Manual risk assessment breaks down quietly, until a regulatory examination exposes a gap or a credit loss surfaces that a well-calibrated model would have flagged weeks earlier. Financial institutions today face an accelerating combination of loan volume, regulatory complexity, and data velocity that overwhelms spreadsheet-driven workflows and siloed review processes. Automation and AI are not optional upgrades at this point; they are operational necessities for credit unions, community banks, and lenders that want to remain competitive and compliant. This guide walks through exactly how to build, validate, and sustain an automated risk assessment process, from laying the groundwork to avoiding the pitfalls that derail even well-intentioned programs.

Table of Contents

- Laying the groundwork: What you need before automating risk assessment

- Step-by-step: How to automate your risk assessment process

- Validating and monitoring automated risk assessment

- Common mistakes and advanced tips for long-term value

- A smarter future: Why automation works best with expert judgment

- Take the next step: Leverage AI-powered risk management today

- Frequently asked questions

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

Key Takeaways

| Point | Details |

|---|---|

| Preparation is key | Successful risk automation starts with data quality, process mapping, and stakeholder buy-in. |

| Use the right tools | Select AI platforms tailored to your risk workflow, from RPA and agentic AI to predictive analytics. |

| Continuous oversight | Always monitor automated systems for drift, bias, and compliance to prevent costly mistakes. |

| Human expertise required | Automation delivers best results when it augments rather than replaces skilled risk professionals. |

Laying the groundwork: What you need before automating risk assessment

Before jumping into implementation, it's critical to set the right foundation. Automation cannot paper over broken processes or compensate for fragmented data. If your risk data lives in disconnected core systems, inconsistent spreadsheets, or partially digitized loan files, no AI model will extract reliable signal from that noise. The single most important preparatory step is achieving data quality and accessibility across your key risk domains: credit, operational, market, and compliance.

Stakeholder alignment is equally non-negotiable. Risk automation touches IT, compliance, lending, finance, and senior leadership simultaneously. Without explicit buy-in from each group, implementation stalls at the integration stage. Process mapping and workflow documentation are not administrative overhead; they are the blueprints your automation tools need to function correctly. If a process is not clearly defined on paper, it cannot be reliably replicated by software.

Several roadblocks appear consistently across institutions of all sizes. Incomplete control libraries leave AI models without reference points for gap analysis. Legacy core systems often lack modern APIs, which complicates data ingestion. Compliance teams sometimes face regulatory gaps and transparency concerns that require resolution before agentic AI tools can be deployed. And model drift, bias, data quality issues, and hallucination risks in generative AI tools all require proactive controls before any system goes live.

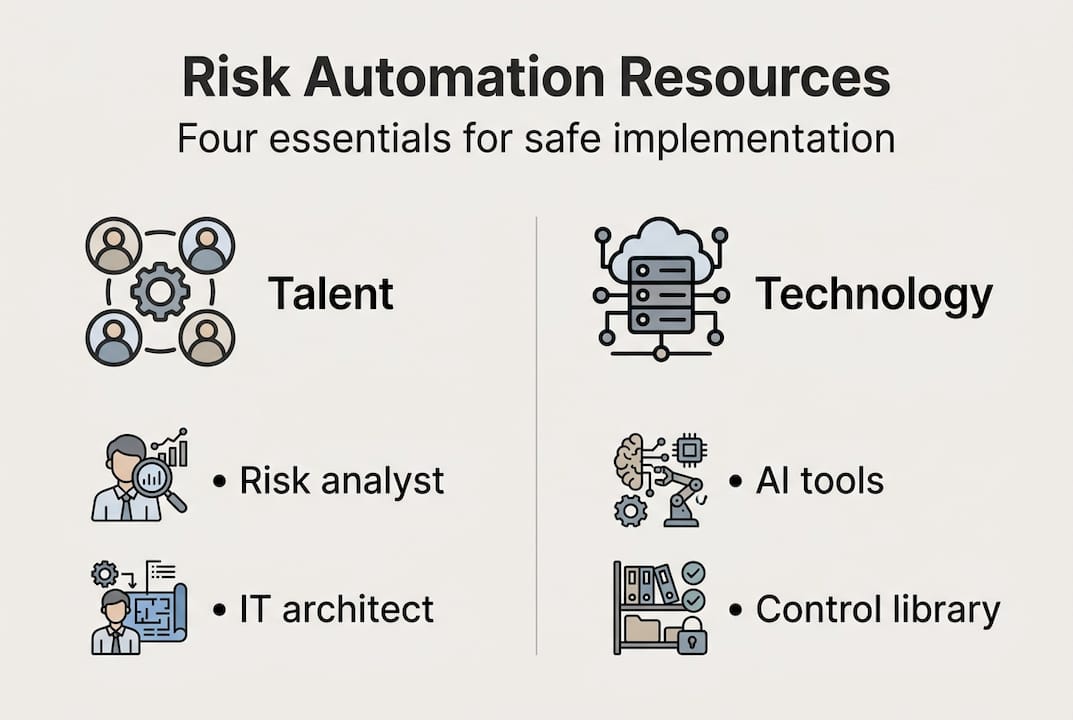

| Resource area | What you need |

|---|---|

| Internal talent | Risk analysts, IT architects, compliance officers |

| AI/integration partners | Vendors with banking-specific implementations |

| Data sources | Core system exports, loan origination data, regulatory filings |

| Governance framework | Model risk policy, data governance charter |

Building your resource foundation across these four areas before selecting any tool reduces implementation risk significantly. Institutions that invest in growth through AI risk intelligence consistently cite pre-implementation data cleanup and stakeholder workshops as the highest-return preparatory activities.

Pro Tip: Designate a cross-functional automation champion who sits at the intersection of risk and technology. This person owns the implementation timeline, resolves integration conflicts, and keeps business units aligned on shared objectives.

Step-by-step: How to automate your risk assessment process

Once everything's in place, follow this sequence to bring automation to life. The shift from manual to intelligent processes is not a single event; it's a structured progression that compounds value at each stage.

- Define objectives and scope. Identify which risk processes generate the most friction or the highest error rates. Quantify the cost of manual effort in those workflows before selecting any tool.

- Audit and prepare your data. Standardize data formats, resolve duplicate records, and establish data pipelines between your core system and risk platform. Automation quality is a direct function of data quality.

- Select the right automation approach. Not all AI is equivalent for risk tasks. Match the tool type to the specific workflow you are automating.

- Run a controlled pilot. Deploy automation on a single high-impact workflow first, validate outputs against manual benchmarks, and measure accuracy, speed, and exception rates before scaling.

- Integrate with existing systems. Connect your automation layer to your loan origination system, core banking platform, and regulatory reporting tools through secure APIs.

- Build a continuous feedback loop. Establish performance metrics, schedule periodic model reviews, and create escalation protocols for flagged exceptions.

| Automation type | Best-fit risk tasks |

|---|---|

| RPA (robotic process automation) | Data entry, reconciliations, standard report generation |

| Generative AI | RCSA narratives, control gap analysis, regulatory document drafting |

| Agentic AI | End-to-end credit reviews, KYC/AML workflows, transaction monitoring |

| Predictive ML models | Dynamic risk scoring, delinquency prediction, anomaly detection |

Key methodologies for automating risk assessment include RCSA automation, agentic AI workflows, RPA, and predictive ML for dynamic risk scoring and anomaly detection, each suited to different layers of the risk function. Tools like AI-powered credit memo automation and predictive analytics for loan risk illustrate how these approaches translate directly into measurable workflow improvements. For compliance-specific workflows, agentic AI for compliance automation can handle end-to-end regulatory tasks that previously required days of analyst time.

Reviewing AI risk management lessons from recent institutional failures makes clear that sequencing and piloting are not optional steps; they are what separates successful programs from costly rollbacks.

Pro Tip: Start with one high-volume, rule-based workflow such as loan application data extraction before moving to judgment-intensive processes like credit risk scoring. Early wins build organizational confidence and expose integration issues at manageable scale.

Validating and monitoring automated risk assessment

Automation's value is only as strong as ongoing validation, and here's how to get it right. A model that performed well at launch can degrade silently as market conditions shift, data distributions change, or regulatory expectations evolve. This is the core challenge of model drift, and it requires a structured monitoring program rather than periodic manual spot checks.

Effective validation programs for automated risk assessment typically include:

- Continuous performance tracking against baseline accuracy metrics established during piloting

- SHAP and LIME testing to explain individual model decisions and detect algorithmic bias in credit or compliance outputs

- Circuit breakers that automatically escalate decisions to human reviewers when model confidence falls below defined thresholds

- Audit trail maintenance that documents every automated decision, input data point, and override for regulatory examination readiness

- Regular backtesting of predictive models against realized outcomes to confirm ongoing calibration

Model drift, bias, and overreliance on automation without human oversight represent the most frequently cited AI-specific risks in banking, and each requires a distinct control response rather than a one-size-fits-all monitoring policy. Traditional model risk management frameworks were not designed for the complexity of large language models or agentic AI, and extending them requires explicit policy updates and dedicated validation resources.

"Traditional MRM frameworks are insufficient for complex AI systems and require extension. Institutions using ad-hoc validation approaches show materially higher breach rates than those with integrated, continuous monitoring programs."

The practical impact of monitoring is most visible in early warning scenarios where automated systems flag portfolio deterioration weeks before it appears in standard reporting. Regulatory transparency is a parallel requirement: examiners at the OCC, FDIC, and NCUA increasingly expect institutions to demonstrate not just that a model produces accurate outputs, but that they can explain why it produced them. Financial AI validation capabilities that include explainability reporting are no longer optional features; they are baseline expectations.

Common mistakes and advanced tips for long-term value

Beyond monitoring, it's crucial to sidestep pitfalls and drive lasting improvement. The most consequential mistakes in risk automation programs share a common theme: treating deployment as an endpoint rather than the beginning of an ongoing operational discipline.

The mistakes most likely to undermine long-term value include:

- Neglecting human oversight checkpoints by assuming automation handles edge cases that require contextual judgment

- Poor data governance that allows training data to drift from current business conditions without formal review triggers

- Failing to update control libraries as new products, markets, or regulatory requirements emerge, leaving AI models referencing outdated benchmarks

- Deploying automation without explainability tools on major credit or compliance decisions, creating regulatory defense vulnerabilities

- Ad-hoc rather than integrated automation which research consistently links to higher breach rates and weaker risk outcomes

AI augments but does not replace human judgment in areas like RCSA interviews, regulatory examination responses, and complex credit decisions where qualitative context determines the outcome. Automation reduces false positives in transaction monitoring and speeds up document review, but it simultaneously introduces new risks around bias, explainability, and model dependency that require active management.

Institutions that have scaled successfully share one consistent practice: moving from ad-hoc automation of individual workflows to a fully integrated automation architecture. This approach, described in detail for AI risk management at scale, connects risk identification, control evaluation, monitoring, and regulatory reporting into a single coherent system with shared data standards and consistent governance.

Pro Tip: Schedule formal human review checkpoints at 30, 90, and 180 days post-deployment for every automated workflow. Use explainability tools like SHAP on all major decisions during these reviews, and document findings to support future regulatory examinations.

A smarter future: Why automation works best with expert judgment

With the practical how-to covered, here's a frank perspective every risk leader should consider. The most persistent misconception in risk automation is that sufficiently advanced AI will eventually make risk professionals redundant. This view misunderstands both what AI does well and where it reliably fails.

AI excels at pattern recognition across large datasets, consistency in applying defined rules, and speed in processing structured information. It struggles with novel scenarios that fall outside its training distribution, regulatory nuance that requires interpretive judgment, and the credibility that human expertise lends to examiner or board-level conversations. High-profile model failures and regulatory pushback in recent years have reinforced this point, not undermined it.

The institutions generating the clearest value from automation are not those that have replaced risk analysts but those that have freed them from repetitive data processing so they can focus on interpretation, strategy, and stakeholder communication. AI risk intelligence case studies from community institutions consistently show this pattern. Automation elevates experts. It does not erase them, and any implementation strategy built on the assumption that it will is likely to produce both operational and regulatory problems.

Take the next step: Leverage AI-powered risk management today

RiskInMind is built specifically for financial institutions that are ready to move from manual, fragmented risk processes to a connected, AI-powered risk management program. From AI-powered loan application automation that reduces processing time and manual data entry, to compliance automation with Erina that handles regulatory reporting and control gap analysis, the platform is designed to reduce manual workload while improving auditability at every step.

If your institution is evaluating automation options or looking to accelerate an existing program, explore all AI risk solutions to see how RiskInMind's suite of specialized AI agents, guided by Ava, can support your risk function from loan underwriting through portfolio monitoring. Schedule a demo and see real response times under half a second with SOC 2 certified, bank-grade security.

Frequently asked questions

What are the first steps to automate risk assessment at a bank?

Begin with data preparation, stakeholder alignment, and selecting a single workflow for pilot automation. Stakeholder alignment and process mapping are prerequisites that determine whether the broader rollout succeeds or stalls.

How does AI improve accuracy in risk assessment?

AI automates data analysis, reduces human error, and applies predictive models for real-time anomaly and risk detection. Predictive ML for dynamic scoring and anomaly detection consistently outperforms manual threshold-based approaches across large loan portfolios.

What are the biggest risks with automated risk assessment?

Key risks include model drift, algorithmic bias, data quality degradation, and overreliance on automation without human review checkpoints. Model drift, bias, and data quality issues require distinct, documented control responses rather than general monitoring policies.

Does automation replace the need for risk experts?

No. Automation enhances expert efficiency but human interpretation, decision-making, and regulatory engagement remain essential to effective risk management. AI augments, not replaces, the judgment that risk professionals bring to complex credit and compliance scenarios.

Recommended

- Transforming Credit Union Growth with AI-Powered Risk Intelligence | RiskInMind

- RiskInMind - AI-Powered Risk Management Solutions

- Streamline your risk analysis process for better compliance | RiskInMind

- Security Policy - RiskInMind

- Master Risk Management In Automated Trading MT4 MT5

- Risk Analyst Staffing — Quantitative & Operational Risk | Careerscape