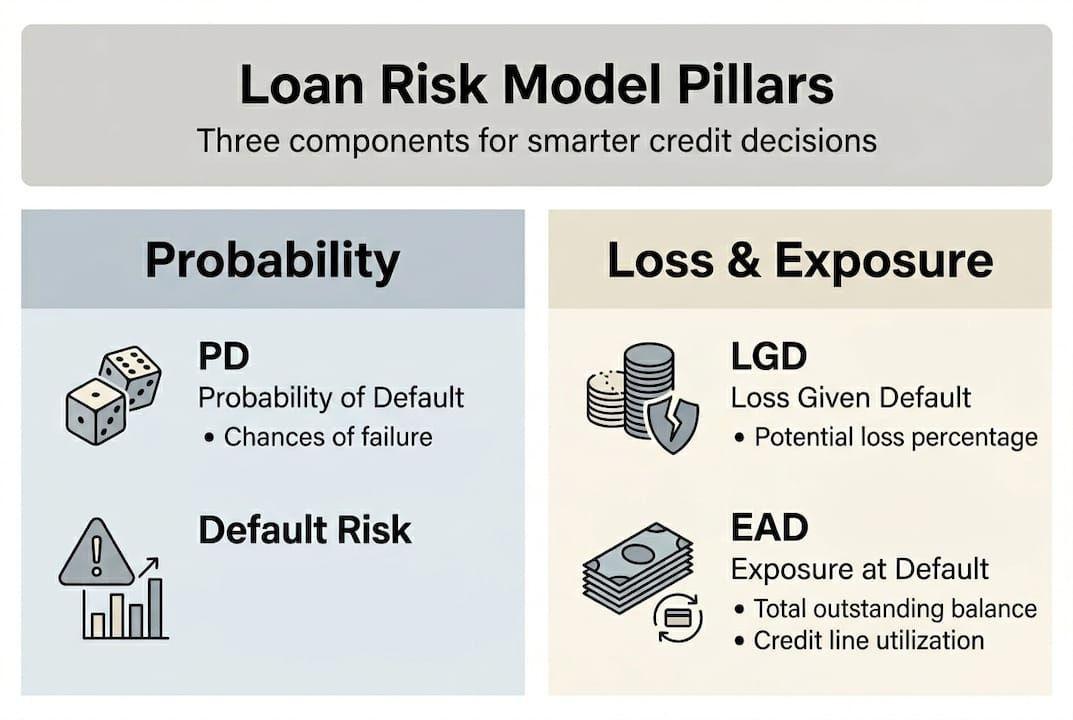

Frameworks and key parameters: PD, LGD, and EAD

The Basel II/III/IV frameworks established the three quantitative pillars that govern internal ratings-based (IRB) credit risk models: Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD). Together, these parameters define expected credit loss (ECL) as: ECL = PD x LGD x EAD. Understanding each component separately is essential before applying them in combination.

| Parameter | Definition | Key drivers |

|---|---|---|

| PD | Probability a borrower defaults within a defined horizon | Credit score, leverage, cash flow, payment history |

| LGD | Percentage of EAD lost if default occurs | Collateral value, seniority, recovery process |

| EAD | Total exposure outstanding at the time of default | Drawn balance, undrawn commitments, accrued interest |

Applying these parameters in a loan assessment follows a logical sequence:

- Estimate PD using a scorecard, logistic regression, or machine learning model trained on historical default data

- Estimate LGD using collateral appraisals, historical recovery rates, and workout cost assumptions

- Calculate EAD by combining current outstanding balance with credit conversion factors for undrawn lines

- Compute ECL by multiplying the three components, then segment results by loan stage for IFRS 9 or CECL reporting

Both IFRS 9 and CECL introduced forward-looking ECL models that require institutions to incorporate macroeconomic forecasts into PD and LGD estimates, a significant departure from the incurred-loss models they replaced. This shift demands richer data and more sophisticated modeling infrastructure.

Data quality is the silent determinant of model accuracy here. Garbage inputs produce garbage PD estimates regardless of model sophistication. Institutions that invest in clean, granular loan performance data consistently outperform those that do not, and examiners increasingly scrutinize data lineage as part of model validation reviews. Understanding FICO score limitations is also critical, since over-reliance on a single score can mask the nuance that PD, LGD, and EAD modeling is designed to capture.

Pro Tip: Run parallel ECL calculations using both point-in-time (PIT) and through-the-cycle (TTC) PD estimates during model development. The spread between the two outputs reveals how procyclical your model is, which is exactly what regulators and auditors will ask about during validation.

Traditional vs. machine learning models: Performance and compliance trade-offs

For decades, logistic regression was the workhorse of credit risk modeling. It is interpretable, well-understood by regulators, and relatively easy to validate. But its linear assumptions limit its ability to capture the complex, non-linear relationships between borrower characteristics and default behavior that exist in real portfolios.

Machine learning models, particularly gradient-boosted trees like XGBoost and deep neural networks, have changed the performance equation. ML models outperform logistic regression by up to 25% in AUC (area under the ROC curve), a standard measure of discriminatory power, but they introduce a compliance challenge: the black-box nature of many ML architectures makes it difficult to explain individual decisions to regulators or adverse-action notice recipients.

| Model type | AUC performance | Explainability | Regulatory acceptance |

|---|---|---|---|

| Logistic regression | Baseline | High | Well-established |

| Decision trees | Moderate gain | High | Generally accepted |

| XGBoost / gradient boosting | Up to 25% gain | Medium (with SHAP) | Conditional |

| Deep neural networks | High gain | Low without XAI tools | Requires justification |

The compliance challenge with ML models is not insurmountable. Explainable AI (XAI) techniques, particularly SHAP (SHapley Additive Explanations) values, allow risk teams to decompose individual model predictions into feature-level contributions. This satisfies the adverse action explanation requirements under ECOA and the Fair Housing Act while preserving most of the predictive advantage. The AI advances in credit assessment at leading institutions demonstrate that explainability and performance are not mutually exclusive.

Key considerations when choosing a modeling approach:

- Model governance: ML models require more rigorous ongoing monitoring for data drift and performance degradation

- Validation complexity: IRB model validation under Basel requires documented statistical tests that are more involved for ML architectures

- Adverse action compliance: Every declined applicant must receive a reason code, which demands feature-level explainability

- Operational integration: AI credit memo tools can bridge the gap between model output and underwriter workflow

The practical recommendation for most community banks and credit unions is a hybrid approach: use logistic regression or scorecard models as the primary decision tool, with ML models running in parallel to flag anomalies or enrich the analysis. This preserves regulatory comfort while building institutional capability in advanced modeling. Institutions exploring model explainability solutions will find that the technology has matured significantly in the past two years.

Meeting regulatory standards: Basel, IFRS 9, and CECL compliance

Regulatory frameworks do not merely constrain modeling choices. They define the minimum standard of rigor that every loan risk model must meet. IFRS 9 and CECL both require forward-looking ECL modeling and explicit staging of loans across their credit lifecycle, replacing the older incurred-loss approach with a more proactive, scenario-sensitive methodology.

For risk teams, the practical compliance steps are:

- Map your portfolio to staging criteria: Under IFRS 9, loans move from Stage 1 (12-month ECL) to Stage 2 (lifetime ECL) when credit risk increases significantly. Define your triggers clearly and document them.

- Incorporate macroeconomic scenarios: Both CECL and IFRS 9 require multiple forward-looking scenarios weighted by probability. Develop at least a base, upside, and downside scenario for key economic variables.

- Validate models against out-of-sample data: Regulators expect backtesting results that demonstrate model performance across different economic periods, not just the training window.

- Document model risk management: Maintain a model inventory, validation schedule, and change log. Examiners will ask for these during reviews.

- Align capital calculations with model outputs: Under Basel III/IV, IRB institutions must demonstrate that their PD, LGD, and EAD estimates feed directly into risk-weighted asset calculations.

A critical distinction that many teams underestimate is the difference between point-in-time (PIT) and through-the-cycle (TTC) model approaches. PIT models reflect current economic conditions and are more responsive but also more procyclical, meaning they can amplify capital requirements during downturns. TTC models smooth over the cycle and are more stable but may understate risk during rapid deterioration. Understanding this trade-off is central to CECL implementation strategies at community institutions.

"Procyclicality is not a modeling flaw to be tolerated. It is a systemic risk to be managed through deliberate model design."

Pro Tip: Review your CECL estimation approach annually against current portfolio composition. As your loan mix shifts, the vintage analysis or cohort method that worked two years ago may no longer represent your actual risk profile. Regulators expect dynamic, not static, compliance. Credit unions can also find specific guidance on credit union compliance requirements under NCUA's CECL framework.

Future trends and best practices in loan risk modeling

The modeling landscape is shifting faster than most regulatory guidance can keep pace with. Forward-looking ECL models are now standard practice, but the frontier is moving toward more robust scenario analysis, continuous model monitoring, and the integration of alternative data sources that capture real-time borrower behavior.

Emerging techniques and trends worth tracking:

- Alternative data integration: Rent payment history, utility data, and cash flow analytics from bank account data are expanding the credit-visible population and improving PD accuracy for thin-file borrowers

- Explainable AI (XAI) as standard practice: Regulatory guidance from the OCC, FDIC, and Federal Reserve increasingly expects institutions to document how model decisions can be explained, making XAI a compliance requirement rather than a differentiator

- Continuous model monitoring: Static annual validation cycles are giving way to real-time performance dashboards that flag population shift, feature drift, and discrimination risk as they emerge

- Climate and ESG risk integration: Physical and transition climate risks are beginning to appear in commercial real estate and agricultural loan models, driven by both regulatory expectation and investor pressure

- Scenario analysis sophistication: Institutions are moving from two-scenario stress tests to probabilistic scenario fans that quantify the full distribution of potential loss outcomes

Best practices for maintaining both compliance and modeling flexibility include maintaining a clear separation between model development, validation, and use functions; investing in model documentation that non-technical stakeholders can understand; and building advanced risk mitigation capabilities that connect model outputs to early warning and workout processes.

Pro Tip: As model complexity grows, so does model risk. Assign each model a risk tier based on materiality and complexity, then calibrate your validation frequency and depth accordingly. A high-complexity ML model driving commercial loan decisions warrants quarterly monitoring, not annual review.

A practitioner's take: Why modeling nuance matters more than ever

The institutions that struggle most with loan risk modeling are rarely those that lack data or technology. They are the ones that treat modeling as a compliance exercise rather than a decision-support discipline. Checking the regulatory box produces documentation. It rarely produces better credit outcomes.

The most persistent blind spots we observe are overfitting models to historical data that does not represent future conditions, misunderstanding how procyclicality will amplify losses during the next downturn, and ignoring data drift until model performance has already degraded. Each of these failures is preventable with deliberate model design and governance.

One concrete example: institutions that switched from pure PIT models to hybrid PIT/TTC approaches before the 2020 economic shock found that their ECL estimates were far less volatile and their capital positions more defensible. That modeling nuance translated directly into examiner confidence and avoided reactive reserve builds that strained earnings. The real-world risk mitigation lessons from that period are still underutilized by many community institutions.

Transparent, well-validated models also carry an underappreciated business value: they accelerate loan decisions, reduce override rates, and build underwriter confidence in the tools they use daily. The goal is not a perfect model. It is a model that is honest about its limitations and built to improve.

Taking the next step: Smarter loan risk solutions

Understanding loan risk modeling at this level of depth is the foundation. Applying it consistently across your portfolio, under regulatory scrutiny, with explainable outputs and real-time monitoring, requires the right infrastructure.

RiskInMind's AI-powered risk management platform is built specifically for credit unions, community banks, and lenders navigating exactly these challenges. The loan assessor tool delivers model-driven credit analysis with built-in explainability, while the regulatory risk agent keeps your compliance posture aligned with Basel, CECL, and IFRS 9 requirements in real time. With SOC 2® certification and sub-half-second response times, your team gets the accuracy and speed that modern risk management demands. Explore a demo and see how purpose-built AI changes what's possible.

Frequently asked questions

What is the main purpose of loan risk modeling?

Loan risk modeling quantifies default likelihood and estimates potential financial losses to inform lending decisions and regulatory compliance. It serves underwriters, compliance officers, and portfolio managers across the full loan lifecycle.

How do machine learning models improve credit risk assessment?

ML models boost discriminatory accuracy and can reduce non-performing loans by up to 20%, though they require explainability techniques such as SHAP values to meet regulatory adverse action and model validation requirements.

What are PD, LGD, and EAD in loan risk modeling?

PD is the probability of default, LGD is the loss given default, and EAD is the exposure at default; together, these Basel-accredited parameters form the ECL calculation that drives reserve and capital decisions.

How do regulations like Basel and CECL affect risk modeling?

Basel III/IV and CECL require forward-looking models that estimate expected losses using macroeconomic scenarios and loan staging criteria, directly linking model outputs to capital adequacy and reserve calculations.

Recommended

- CRE Loan Risk Predictor - AI Commercial Real Estate Analysis | RiskInMind

- How Smarter Risk Management Can Help Prevent the Domino Effect of Loan Defaults | RiskInMind

- Emerging Risks In Subprime Unsecured Lending Based On Latest Credit Insights | RiskInMind

- Credit RiskinMind AI Credit Memo Generator | RiskInMind